Falling market rates acting as added support for mega caps and growth stocks; US Treasury Yields Retreat after Claims Report; The Eurozone economy is entering recession

GLOBAL CAPITAL MARKETS OVERVIEW, ANALYSIS & FORECASTS:

Author: Dr. Alexander APOSTOLOV (researcher at Economic Research Institute at BAS)

On Thursday, all three main U.S. stock indexes closed in the green, with the Dow Jones gaining more than 160 points and the S&P 500 gaining 0.6%, establishing a new annual closing high. The Nasdaq climbed 1%, leading Wall Street's gains, as a decline in U.S. Treasury yields boosted the overall market. While awaiting inflation data and the Federal Open Market Committee meeting next week, investors digested jobless claims data that exceeded expectations. The number of Americans filing for unemployment benefits increased substantially more than anticipated last week, reaching its greatest level since 2021, indicating that the U.S. labor market may be cooling. As a consequence, the likelihood of a 25 basis point increase in the Fed funds rate this month decreased from 32% to 28%. Amazon shares increased by 2.5%, while Tesla shares increased by 4.6%. Carvana's stock price increased 56% after the company reported a positive outlook for the second quarter. GameStop's stock fell 17.9% following disappointing sales and a poor performance by its fifth CEO in five years.

As a result of the Bank of Canada's unanticipated interest rate increase, the Canada S&P/TSX Composite declined 0.2% to close at 19,940 on Thursday, extending a 0.4% loss from the previous session. On Wednesday, the central bank raised its key overnight benchmark interest rate to a 22-year high of 4.75 percent, leaving open the possibility of further increases in borrowing costs in the face of mounting concerns that inflation could exceed the central bank's target of 2 percent. Oil producers and technology equities led the decline with respective losses of 0.7%. Additionally, industrial equities were under pressure. In contrast, mining companies increased as gold prices increased.

The European stock market ended Thursday unchanged, as gains in auto stocks were countered by losses in telecom companies. Ahead of next week's crucial monetary policy decisions by the Federal Reserve and European Central Bank, investor sentiment remains cautious. Due to the impact of rising prices on consumer expenditure, the euro zone economy entered recession during the winter, according to recent economic data. Due to a more than 8% increase in the value of German biotech company Evotec after Citigroup upgraded its rating from "neutral" to "buy" based on the company's optimistic outlook, the DAX in Germany rose by 0.2%. Thursday's closing price for the CAC 40 index was 7,220, a 0.3% increase from Wednesday's close. However, investors remained cautious and assessed the outlook for monetary policy. This week's announcements of unexpected rate increases by the Reserve Bank of Australia and the Bank of Canada have fueled fears of potential hawkish action by other central banks. On the other hand, concerns about the economy's health are mounting. Recent data indicated that the euro zone economy entered a recession during the winter, and US claims data pointed to a declining labor market. Next week, the Federal Reserve and the European Central Bank will make policy decisions regarding monetary conditions. Alstom (2.6%), Stellantis (1.5%), and Michelin (1.5%) were the top-performing individual stocks. In an effort to increase capital utilization, Societe Generale consented to sell a portion of its African operations, resulting in a 1.2% increase in its share price. The FTSE MIB gained 0.8% on Thursday to finish at 27,275, indicating its third consecutive session of gains and outperforming regional peers. The banking sector was the primary contributor, with Mediobanca (2.3%), FinecoBank (1.9%), and Leonardo (1.7%) exhibiting the strongest performance. The Banca Monte Paschi Siena stock price increased by 0.7% as investors evaluated a possible merger with BPER Banca. CNH Industrial (+1.5%) and Stellantia (+1.4%) also increased. The IBEX 35 rose 0.5% to 9,350 on Thursday, outperforming its regional peers due to bank pressure. Bankinter's (1.2%) and Banco Sabadell's (1%) gains were the greatest in the financial statements. Investors also kept a close watch on Banco Santander (0.8%), which agreed to acquire the remaining 37.5% of Brazilian broker Toro Investimentos, and BBVA (0.2%), which accelerated its growth plans for the Italian market. In addition, Repsol (1.2%) and Inmobiliaria (1.1%) were among the companies with the greatest performance. Acciona Energia lost 1.8% while Amadeus IT lost 1.5%. Despite signing a deal worth approximately 1,400 million euros to construct a new stadium for the Buffalo Bills, Grupo ACS fell 0.3%. Overall, sentiment remained subdued as the market anxiously awaited next week's ECB and Fed decisions in the wake of the National Bank of Canada's unexpected rate hike.

On Thursday, the ruble-based MOEX Russia index continued to rise, propelled primarily by gains in the banking sector, while oil and gas producers remained relatively stable. In the first five months of this year, Moscow's budget deficit was the largest ever for the period, totaling 3,4 trillion rubles. This represents a significant increase in the deficit from the same period last year, when it was 1,6 trillion rubles, highlighting the challenging fiscal situation caused by low energy revenues and heavy war-related expenditure. Friday will see the release of Sberbank's interim financial statements, which investors are currently avidly anticipating.

Hong Kong stocks rose 47.18 points, or 0.25 percent, to 19,299.18 on Thursday, reversing a slight decline in early trade while trying to hold on to gains from the previous session amid speculation China could roll out new stimulus measures as soon as this month , and may introduce more measures at the Politburo meeting in July. Separately, some economists believe a housing-focused stimulus package may be on the horizon, given the deteriorating sentiment surrounding resale property listings and the decline in transaction volumes. Meanwhile, Reuters reported that China's largest bank has reduced deposit rates for renminbi today. However, gains were limited by caution ahead of Chinese inflation data on Friday and fears that the Federal Reserve may raise rates further the following week after Canada unexpectedly raised its key rate on Wednesday. Gains were led by the financial and real estate sectors, with the Country Garden real estate sector heading the way. Orient Overseas International (5.2%), Longfu Group Co., Ltd. (5%), Trip.Com (4.8%), and CITIC Limited (3.2%).

Nikkei 225 fell 0.85% to close at 31,641 and Topix fell 0.67% to 2,192, both benchmarks falling for a second consecutive day as investors continued to trade following a strong rebound in technology equities. Gain profit. Recently, robust corporate profits, a weak yen, and investor enthusiasm for artificial intelligence-related companies propelled Japanese stocks to a 33-year high, making them the best-performing equities in the world in May. Meanwhile, Japan's first-quarter GDP was revised up to 2.7% on an annualized basis, exceeding the consensus forecast of 1.9% and the initial reading of 1.5%. Index stalwarts such as SoftBank Group (-1.5%), Keyence (-3.5%), Fast Retailing (-0.8%), Sony Group (-1.7%), and Daikin Industries (-1.5%) experienced notable declines.

The S&P/ASX 200 fell 0.26% to 7010 on Thursday, marking the third consecutive session of declines, as losses in the technology and healthcare sectors outweighed gains in the mining and energy sectors. In April, Australia's exports declined at the quickest rate in nine months, while import growth accelerated to a three-month high. On Wednesday, data showed that Australia's economy grew 0.2% in the first quarter, the slowest pace in six quarters, missing forecasts for a 0.3% growth rate. Technology and healthcare stocks led the decline, tracking US peers down, with Xero (-5.6%), Wisetech Global (-3.1%), Rea Group (-3%), Resmed Inc. (-3%), and CSL Ltd. (-0.9%) falling. Meanwhile, mining and energy stocks rose on stronger commodity prices, with BHP Billiton Group (1.4%), Rio Tinto (2.2%), Fortescue Metals (1.8%), Woodside Energy (1.1%), and Santos (0.4%) rising.

New Zealand shares fell 73 points, or 0.62%, to 11,686 in early trade on Thursday, falling for a third day in a row while hovering at their lowest level in 10 weeks, with healthcare, utilities, and non-energy mining sectors falling. Wall Street's S&P 500 and Nasdaq closed lower on Wednesday, with traders taking profits after the broader market rallied and ahead of key economic and policy events next week. Investors were also unnerved by China's weak trade data for May, as both exports and imports fell on weak demand at home and abroad. In Australia, the economy grew at its weakest pace in six quarters in the first quarter of 2023, while the country's central bank unexpectedly raised the cash rate to an 11-year high of 4.1% earlier this week and warned of further tightening. Infratil had the biggest loss (-4.5%), followed by Fisher & Paykel Healthcare (-1.8%), Seeka Ltd. (-1.5%), Contact Energy Ltd. (-0.6%), and Marsden Maritime Holdings (-0.4%).

The Baltic Sea Freight Exchange's main index, which measures the cost of shipping goods around the world, rose 0.2 percent to 1,040 on Thursday, the highest level since May 31. The capesize index, which tracks ships typically carrying 150,000 tonnes of cargo such as iron ore and coal, rose 5.3% to 1,460; and the panamax index, which tracks ships that typically carry coal or grain cargoes of about 60,000 to 70,000 metric tons, rose 0.6 percent to 1,146. Meanwhile, the supramax index fell 19 points, or about 2.5 percent, to 747 points, its lowest level since late February.

REVIEWING THE LAST ECONOMIC DATA:

Reviewing the latest economic news, the most critical data is:

- US: U.S. utilities added 118 billion cubic feet of natural gas to storage in the week ended June 2, 2023, slightly more than the 111 billion cubic feet expected by the market, as mild weather limited demand for the heating and cooling fuel . Last week's increase brought inventories to 2.550 trillion cubic feet, 56.2 billion cubic feet above last year and 35.3 billion cubic feet above the five-year average of 2.197 billion cubic feet. Total working gas is 2.550 cubic feet, which is within the five-year historical range.

- US: In April 2023, U.S. wholesale inventories fell by 0.1% month-on-month, lower than the previous estimate of 0.2%, after a downward revision of 0.2% in March. Nondurable goods inventories fell (-1.2%, from -0.5% in March), led by pharmaceuticals (-0.8%), apparel (-2.3%) and agricultural products (-7.1%). Inventories of durable goods, on the other hand, rose 0.6% (unchanged in March). Wholesale inventories rose 6.3% compared to a year earlier.

- US: For the week ending May 27, 2023, U.S. Continuing Jobless Claims (which include people who have received unemployment benefits for a week or more) fell to 175,700 from 179,400, compared with expectations for 180,000. It was the lowest reading since mid-February.

- US: U.S. stocks vacillated between modest gains and losses on Thursday, as investors avoided big bets ahead of next week's Federal Open Market Committee decision. The claims report showed a larger-than-expected increase in first-time claims, suggesting strength in the U.S. labor market may be cooling. Chances of a 25 basis point hike in the Fed funds rate this month fell to 28% after the jobs data, from 32% earlier, but traders remained betting global rates would remain elevated for longer. The Bank of Canada and the Reserve Bank of Australia made unexpectedly hawkish moves earlier this week, which pressured U.S. Treasury yields to remain high. On the corporate front, shares of GameStop fell nearly 18% as its sales disappointed and its chief executive was fired. Meta shares also fell nearly 2 percent after EU industry chiefs demanded that the social media company take immediate action to address content targeting children.

- US: The number of Americans filing for unemployment benefits jumped to 261,000 for the week ending June 3, 2023, which includes the Labor Day holiday, the highest number since October 2021 and above the market forecast of 235,000 people. The previous week's figure was revised up slightly to 233,000 from an initial reading of 232,000. It marked the third straight week of increases in initial jobless claims, a sign that strength in the labor market may be fading. The 4-week moving average excluding weekly fluctuations is 237.25K, an increase of 7.5K from the previous week. According to unadjusted data, the largest increases in first-time claims were in Ohio (6.345 million), California (5.173 million), and Minnesota (2.746 million), while the largest decreases were in Connecticut (-235,000) and New York states (-124,300). Continuing claims, meanwhile, fell to 1.757 million from 1.794 million, the lowest level since mid-February and below forecasts for 180,000.

- EU: In the three months ending March 2023, employment in the euro area rose by 0.6% from the previous quarter to 166.4 million, in line with the preliminary estimate and up from 0.3% in the fourth quarter of 2022. It was the fastest job growth since the fourth quarter of 2021, further evidence that the job market remains tight despite the ECB's aggressive tightening measures. Estonia (4.4%), Spain (1.3%), Croatia (1.2%), and Portugal (1.2%) had the fastest job growth, offsetting Lithuania's (-1.5%), Romania's (-1.1%), and Greece's (-0.3%) decline. Employment rose at a 1.6% annual rate, up from 1.5% in the prior period and below an earlier estimate of 1.7%.

- EU: In the first three months of 2023, the euro zone economy unexpectedly shrank by 0.1% month-on-month, compared with early estimates of a modest growth of 0.1%. Figures for the final quarter of 2022 were also revised to show a decline of 0.1% instead of flat, meaning the Eurozone has now entered a mini-technical recession. Household spending fell by 0.3% in Q1 2023 (-1% in Q4 2022), due to the impact of high inflation and borrowing costs. Furthermore, public spending fell by 1.6% (vs. +0.8%) as the government withdrew stimulus measures designed to partially offset rising energy costs. On the other hand, gross fixed capital formation rebounded (+0.6% vs -3.5%). Also, exports fell by 0.1% (to -0.2%) and imports fell by 1.1% (to -2.5%). Among the EU's largest economies, GDP contracted in Germany (-0.3%) and the Netherlands (-0.7%), while GDP expanded in France (0.2%), Italy (0.6%), and Spain (0.5%).

- AU: Australia's imports of goods and services rose 1.6 percent year-on-year to a three-month high of A$45.02 billion in April 2023, on the back of strong domestic consumption as the economy fully emerges from COVID-19 restrictions. Purchases of consumer goods rose 0.7 percent to A$11.63 billion, boosted by food and beverages mainly for consumption (8.5 percent) and consumer goods not otherwise specified (0.5 percent). Elsewhere, imports of capital goods rose 7.2 percent, driven by civil aircraft and classified goods (103.4 percent), and industrial transportation equipment (14.6 percent). Machinery and industrial equipment (4.7%). Services purchases rose 3.7 percent to $8.73 billion, led by gains in transport (2.4 percent) and other services (0.9 percent). Meanwhile, imports of intermediate and other goods were flat at A$15.16 billion, while non-monetary gold imports fell 39.8 percent to A$447 million.

- AU: Australia's trade surplus fell to A$11.16 billion in April 2023 from a downwardly revised A$14.82 billion in the previous month, missing market forecasts for an increase of A$14 billion. It was the smallest trade surplus since last January, with exports falling and imports rising. Shipments fell 5 per cent from the previous month to a nine-month low of A$56.18 billion, dragged down by sales of metal ore and minerals, with total exports to China's largest trading partner falling 15.4 per cent from the previous month. Imports, meanwhile, rose 1.6 per cent to a three-month high of A$45.02 billion.

- JP: The value of loans in Japan rose 3.4% year-on-year in May 2023, up from 3.2% in April, marking the fastest growth rate in two years, as the country's continued economic recovery and higher input costs boosted corporate credit needs. Outstanding loans held by the country's major, regional and "new gold" banks stood at 602.3 trillion yen. Major and regional banks were the main drivers of loan growth, rising 4% and 3.6%, respectively, while "new gold" banks rose 1.1%.

- UK: The gap between the proportion of respondents to the Royal Institution of Chartered Surveyors (RICS) UK Residential Market Survey, which measures rising and falling house prices, rose from -39 in April to -39 in May 2023, the highest reading in six months and above forecasts of -38. However, concerns over persistent inflation and further rate hikes by the Bank of England are expected to dampen demand and pressure prices in the coming months. Tarrant Parsons, senior economist at RICS, said: "The latest survey feedback points to a slight recovery in sales market activity in May, with an overall less negative impact compared with the end of 2022. However, storm clouds appear to have gathered and the UK's stubborn Higher inflation could prompt further action by the Bank of England through rate hikes, leading to higher mortgage rates and ultimately reducing affordability and buyer demand, undermining the recent improvement in activity."

LOOKING AHEAD:

Today, investors should watch out for the following important data:

- CNY: CPI y/y, PPI y/y, New Loans, and M2 Money Supply y/y.

- CAD: Employment Change, Unemployment Rate, and Capacity Utilization Rate.

- JPY: M2 Money Stock y/y.

- EUR

Italian Industrial Production m/m

KEY EQUITY & BOND MARKET DRIVERS:

Кey factors in the stock and bond market are currently:

- US: U.S. 10-year Treasury yields briefly touched 3.82% before falling below 3.75% after initial jobless claims jumped to their highest level since October 2021, reducing expectations for a Fed rate hike next week and in July. Currently, market participants see a 72 percent chance that the Fed will keep rates unchanged this month, with about 50 percent expecting a 25 basis point hike in July. Traders now await further clarity on inflationary pressures from the U.S. CPI report due on Tuesday and PPI on Wednesday, the last key economic indicators before the Federal Open Market Committee's decision later on Wednesday.

- US: U.S. futures were flat on Thursday as investors continued to assess the outlook for monetary policy, with expectations for rate hikes persisting. The Fed will decide on monetary policy next week, and the odds of a 25 basis point rate hike have been rising, currently at 32%. Additionally, investors see a 52% chance of a rate hike in July. Due to unexpectedly hawkish actions by the Bank of Canada and the Reserve Bank of Australia earlier this week, U.S. Treasury yields were also higher. On the corporate front, GameStop shares fell nearly 18% in premarket trading after its sales disappointed and its chief executive was fired. Meta shares also fell nearly 1% after EU industry chiefs demanded that the social media company take immediate action to address content targeting children.

- IN: The yield on India's 10-year government bond was around 7%, near its lowest level in a year, as investors digested the economic and currency outlook. The Reserve Bank of India held borrowing costs steady for a second straight meeting in June, in line with market expectations, but said monetary conditions would remain tight and signaled further action could be taken to curb inflationary pressures if necessary. RBI Governor Shaktikanta Das also stressed that the move was not a policy shift. India's inflation rate was back in the tolerable range of 2%–6% in April, but the impact of the monsoon outlook and El Niño on prices remains uncertain. Meanwhile, high U.S. Treasury yields continued to dampen investor appetite.

- CN: Yields on 10-year Chinese government bonds have been falling since the start of the year, hovering at 2.7%, near their lowest level since November. Concerns are growing about a sluggish economic recovery and a weakening outlook for China's economy. The latest data showed exports fell more than expected and imports were lower, while the official manufacturing PMI showed factory activity contracting for a second straight month. The dismal numbers have raised expectations that Chinese authorities will introduce additional stimulus measures to support the economy, possibly including lowering the reserve requirement ratio for banks. However, China's largest bank recently cut interest rates on a range of yuan and dollar deposit products.

- GE: Germany's 10-year government bond yield climbed to 2.5%, approaching a 2-1/2-month high of 2.556% hit on May 26, on expectations the main central bank will hike rates further and keep them there for longer to tackle inflation pressure. Market participants expect the ECB to raise interest rates to a peak of around 3.75% later this year from the current 3.25%. Many investors expect a 25 basis point hike this month and next. Bank of Canada Governor Christine Lagarde recently emphasized that inflation in the euro zone remains high, suggesting further monetary tightening is needed. Elsewhere, the Federal Reserve is also scheduled to announce its rate decision next week, while the Reserve Bank of Australia and the Bank of Canada surprised markets by raising rates by 25 basis points each at their recent meetings after pausing.

- AU: Australian government bond yields topped 4%, the highest since early January, and tracked a rise in global bond yields. On June 6, the Reserve Bank of Australia unexpectedly raised interest rates by 25 basis points to an 11-year high of 4.1%, saying further monetary tightening may be needed to bring inflation back into the target range. The next day, the Bank of Canada also surprised markets by increasing borrowing costs by 25 basis points. The surprise moves added to speculation that global interest rates will need to remain higher for longer due to higher inflation. In Australia, inflation is expected to return only to the upper end of the Reserve Bank of Australia's 2-3% target range by mid-2025. Treasury Secretary Jim Chalmers said the economy grew 0.2% in the first quarter, below forecasts for 0.3% and the weakest growth since the COVID-19 outbreak in the third quarter of 2021, suggesting that "interest rates The rise is clearly unpleasant."

LEADING MARKET SECTORS:

- Strong sectors: Consumer Discretionary, Consumer Staples, Information Technology.

- Weak sectors: Real Estate, Materials, Energy, Financials.

TOP CURRENCY & COMMODITIES MARKET DRIVERS:

Кey factors in the currency and commodities market are currently:

- EUR: The euro traded around $1.07, holding near a two-month low of $1.0633 touched on May 31, as investors awaited next week's European Central Bank monetary policy meeting after the latest data showed the euro zone economy slipped into recession. Higher interest rates started to take their toll on the EU economy, as revised GDP figures showed the euro zone contracted by 0.1% in the first quarter, instead of the 0.1% expansion initially forecast, and the fourth quarter was also revised down from flat to 0.1% shrinkage. Meanwhile, data showed a sharper-than-expected slowdown in consumer and producer prices, but European Central Bank President Christine Lagarde said inflation remained elevated, signaling a possible future rate hike. Elsewhere, the Federal Reserve is also scheduled to announce its rate decision next week, while the Reserve Bank of Australia and the Bank of Canada surprised markets by raising rates by 25 basis points each at their recent meetings after pausing.

- JPY: The yen held around 139 per dollar, close to a six-month low of 140 hit in late May, as the Bank of Japan maintained its ultra-low interest rate policy despite market pressures and persistent inflation. In contrast, major central banks continue to stick to tight monetary policies. Both the Bank of Canada and the Reserve Bank of Australia unexpectedly raised interest rates, raising expectations that the Fed will raise rates again in July. Meanwhile, the latest data showed that Japan's economy grew much more than expected in the first quarter.

- OIL: Brent crude futures fell more than 3 percent to below $74.5 a barrel on Thursday after reports that Iran and the United States were close to an interim deal that would trade sanctions relief in exchange for a reduction in Iran's uranium enrichment. Throughout the week, oil prices were relatively flat as weak demand indicators such as rising U.S. fuel inventories and sluggish Chinese economic data trumped expectations of tighter supply from Saudi Arabia. At the OPEC+ meeting on Sunday, Saudi Arabia announced a further 1 million bpd cut in crude output for July to boost lagging prices.

- GAS: U.S. natural gas futures fell 1 percent to $2.3/MMBtu on Thursday, ending a four-day winning streak after the EIA reported a slightly larger-than-expected storage build last week as mild weather supported demand for fuel. Despite this setback, expectations of increased demand from air-conditioning use amid forecasts of warmer weather supported U.S. natural gas prices. The number of cooling degree days (CDD) over the next two weeks is expected to rise to 167, above the 30-year normal of 149, according to Refinitiv.

- GLD: Gold prices rose nearly 1 percent to near $1,960 an ounce on Thursday, benefiting from a slightly weaker dollar after higher-than-expected initial jobless claims data raised concerns about the health of the U.S. economy. Still, gold prices remain well below the near-record high of $2,050 reached on May 5 as traders expect interest rates to remain high for an extended period. Both the Reserve Bank of Australia and the Bank of Canada surprised markets this week by providing another 25 basis point increase in borrowing costs.All eyes are now on next week's FOMC meeting, with nearly 72% of traders expecting the Fed to leave the Fed funds rate on hold. Meanwhile, the ECB is set to raise interest rates further next week as well.

CHART OF THE DAY

On Thursday afternoon, all three main U.S. stock indexes were in positive territory, with the Dow up more than 100 points and the S&P 500 up 0.5%. As U.S. Treasury yields declined, large-cap equities advanced, propelling the Nasdaq to the top of Wall Street gains. While awaiting inflation data and the Federal Open Market Committee meeting next week, investors digested jobless claims data that exceeded expectations. The number of Americans filing for unemployment benefits increased substantially more than anticipated last week, reaching its greatest level since 2021, indicating that the U.S. labor market may be cooling. Amazon's stock increased by nearly 3 percent, while Tesla's rose by the same amount. Carvana's stock price increased by 45 percent after the company issued an optimistic forecast for the second quarter. Instead, GameStop's stock fell nearly 18% following disappointing sales and a poor performance by its fifth CEO in five years.

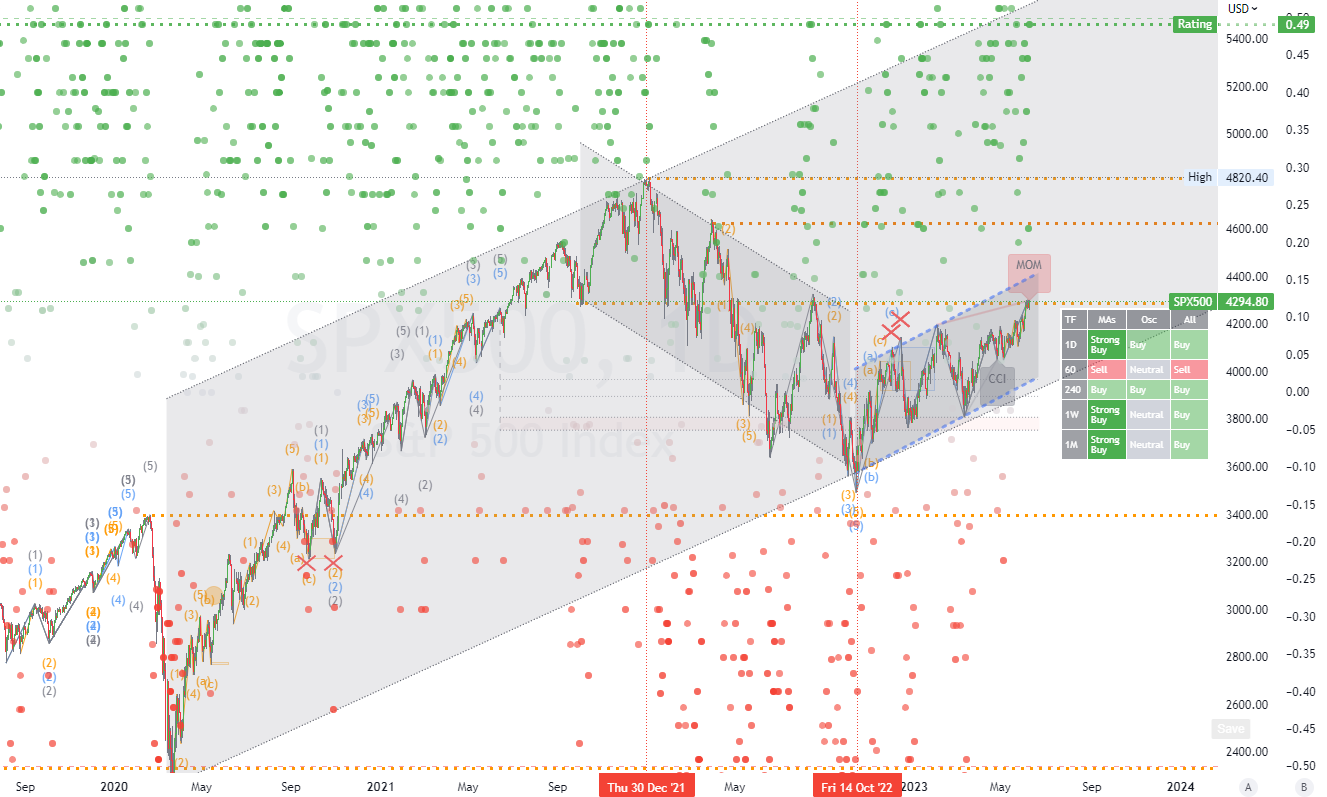

long-term Channels Trading Strategy for: (S&P 500 index).Time frame (D1). The primary resistance is around (4400). The primary support is around (4000). Therefore, the next most probable price movement is a (consolidation/down) trend. (*see all other details on the chart).

Start trading in four simple steps

1. Register

Open your live trading account

2. Verify

Upload your documents to verify your account

3. Fund

Deposit funds directly into your account

4. Trade

Start trading and choose from 130+ instruments

Demo account

The Blue Suisse Trading Account with virtual funds in a risk-free environment

Demo accountLive account

The Blue Suisse Trading Account in our transparent live model environment

Open an Account- Trading Account types Trading conditions Trading hours Transparency Market Information

- Products Currencies Commodities Indices Stocks

- Tools MetaTrader 4 / 5 Mobile CRM, MAM and DSP

- Education Currency Trading for Beginners How to improve your trading CFD Trading

- Partnerships Asset- and Moneymanager Tied agent White labels FIX API

- Company About us Regulatory Our philosophy Careers FAQs Contact us