Sell off coinciding with the news that the Bank of Japan is going to discuss changes to its yield curve control policy at its policy meeting on Friday

GLOBAL CAPITAL MARKETS OVERVIEW, ANALYSIS & FORECASTS:

Author: Dr. Alexander APOSTOLOV (researcher at Economic Research Institute at BAS)

European stocks continued to rise on Thursday afternoon, with Frankfurt's DAX 40 up about 1.2 percent to a near six-week high of 16,320, as investors digested the latest policy decisions from the European Central Bank and Federal Reserve, as well as a slew of earnings reports. The European Central Bank raised interest rates for the ninth time in a row and opened the door to further tightening, while investors believe the tightening cycle in the United States is over. On the enterprise front, several companies made notable announcements. Nestlé improved its full-year organic sales outlook, Renault posted its biggest-ever operating margin, and Airbus posted a better-than-expected underlying operating profit and reiterated its financial targets for the year. Elsewhere, Shell reported a 56% drop in profit from the previous year to $5 billion, while Barclays' first-half profit was in line with expectations.

The CAC 40 rose more than 1% to 7,410 on Thursday as investors focused on corporate earnings. Shares of Saint-Gobain were the best performers, rising more than 5% after the company reported strong results for the first half of the year. BNP Paribas rose nearly 4 percent after second-quarter net income topped estimates, while Safran rose 2.4 percent after it raised its profit and cash flow forecasts. Conversely, the biggest laggard was call center operator Teleperformance, which fell nearly 10% after it lowered its full-year revenue growth target. Airbus shares fell 1.8% after it scrapped an interim industrial target for record jet output, while Renault shares fell 1.1% despite its record high operating margin for the first half of 2023. Traders also priced in a widely expected quarter-point hike from the Federal Reserve yesterday and braced for a rate hike from the European Central Bank later in the day.

The ruble-based MOEX Russia index rose on Thursday, trading at its highest level since February 2022. Oil and gas stocks rose 0.5 percent as oil prices rose. RussNeft NK, in particular, gained 4.4 percent. Elsewhere, financials rose more than 1%, pushing their year-to-date gains to 50%. VTB, Russia's second-largest bank, is on track to post record profits this year, Chief Financial Officer Dmitry Pyanov said. He expressed confidence in the bank's future performance, expecting further loan growth and improving his forecast for a return on equity of more than 20% in 2023. On the other hand, tech giant Yandex reported a 27% drop in second-quarter net profit compared to the previous year as the company tightened spending following Russia's invasion of Ukraine due to higher costs.

The FTSE 100 was higher on Thursday as traders continued to digest quarterly company results and interest rate decisions. Informa rose nearly 4% as it remained on track to meet its full-year forecast thanks to strong bookings and a recovery in China. Elsewhere, Centrica jumped 4% after announcing a big dividend increase and posting a first-half profit. Conversely, Shell fell around 2% after reporting a 56% drop in second-quarter profit, Barclays fell more than 5% on a 56% drop in second-quarter profit, while Barclays fell 5.5% on a warning of stress in its UK business. % and its investment banking unit missed expectations. On the monetary policy front, the Federal Reserve raised interest rates by 25 basis points on Wednesday, and the European Central Bank and Bank of England are also expected to raise rates soon.

U.S. stocks were higher on Thursday, with the Dow up about 80 points and on track for a 14th straight session of gains, while the S&P 500 rose 0.8% and the Nasdaq rose 1.5% as investors reacted to fresh data and corporate earnings results feel happy. The U.S. economy grew by 2.4% in the second quarter, beating market expectations of 1.8%, suggesting the U.S. economy remains resilient despite high interest rates. Meanwhile, shares of Meta Platforms rose about 8% after the company reported strong earnings and profits and gave a better-than-expected forecast for the period. Comcast rose more than 6.5 percent after earnings and revenue topped estimates, while McDonald's rose about 1.4 percent after sales topped expectations. Mastercard is also in the green (0.2%) after posting strong revenue and earnings growth. Today, after the market closes, Intel, Ford, and T-Mobile are all set to report.

On Thursday, the Shanghai Composite fell 0.2 percent to close at 3,217 points and the Shenzhen Composite fell 0.41 percent to close at 10,924 points, reversing gains made earlier in the session as investors digested a 16.8 percent drop in Chinese industrial profits in the first half. % figures, supporting the need for further stimulus from Beijing. Earlier this week, China's Politburo pledged to step up policy measures to boost growth as China's post-epidemic recovery showed signs of slowing. Technology stocks fell the most, Donghui Information (-1.2%), China Machine Innovation (-0.9%), Foxconn Industry (-2.5%), HKUST Xunfei (-0.6%) and Luxun Precision (-2.2%) fell significantly.

Hongkong Hang Seng Index soared 273.97 points, or 1.41%, to close at 19639.11 points, turning from a weak session the previous day to its highest level in five weeks, helped by the outcome of a meeting of China's Politburo, which had a more expansive tone, as Promote household consumption, cut taxes and fees, and provide further assistance to the real estate market. The government also plans to ease local government debt by limiting local government bond issuance. Traders were also optimistic, with U.S. futures notably higher after the Federal Reserve said it would decide whether to pause or raise rates based on the data. All major sectors contributed to the upturn, with technology and real estate each up nearly 3%. Shares of XPeng soared 33.9 percent after Volkswagen AG said it planned to invest $700 million in the Chinese electric car maker. KE Holdings (10.3%), Geely Automobile (8.6%), Xiaomi Corporation (5.6%) and Li Ning (5.3%) also claimed victory for Sharp.

New Zealand shares closed almost flat on Thursday at 11,954.11, after dipping slightly in early trade, with gains in communications, consumer non-durables and health care offsetting losses in retail trade, financial and industrial services. Investors continued to study the Federal Open Market Committee's decision to raise its key interest rate by 25 basis points on Wednesday, amid signs that Fed Chairman Jerome Powell was no more hawkish than before, as any further tightening would depend on data. Meanwhile, traders were carefully monitoring the European Central Bank meeting later in the day, which is expected to raise the benchmark by another 0.25 percentage point. Domestically, signs of easing inflation have grown in New Zealand with the Reserve Bank of New Zealand raising interest rates by a total of 525 basis points since the end of 2021, but the board recently warned that further rate hikes may be needed to bring inflation back to 1% to 3% %The goal. In China, the Politburo has vowed to implement countercyclical policies to support the economy.

Tokyo's Nikkei 225 rose 252 points, or 0.77%, on Thursday. The top gainers were Tokuyama (3.80%), Bandai Namco Holdings (3.52%) and Tokyo Electric Power (3.1%). The biggest decliners were CyberAgent (-11.24%), Nitto Denko (-4.27%) and Nissan (-2.98%).

India BSE Sensex extended early losses to close 440 points lower at 66,267 on Thursday, pressured by financial firms and automakers as the market continued to assess key corporate earnings and price in a widely expected rate hike from the Federal Reserve. Political clashes also weighed on sentiment after India's parliament authorized a vote of no confidence in Prime Minister Modi over violence in northern Manipur state, although Modi's majority in parliament would prevent any instability. On the corporate front, Mahindra fell 6.2 percent after it announced plans to buy a stake in private lender RBL. Elsewhere, Tech Mahindra fell 3.6% after reporting a drop in quarterly profit, citing weak consumer spending.

REVIEWING THE LAST ECONOMIC DATA:

Reviewing the latest economic news, the most critical data is:

- US: According to a survey by the National Association of Realtors, in June 2023, contracts to buy second-hand homes in the United States rose by 0.3% month-on-month, exceeding market expectations for a 0.5% decline. The increase came after three straight periods of decline, suggesting the housing market is trying to recover from lows caused by the Federal Reserve's unprecedented rate hikes. Looking at regional trends, contract signings increased in the Northeast and Midwest, but declined in the South and West. Pending deals fell 15.6% compared to the same period last year. The 30-year fixed mortgage rate will drop to 6.4% this year and further down to 6.0% in 2024. NAR chief economist Lawrence Yun (Lawrence Yun) also mentioned, "the existence of multiple quotations means that due to insufficient supply, housing demand is not being met. Home builders are increasing production and hiring workers."

- US: Preliminary estimates show that in June 2023, U.S. wholesale inventories fell by 0.3% month-on-month, unchanged from the previous month. Durable goods inventories fell (-0.1% from 0.4% in May) and non-durable goods inventories fell (-0.7% from -1.4%). Wholesale inventories rose 1.7% in June from a year earlier.

- US: The U.S. goods trade deficit narrowed to $87.8 billion in June 2023 from a revised $91.9 billion last month, according to advance estimates. Exports edged up 0.2% to $162.5 billion, with growth in sales of capital goods (1.6%), food, feed and beverages (0.1%), and other goods (9.5%) outpaced by gains in industrial goods (-1.2%), consumer goods (- 1.2%) and automobiles (-0.4%) were partly offset by declines in exports. Imports, meanwhile, fell 1.4% to $250.3 billion, driven largely by declines in purchases of industrial supplies (-4.4%), capital goods (-3.3%) and other goods (-4.2%).

- US: The U.S. goods trade deficit narrowed to $87.8 billion in June 2023 from a revised $91.9 billion last month, according to advance estimates. Exports edged up 0.2% to $162.5 billion, with growth in sales of capital goods (1.6%), food, feed and beverages (0.1%), and other goods (9.5%) outpaced by gains in industrial goods (-1.2%), consumer goods (- 1.2%) and automobiles (-0.4%) were partly offset by declines in exports. Imports, meanwhile, fell 1.4% to $250.3 billion, driven largely by declines in purchases of industrial supplies (-4.4%), capital goods (-3.3%) and other goods (-4.2%).

- US: New orders for US-made durable goods rose 4.7% month-on-month in June 2023, the highest since July 2020, after a 2% increase in May and easily beating market expectations of 1%. It was the fourth straight month of growth in durable goods orders. Transportation equipment surged 12.1 percent, boosted by nondefense aircraft and parts (69.4 percent) and motor vehicles (0.3 percent). Excluding transportation, new orders rose 0.6%. Demand also increased for capital goods (11.2%), namely non-defense goods (16.9%), machinery (0.1%), computers and electronics (1.5%), electrical equipment (1.5%) and primary metals (0.9%). Excluding defense, new orders rose 6.2%. Orders for nondefense capital goods excluding aircraft, a closely watched indicator of business spending plans, rose 0.2 percent after falling 0.5 percent in May.

- US: Forecasts show that in the second quarter of 2023, the U.S. economy will grow by an annualized quarter-on-quarter of 2.4%, higher than the 2% in the previous period, and much higher than the market's expected 1.8%. Nonresidential fixed investment accelerated sharply (7.7% vs. 0.6%), led by a rebound in equipment (10.8% vs. -8.9%) and intellectual property products (3.9% vs. 3.1%). Also, private inventories added 0.14 percentage points to growth (-2.14 in Q1). On the other hand, consumer spending slowed sharply (1.6% vs. 4.2%), but remained above market expectations as inflation eased, but the labor market remained tight. While consumption of goods slowed sharply (0.7% vs. 6%), spending on services remained strong (2.1% vs. 3.2%). In addition, public spending grew at a much slower rate (2.6% vs. 5%), and the impact of net trade on growth was reduced by 0.12 percentage points, with exports falling by 10.8% and imports by 7.8%. Residential investment continued to decline (-4.2% vs. -4%).

- US: The U.S. economy could grow at an annualized rate of 1.8% in the second quarter of 2023, which would be the slowest growth in a year after a 2% expansion in the first quarter. Consumer spending is expected to remain strong, though likely at a slower pace, while business investment is likely to pick up, driven by equipment such as airplanes and cars. Government spending is also seen as a contribution to global growth, while net trade is expected to be a drag and residential investment could fall again. Investors are increasingly confident the U.S. economy can avoid a recession this year thanks to a strong labor market, rising wages and savings. At the FOMC news conference in July, Chairman Jerome Powell said that while central bank staff no longer forecast a U.S. recession, economic growth was expected to be below trend and labor market conditions would soften. In June, the Fed forecast that the U.S. economy would grow by 1% this year.

- CA: Average weekly earnings for Canadian non-farm payrolls rose 3.6% year-over-year to $1,201 in May 2023 after rising 2.9% the previous month. It was the biggest gain in earnings since November, with 19 of 20 industries reporting profits. The biggest gains were in forestry and logging (up 10 percent to $1,404), utilities (up 6.7 percent to $2,155) and other services, excluding public administration (up 6.5 percent to $1,025). Among Canadian provinces, revenues were in Nunavut (up 7.4 per cent to $1,658), Nova Scotia (up 5.5 per cent to $1,065) and Manitoba (up 4.7 per cent to $1,094) largest increase.

- CA: Average weekly earnings for Canadian non-farm payrolls rose 3.6% year-over-year to $1,201 in May 2023 after rising 2.9% the previous month. It was the biggest gain in earnings since November, with 19 of 20 industries reporting profits. The biggest gains were in forestry and logging (up 10 percent to $1,404), utilities (up 6.7 percent to $2,155) and other services, excluding public administration (up 6.5 percent to $1,025). Among Canadian provinces, revenues were in Nunavut (up 7.4 per cent to $1,658), Nova Scotia (up 5.5 per cent to $1,065) and Manitoba (up 4.7 per cent to $1,094) largest increase.

- CA: Canada's CFIB Business Barometer Long-Term Optimism Index edged up 0.2 points from the previous month to 54.2 points in July 2023, indicating that small businesses remain relatively optimistic about conditions in the coming year. Optimism in financial services and insurance companies (+3 to 59.1), information and entertainment companies (+1.5 to 70), and hospitality (+1.8 to 62.7) improved significantly, while pessimism in retail (+4.5 to 47.2) alleviated. On the other hand, pessimism increased in agriculture (-6.3 to 39.1) and optimism in manufacturing (-1.1 to 55.1) declined.

- UK: The Confederation of British Industry's Distributive Trade Survey showed that the UK retail sales balance fell to -25 in July 2023 from -9 in the previous month, indicating that retail sales fell at the fastest rate since April 2022. Also, expectations for the month ahead fell from zero to -32, the lowest reading since March 2021. Orders with suppliers fell to the lowest level since January 2021, when the UK re-entered a COVID-19 lockdown, the survey showed. Commenting on the situation, Martin Sartorius, an economist at the Confederation of British Industry (CBI), said: "Businesses are cutting orders and bracing for another sales contraction in the year to August. As we prepare, we remain cautious about the near-term outlook for the retail industry," he said, adding that due to cost pressures, a tight labor market, rising interest rates, and uncertain demand conditions.

- UK: UK car production rose 16.2% year-on-year to 84,767 in June 2023, the fifth consecutive month of growth, as manufacturers are increasingly able to cope with global supply chain challenges, notably semiconductor shortages that have limited production since the pandemic. In the first half of this year, UK car production rose 11.7 percent to 450,168 vehicles, exports rose 11.6 percent and domestic sales rose 4.5 percent. The EU remains the largest global market, accounting for 59.5% of UK car shipments so far this year, followed by the US, China, Japan and Australia. Production of hybrid, plug-in hybrid and battery electric vehicles rose 71.6% so far this year and accounted for 37.8% of all vehicles produced so far this year. Mike Hawes, chief executive of SMMT, said: “UK car manufacturing is growing again, with output – especially electric models – rising and major investment announcements dominating the headlines.”

- IT: In July 2023, Italian consumer confidence fell to 106.7 from 108.6 in the previous month, below market expectations of 107. The economic environment dropped from 127.6 to 123.4, the future environment deteriorated from 118.4 to 115.0, the personal environment dropped from 102.2 to 101.1, and finally, the current environment dropped from 102.0 to 101.0.

- GE: Entering August 2023, Germany's GfK consumer climate indicator rose to -24.4 from 25.2 revised down last month, higher than the market forecast of -24.7. Income expectations are at their highest level since February 2022, inflation is expected to be lower (-5.1 to -10.6 in July), while propensity to buy is up slightly (-14.3 to -14.6). Meanwhile, economic sentiment was unchanged at 3.7 after easing in the previous two months. "The main reason for the weakening of pessimism is the hope that inflation will fall," said GfK consumer expert Rolf Bürkl. "This means that the likelihood of a recovery in the consumer environment has increased. However, this level will remain low in the coming months, so that private consumption will not be able to make any positive contribution to overall economic development."

- AU: Australia's import prices fell 0.8% quarter-on-quarter in the three months to June 2023, after falling 4.2% in the three weeks to March. It was the second straight month of declines in import prices, as demand weakened due to high inflation and a slowdown in commodity prices. The main decliners were: petroleum, petroleum products and related materials (-7.0%), as demand for oil shrank on fears of a global recession; fertilizers (-16.4%), dragged down by lower natural gas and ammonia prices; and chemical materials and Products (-8.2%) due to lower global prices for insecticides and herbicides. Offsetting this decline, specialist machinery rose 5.6%, supported by a weaker Australian dollar, while non-monetary gold rose 7.2%, driven by stronger demand for safe-haven assets. Import prices fell 0.3 percent through the second quarter, reversed from a 4.7 percent increase in the first quarter.

- AU: In the three months to June 2023, Australian export prices fell by 8.5% quarter-on-quarter, reversed from a 1.6% increase in March to March. It was the biggest drop in export prices since the third quarter of 2009, when demand weakened and commodity prices slowed. The decrease was mainly due to: coal, coke and briquettes (-20.6%), dragged down by lower heating and metallurgical gas demand; natural and manufacturing (-20.9%), driven by lower oil-related contract prices and high European inventories , spot prices faced further downward pressure; metal-bearing ore and metal scrap (-6.2%), whose manufacturing and construction growth slowed due to lower demand for iron ore in China; and coarse manure and minerals (-5.8%). The decline was partly offset by non-monetary gold (+6.4%); sugar and honey (+119.1%); and meat and meat products (+3.8%). Export prices plunged 11.1 percent through the second quarter after rising 6.9 percent in the first quarter.

LOOKING AHEAD:

Today, investors should watch out for the following important data:

- EUR: French Consumer Spending m/m, French Flash GDP q/q, German Prelim CPI m/m, French Prelim CPI m/m, Spanish Flash CPI y/y, Spanish Flash GDP q/q, and EU Economic Forecasts.

- JPY: Tokyo Core CPI y/y, BOJ Outlook Report, Monetary Policy Statement, BOJ Policy Rate, and BOJ Press Conference.

- USD: Core PCE Price Index m/m, Employment Cost Index q/q, Personal Income m/m, Personal Spending m/m, Revised UoM Consumer Sentiment, and Revised UoM Inflation Expectations.

- AUD: PPI q/q, and Retail Sales m/m.

- CHF: KOF Economic Barometer.

- CAD: GDP m/m.

KEY EQUITY & BOND MARKET DRIVERS:

Кey factors in the stock and bond market are currently:

- EU: French 10-year OAT yields extended losses, falling below the 3% threshold and approaching a three-week low of 2.834% hit on July 19. Earlier, the European Central Bank raised interest rates to a new multi-year high and left the door open for further rate hikes. Notably, this marked the ninth consecutive rate hike by ECB officials, who expressed concern about the near-term outlook. The Fed made a similar move on Wednesday, but a dovish Powell convinced investors that the rate hike in July was the last in this tightening cycle.

- IT: Italy's 10-year BTP yield edged down to 4%, close to a three-week low of 3.94% hit on July 19. Earlier, the European Central Bank raised interest rates for the ninth time in a row and kept the possibility of further rate hikes on the back of easing inflation pressures and signs of weak economic growth. The Federal Reserve made a similar move on Wednesday. Traders see the ECB's rate peaking at around 3.92 percent in December this year, little changed from before the decision, while they believe the Fed's tightening policy is over.

- US: U.S. 10-year Treasury yields rose to 3.9% on Thursday, as strong U.S. data reinforced the view that the Federal Reserve may be forced to continue tightening policy. The U.S. economy grew at a 2.4% pace in the second quarter, well above market expectations of 1.8%, underscoring the economy's resilience to higher interest rates. In addition, initial jobless claims unexpectedly fell to the lowest level in five months, suggesting that the labor market remains tight.

- US: U.S. stock futures continued to rise on Thursday, with the Dow Jones contract up about 170 points, the S&P 500 up 0.9% and the Nasdaq 100 up 1.6% as investors welcomed the new data and corporate earnings results. The U.S. economy grew by 2.4% in the second quarter, beating market expectations of 1.8%, suggesting the U.S. economy remains resilient despite high interest rates. Meanwhile, Meta Platforms surged about 10% in premarket trading after reporting strong earnings and profits and a better-than-expected current forecast. Comcast rose more than 2.5 percent after earnings and revenue topped estimates, while McDonald's rose about 1.1 percent after sales topped expectations. Mastercard is also in the green (0.6%) after posting strong revenue and earnings growth. Intel, Ford and T-Mobile are scheduled to report after the close today.

- GE: German 10-year government bond yields continued to fall to 2.4%, closing at a three-week low of 2.285% touched on July 19, after the ECB raised interest rates by 25 basis points for the ninth time as expected. The central bank reiterated that interest rate decisions will continue to be based on its assessment of the outlook for inflation, adding that inflation continues to decline but is expected to remain too high for too long.

- UK: The 10-year gilt yield was steady at around 4.3%, down from a near 15-year high of 4.717% hit earlier this month, as traders believed the Fed had delivered what some had expected to be the last rate hike of the year. Meanwhile, weaker-than-expected U.K. economic data and signs of easing inflationary pressures have dampened expectations that Bank of England interest rates will peak. The latest PMI survey showed UK business activity growth slowed sharply in July to its lowest level in six months, while CPI data showed UK annual inflation fell to 7.9% in June, the lowest level since March 2022. minimum level. Financial markets are currently pricing in the Bank of England rate peaking at 5.75% in November. That's in stark contrast to last week's pricing, which suggested a slightly more than 50% chance of rates hitting 6% in early 2024.

- EU: The ECB is likely to hike rates by another 25 basis points on Thursday, taking the rate on its main refinancing business to 4.25%, the highest since October 2008, and the deposit rate to 3.75%, a 22-year high. That would mark the ninth straight rate hike since the ECB's tightening cycle begins in July 2022, as policymakers weigh signs of cooling inflationary pressures against the risk of a recession in the euro area, with persistently high core inflation continued challenges, especially the soaring price of services. Investors will be closely watching the upcoming policy statement and President Lagarde's press conference for further insight into the ECB's future trajectory, as several ECB members cast doubt on the need for a rate hike in September.

LEADING MARKET SECTORS:

- Strong sectors: Communication Services.

- Weak sectors: Utilities, Real Estate, Financials, Industrials, Consumer Discretionary.

TOP CURRENCY & COMMODITIES MARKET DRIVERS:

Кey factors in the currency and commodities market are currently:

- EUR: The euro fell to around $1.1 in early trade after upbeat U.S. GDP growth data pushed the greenback higher. Meanwhile, the ECB's borrowing costs rose by another 25 basis points, as expected, and said further decisions would continue to follow a data-dependent approach. At a regular press conference, President Lagarde said a pause or hike is expected, but no cut at the next meeting, and the data will tell us how much, if any, the central bank will have to cover. The euro zone economy has been showing signs of weakness, while inflation remains almost three times above target. Policymakers noted that inflation continued to decline but was expected to remain too high for too long. Meanwhile, a flash PMI survey for July showed the most significant contraction since November, driven largely by a sharp decline in manufacturing not seen in more than three years.

- USA: The U.S. dollar index jumped above 101 on Thursday, erasing early losses after key data backed the Federal Reserve extending tightening at its upcoming September meeting. Underscoring the economy's resilience to higher interest rates, the latest data showed that U.S. gross domestic product rose 2.4% in the second quarter, well above market expectations of 1.8%. Initial jobless claims unexpectedly fell to their lowest level in five months, while continuing claims fell to their lowest level in six months, also reinforcing the hawks' argument that the labor market remains tight. Yesterday, the Fed implemented a widely expected 25 basis point rate hike. Federal Reserve Chairman Jerome Powell insisted the central bank will take a "data-dependent" approach in deciding to raise interest rates further, clarifying that no decision has been made to raise borrowing costs further.

- EUR: The euro gave up some of its early gains but remained above $1.10 on Thursday after the European Central Bank announced an expected increase in borrowing costs by another 25 basis points and said further decisions would continue to follow a data-dependent approach. Traders will now be closely watching President Lagarde's press conference for further insight into the central bank's plans for the rest of the year. The euro zone economy has been showing signs of weakness, while inflation remains almost three times above target. Policymakers noted that inflation continued to decline but was expected to remain too high for too long. Meanwhile, a flash PMI survey for July showed the most significant contraction since November, driven largely by a sharp decline in manufacturing not seen in more than three years.

- NZD: New Zealand's 10-year government bond yield was at 4.6683% on Thursday, little changed from the previous session, as traders digested comments from Federal Reserve Chairman Jerome Powell following Wednesday's 25 basis point rate hike, while reiterating its next steps Decisions will depend on economic data. Meanwhile, the Reserve Bank of New Zealand said in the minutes of its July meeting that inflationary pressures in the country have risen by a cumulative 525 basis points since the end of 2021 and are now easing. However, the central bank mentioned that interest rates will remain at restrictive levels for some time to bring inflation down to the target range of 1% to 3%. New Zealand's headline inflation slowed for the second consecutive quarter to 6% in the second quarter of 2023, the lowest level since the fourth quarter of 2021, from 6.7% in the first quarter of 2022 and 7.4% in the fourth quarter of 2022 .

CHART OF THE DAY:

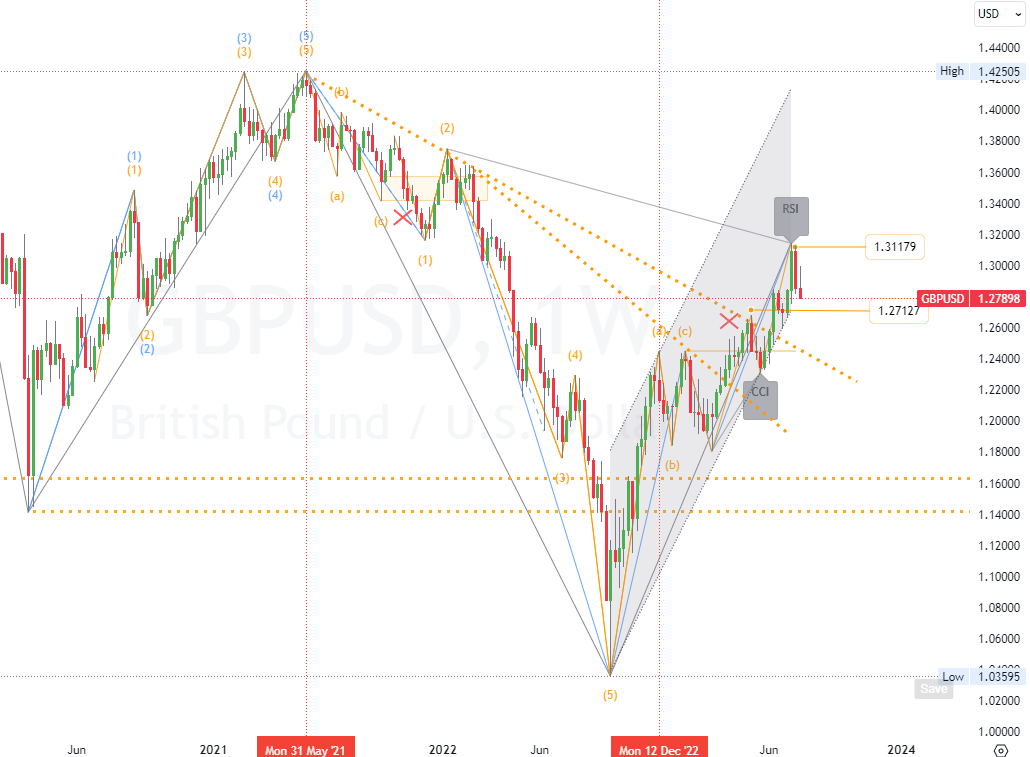

Sterling rose above $1.29, nearing a 15-month high of $1.317 reached on July 14, after the Federal Reserve raised interest rates by 25 basis points as expected, but Fed Chairman Powel sounded dovish in a news conference, and the future direction is uncertain. Certainty remains. Meanwhile, the Bank of England is also expected to raise interest rates by 25 basis points next week. Still, weaker-than-expected PMI data and lower UK inflationary pressures suggest the Bank of England may not have to raise rates as initiallLong-term

rading strategy based on channels for: (GBPUSD). : (GBPUSD).Time frame (D1). The primary resistance is around (1.31179). The primary support is around (1.27127). Therefore, the next most probable price movement is a (down) trend. (*see all other details on the chart).

Start trading in four simple steps

1. Register

Open your live trading account

2. Verify

Upload your documents to verify your account

3. Fund

Deposit funds directly into your account

4. Trade

Start trading and choose from 130+ instruments

Demo account

The Blue Suisse Trading Account with virtual funds in a risk-free environment

Demo accountLive account

The Blue Suisse Trading Account in our transparent live model environment

Open an Account- Trading Account types Trading conditions Trading hours Transparency Market Information

- Products Currencies Commodities Indices Stocks

- Tools MetaTrader 4 / 5 Mobile CRM, MAM and DSP

- Education Currency Trading for Beginners How to improve your trading CFD Trading

- Partnerships Asset- and Moneymanager Tied agent White labels FIX API

- Company About us Regulatory Our philosophy Careers FAQs Contact us