Rising Treasury yields, Weakness in mega cap stocks, Pro-cyclical vibe, DXY steady on inflation, Fed next week; The Turkish lira hit a new record low

GLOBAL CAPITAL MARKETS OVERVIEW, ANALYSIS & FORECASTS:

Author: Dr. Alexander APOSTOLOV (researcher at Economic Research Institute at BAS)

Wednesday was a flat day for major European stock markets as investors shied away from large wagers in the face of economic uncertainty and the possibility of additional interest rate hikes at next week's European Central Bank meeting. China's latest trade data revealed exports fell more than anticipated and imports were lower, indicating a feeble recovery in the second-largest economy in the world. After the owner of Zara surpassed revenue and sales forecasts, banking and retail equities inched higher, while Inditex climbed roughly 5 percent. In contrast, mining and luxury equities experienced losses. On Wednesday, the FTSE MIB recovered from early losses to close just above the neutral line at 27,055, as gains in technology stocks offset losses in banks and utilities, and investors continued to assess the impact of the ECB's policy tightening. After announcing a new joint venture with Sanan to construct a manufacturing plant in China, STMicroelectronics boosted its stock price by 3.2 percent, boosting the sector's average gain to almost 3 percent. Investors continued to evaluate the possibility of a merger between Banca Monte Paschi Siena and BPER Banca, which resulted in banks paring back some of the steep gains made in the prior session. The CAC 40 was nearly unchanged at 7,203 on Wednesday as traders continued to evaluate generally disappointing macroeconomic data while keeping a watch on next week's monetary policy decisions from the Federal Reserve and the European Central Bank. In the meantime, recent rate increases in Canada and Australia have unnerved investors. Renault (-2.5%) was the worst performer among individual equities, followed by Thales (-1.9%), Danone (-1.5%), and Sanofi (-1.5%). The IBEX 35 rose to 9,359 on Wednesday, outperforming regional competitors, as a 5.69% increase in Inditex shares moved the company's market capitalization above 100 billion euros. The proprietor of Zara reported a 54% increase in net profit to 1.168 million euros for the first quarter ending in April, the highest amount for such a period. It was also a positive day for Sacyr (+2.41%) and IAG (+1.51%), which rose after JB Capital and JP Morgan upgraded their recommendations. After receiving nearly €34 million for the deployment of a "Development, Training, and Testing Center for Military Operations in Cyber Defense with 5G Technology" for the Ministry of Defense, Telefonica reversed earlier losses to close 1.70% higher. Acciona Energia and Laboratorios Farma, on the other hand, were the most prominent bears, falling approximately 1.7% each.

The FTSE 100 fluctuated around the flat line of 7,625 on Wednesday, extending gains since June, as indications of a slowing global economy reminded investors of upcoming interest rate increases by major central banks. In May, China's exports declined significantly, indicating weak foreign demand. According to the Halifax survey, aggressive rate increases by the Bank of England led to the first annual decline in home prices since 2012. Oil companies traded in London declined, with BP and Shell falling 0.7% each, as crude prices continued to decline following Saudi Arabia's weekend output cut. Banks, on the other hand, support the index, with HSBC and Lloyds being particularly supportive.

The ruble-based MOEX Russia index rose 0.5% to close at 2,695 on Wednesday, erasing the previous session's losses as investors digested the most recent government budget data. In the first five months of this year, Moscow posted a budget deficit of 3,4 trillion rubles, the largest on record for the period, compared to 1,6 trillion rubles a year earlier, highlighting the country's struggles with low energy revenues and soaring war expenditure. precarious financial situation. Consequently, energy companies underperformed, with Bashneft shares declining 1.4%. However, the demand for dividend payments in the near future supports stocks. VTB shares climbed 2.3% after the bank reported robust results for the first four months of 2023, propelling the sector nearly 40% higher so far this year.

The Dow attempted a 50-point gain on Wednesday, while the S&P 500 traded near a flatline but near its highest level since August 2022, and the Nasdaq gave up early gains to decline 0.3%. Next week's inflation reports and the Federal Reserve's monetary policy decision kept investors on the sidelines. Traders currently assign a probability of 67% that the Fed will maintain the Fed funds rate, down from 77% earlier in the session, but a probability of 52% for a 25 basis point hike in July. After the Bank of Canada unexpectedly raised interest rates by 25 basis points, U.S. Treasury yields increased, which weighed on the technology sector. Caterpillar (3.1%), 3M (2.1%), and Chevron (2%) were the top Dow performers, respectively. In addition, JPMorgan Chase raised its price target for Netflix, which led to a nearly 2% increase in its stock price, and Marvell soared more than 2% on news that it had signed an artificial intelligence chip contract with Amazon.

The Baltic Exchange's primary shipping index increased for a third consecutive day on Wednesday, increasing approximately 0.4% to a three-month high of 1,020 points. The capesize index, which tracks ships typically carrying 150,000 metric tons of cargo such as iron ore and coal, rose 4 points to a three-month high of 1,387; and the panamax index, which tracks ships that typically carry coal or grain cargoes of about 60,000 to 70,000 metric tons, added 31 points, or about 2.8 percent, to 1,119 points. The supramax index dropped 15 points, or approximately 2%, to 766 points.

Australia's S&P/ASX 200 fell 0.16% to 7,118 on Wednesday, marking a second straight session of losses after data showed Australia's economy grew 0.2% in the first quarter, the slowest pace in six quarters , and missed forecasts for a 0.3% increase due to weak household consumption. On Tuesday, the Reserve Bank of Australia also raised the cash rate to an 11-year high of 4.1%, saying the increase would increase confidence that inflation will return to target within a reasonable time and further tightening may be required. Energy stocks led losses, with Woodside Energy (-0.4%), Santos (-0.9%), and Beaches Energy (-8.1%) leading the way. Financial firms also fell, including Commonwealth Bank (-09%), Westpac (-1.5%), National Australia Bank (-1.8%), and ANZ Banking Group (-0.05%).

New Zealand stocks fell 72 points, or 0.6%, to 11,810 in early trade on Wednesday, marking a second straight session of losses, dragged down by losses in the healthcare, non-energy minerals, energy minerals, and business services sectors. 2023 will be one of the slowest years for advanced economies to grow in the past 50 years, with higher interest rates and tighter credit weighing more heavily on next year's numbers, the World Bank said in a report on Tuesday. worried about this. There is also growing caution about the health of the Chinese economy ahead of trade data due later in the day and an inflation report on Friday. U.S. stocks were upbeat on Tuesday, with a rotation in financials raising hopes that the S&P 500's recent gains could soon outpace technology stocks. Seeka Ltd. fell 3.6 percent, Ebos Group fell 3.2 percent, while Serko Ltd., Port of Tauranga, and Mercury NZ Ltd. fell 1.2 percent, 1.1 percent, and 1 percent, respectively.

The Shanghai Composite Index rose 0.4% to close above 3,200 points, and the Shenzhen Stock Exchange constituent stocks fell 0.2% to close at 10,750 points, showing mixed results. Mainland stocks are struggling to find direction as investors cautiously await Chinese trade data for more economic cues. Chinese stocks have come under pressure in recent sessions as weaker-than-expected data pointed to a challenging recovery path for the country. On Monday, Hongbo shares (10%), HKUST Xunfei (2.6%), and Chengdu Information (8.4%) rose significantly, while Dangdai Ampere (-5.7%), Alpha Group (-1.9%), and BYD (-1.4%) fell .

India's BSE Sensex rose 350 points to 63,140 on Wednesday, its highest since reaching an all-time high in early December, as investors continued to welcome the Reserve Bank of India's dovish policy expectations amid evidence of moderating inflation in the Indian economy. The central bank will keep interest rates on hold in a decision tomorrow, with investors ramping up bets for a rate cut at the end of the third quarter. On the corporate front, metals, technology, and consumer goods companies led gains, with TCS, Infosys, Tata Steel, and Hindustan Unilever closing 1% to 0.5% higher.

REVIEWING THE LAST ECONOMIC DATA:

Reviewing the latest economic news, the most critical data is:

- CA: After pausing tightening at its previous two meetings, the Bank of Canada unexpectedly raised its overnight rate target by 25 basis points to 4.75% in June 2023, while markets expected rates to remain unchanged. Borrowing costs are now at levels not seen in 22 years, as policymakers believe monetary policy is not restrictive enough to bring supply and demand back into balance and sustainably return inflation to the 2% target. With the annual CPI rising to 4.4% in April, the first rise in 10 months, concerns have grown that inflation could run well above the 2% target, with the three-month measure of core inflation falling for several months. Operating in the 3.5–4% range, excess demand persists. The Bank continues to assess the dynamics of core inflation and the outlook for CPI inflation, and is firmly committed to restoring price stability to Canadians.

- CA: Canada's exports rose 2.5% to $64.9 billion in April 2023 after two consecutive months of decline, with gains in six of 11 product sectors. Unwrought gold exports (up 46.0%), which are primarily the result of increased transfers of gold assets by Canadian financial institutions to the United States, contributed the most (up 11.6%). Exports of energy products also rose (+6.4%) as higher prices led to a rebound in crude oil sales (+7.1%) after a six-month decline. In addition, coal exports rose due to higher shipments to South Korea. Meanwhile, exports of motor vehicles and parts surged (+7.4%). Among the main trading partners, overseas sales mainly increased in South Korea (+35.2%), Italy (+15.2%), and the United States (+4.4%), but fell in the United Kingdom (-34.4%), Germany (-24.8%), and China (-14.7%).

- CA: Canada posted a trade surplus of C$1.94 billion in April 2023, above market forecasts of C$900 million and well above last month's downwardly revised surplus of C$230 million. Exports rose 2.5 percent to C$64.8 billion amid record volumes, helped by a 46 percent surge in unwrought gold sales, as higher volumes coincided with higher gold prices over the same period. Also, energy exports rose sharply (4.6%) as higher oil prices boosted crude exports (7.1%), while sales of motor vehicles and parts rose 7.4%. Imports, on the other hand, fell 0.2% to C$62.9 billion, as declines in purchases of energy products (-12.8%) outweighed increases in imports of consumer goods (4%).

- CA" Imports to Canada fell 0.2% month-on-month to $62.9 billion in April 2023, the third consecutive month of decline, with declines in seven of 11 product sectors. Imports of energy products (-12.8%) fell the most in April, while imports of crude oil (-20.5%) fell, partly due to lower shipments from Saudi Arabia and the US. Imports of refined petroleum products also fell sharply (-11.7%), mainly due to lower imports of motor gasoline from the United States. Consumer goods purchases increased 4.0% in April as a result of higher pharmaceutical product imports (+28.1%). Among the main trading partners, purchases were mainly from Switzerland (-17.1%), Italy (-101%), the UK (-9.2%), China (-8.9%), and the USA (-0.4%), but also from the Netherlands (+ 55.6%).

- US: The Mannheim Used Car Value Index, which tracks used car prices at U.S. wholesale auctions, fell 2.7% in May 2023 after falling 3% in April. Seasonal adjustments continue to have a downward impact. Prices fell for compact cars (-2.4 percent), midsize cars (-2.5 percent), luxury cars (-3 percent), and pickup trucks (-4.3 percent), while SUVs were flat and vans edged up 0.2 percent. Used car prices fell 7.6% from a year earlier, the biggest annual drop in four months. However, "over the next few months, the rate of decline is likely to slow as we encounter the lower prices seen at auctions from May to November last year. By any measure, two readings in a row are not a trend, as pre-owned retail inventory remains lower than last year, which tends to keep buyers at auction, supporting prices." x Auto.

- US: Imports to the U.S. rose $4.8 billion from the previous month to $323.6 billion in April 2023, recovering from two consecutive months of decline. Imports of goods rose $5.2 billion, led by higher purchases of motor vehicles, parts, and engines (up $2.0 billion), finished metals (up $1.5 billion), nonmonetary gold (up $1.10). billion), organic chemicals (up $900 million), and cell phones and other household goods (up $1.7 billion). On the other hand, imports of crude oil (-$800 million) and natural gas (-$8 trillion) fell. In addition, imports of services fell by $400 million due to transportation (-$400 million) and tourism (-$200 million).

- US: In April 2023, the U.S. trade deficit widened to a six-month high of $74.6 billion, compared with a gap of $60.6 billion in March and a market forecast gap of $75.2 billion. Crude oil, fuel oil, pharmaceutical preparations, gemstones and diamonds, jewelry, financial services, and government goods and services were the top exports, which saw a 3.6 percent decline to $249 billion, while tourism sales increased. Imports, meanwhile, rose 1.5 percent to $323.6 billion, led by passenger vehicles, industrial supplies and materials, finished metals, non-monetary gold, organic chemicals, mobile phones and other household items, while crude oil, natural gas, transportation and travel Purchases of services declined. The countries with the largest deficits were China ($24.2 billion), the European Union ($17.3 billion), Mexico ($11 billion), and Vietnam ($8.5 billion); surpluses occurred in the Netherlands ($4.2 billion), South and Central America ( 4.1 billion), as well as Belgium ($1.9 billion) and Hong Kong ($1.6 billion).

- US: U.S. exports fell $9.2 billion from the previous month to $249 billion in April 2023, the lowest level since March 2022. Merchandise exports fell $9.4 billion due to crude oil (down $2.1 billion), fuel oil (down $1.1 billion), pharmaceutical preparations (down $500 million), gemstones and diamonds (down $400 million), and jewelry (down $4 trillion USD). On the other hand, exports of services increased by $0.2 billion, mainly due to travel (up $0.5 billion) and other business services (up $0.3 billion).

- US: The average U.S. contract rate for 30-year fixed-rate mortgages with eligible loan balances ($726,200 or less) fell 10 basis points to 6.81% for the week ended June 2, 2023. It was the first decline in four weeks, while 6.91% was the highest since early November. Still, borrowing costs are rising as the Fed needs to keep the federal funds rate higher for longer. With the debt ceiling impasse over, the second week of June's inflation report and the Fed's monetary policy decision should be the next big catalyst for mortgageUS: U.S. mortgage applications fell 1.4% for the week ended June 2, 2023, marking the fourth straight weekly decline and pushing the mortgage market index to a new three-month low, according to the Mortgage Bankers Association. Joel Kan, MBA deputy chief economist, stated that "lower purchasing power from higher interest rates and a persistent lack of unsold inventory in the market have constrained purchasing activity while interest rate incentives for refinancing borrowers remain minimal." Applications to buy a home fell 1.7%, while applications to refinance a home loan fell 0.7%. Meanwhile, the average contract rate on 30-year fixed-rate mortgages with eligible loan balances ($726,200 or less) fell to 6.81% from 6.91%, the first drop in four weeks and the highest level since early November rates.

- TW: Imports to Taiwan fell 21.7% year-on-year to US$31.25 billion in May 2023, down from 20.2% in the previous month and more than the market forecast of a 20.8% drop. This was the largest drop since September 2015, as purchases of all major commodities continued to decline: electronics parts (-32.1%), mineral products (-29.4%), machinery (-10.8%), chemicals (-36%), and base metals (-27.4%). In terms of trading partners, from the Middle East (-28.1%), China and Hong Kong (-27.2%), ASEAN countries (-24.3%), Japan (-17.3%), and Europe (-14.5%). In contrast, imports from the US increased (5.1%). In the first five months of this year, imports were down 18 percent compared to the same period last year.

- TW: In May 2023, Taiwan's trade surplus widened to US$4.89 billion, more than double the US$2.12 billion in the same month of the previous year and slightly below market expectations of US$5 billion. Exports fell 14.1% year-on-year to $36.11 billion, led by electronics components (-9.9%), base metals (-24.6%), machinery (-12.4%), plastic rubber (-31.1%), machinery (-10.8%), chemicals (-36%), and base metals (-27.4%). Consider that the trade surplus rose slightly to $20.5 billion in the January–May period from $20.25 billion in the same period in 2022.

- GE: In April 2023, German industrial production increased by 0.3% month-on-month, recovering from a downwardly revised 2.1% decline in March but lower than the market forecast for a 0.6% increase. The increase was driven by a rebound in the construction sector (2 percent compared to -2.9 percent in March), as well as gains in the manufacturing of basic pharmaceutical products and pharmaceutical preparations (6.4 percent) and consumer goods (1.5 percent). However, motor vehicles and parts, engineering (-0.5%), capital goods (-0.3%), intermediate goods (-0.2%), and energy (-1.5%) Excluding energy and construction, industrial output rose 0.1%. Industrial production rose 1.6% from a year earlier, down from a 2.3% rise in March.

- UK: In May 2023, the Halifax house price index in the UK fell by 1% year-on-year, which was the first decline since December 2012, in line with market expectations. House prices were flat compared to the previous month. A brief upturn in the housing market in the first quarter of the year has faded, with the impact of rising interest rates trickling down to household budgets. Apartment prices experienced the largest drops (-1.9%), followed by terraced houses (-1.0%) and semi-detached houses (-0.5%), while detached house prices increased by 0.4%. Prices of existing homes continued to fall (-1.9%), while those of new builds continued to rise (+2.8%), albeit at the slowest pace in almost three years. The typical UK property price is now £286,532, compared to £286,662 in April .

- AU: The Australian economy grew by 0.2% quarter-on-quarter in the first quarter of 2023, below the consensus forecast of 0.3%, after an upward revision of 0.6% in the fourth quarter. It was the sixth straight period of economic growth, but at the slowest pace, as household consumption rose the least in six quarters (0.2 percent in the fourth quarter compared with 0.3%). The household savings rate fell to 3.7 percent from 4.5 percent previously, the lowest level since the second quarter of 2008. In addition, growth in government spending slowed sharply (0.1% versus 0.6%), while net trade had a negative impact on exports (1.1%), which grew less than imports (3.2%). In the meantime, machinery and equipment, non-residential and residential, and intellectual property products drove a rise in private investment (1.4% vs. -0.9%). Public investment increased (3.0% vs. -1.2%) due to increases in state and local governments, state and local corporations, and the nondefense sector. For the full year, the economy grew 2.3%, down from 2.7% growth in the fourth quarter.

- JP: Japan's reserve assets fell slightly to $1.255 trillion in May 2023 from an eight-month high of $1.265 trillion in April, largely due to a decline in foreign exchange reserves. Total reserve assets are divided into foreign exchange reserves ($1.126 trillion), IMF reserve positions ($1.0626 billion), special drawing rights ($5.8304 billion), gold ($5.343 billion), and other reserve assets ($5.779 billion). In October, official data showed that Japanese authorities spent a total of 6.35 trillion yen in foreign exchange intervention in November and December to support the currency, but took no further action. Meanwhile, the latest data showed that the government did not engage in currency intervention in the first quarter of this year.

LOOKING AHEAD:

Today, investors should watch out for the following important data:

- EUR: French Final Private Payrolls q/q, Final Employment Change q/q, and Revised GDP q/q.

- GBP: RICS House Price Balance.

- JPY: Bank Lending y/y, Current Account, Final GDP Price Index y/y, Final GDP q/q, and Economy Watchers Sentiment.

- USD: Unemployment Claims, Final Wholesale Inventories m/m, and Natural Gas Storage.

- NZD: Manufacturing Sales q/q.

- AUD: Trade Balance.

- CHF: SNB Chairman Jordan Speaks.

- CAD: Gov. Council Member Beaudry Speaks.

KEY EQUITY & BOND MARKET DRIVERS:

Кey factors in the stock and bond market are currently:

- US: U.S. 10-year Treasury yields traded above the 3.75% level, approaching a more than two-month high of 3.8% hit on May 26, as concerns over persistent higher-than-expected inflation boosted sentiment that the Federal Reserve will raise interest rates again. Reflecting similar concerns about the United States, both the Reserve Bank of Australia and the Bank of England unexpectedly raised interest rates this week, citing borrowing costs not being tight enough to bring inflation back to target. As a result, the market sees a 70% chance that the U.S. central bank will raise rates by at least 25 basis points before its July meeting. Investors are now awaiting key inflation data next week, which will cement another Fed rate hike after the latest jobs report showed the U.S. added 339,000 jobs in May.

- CA: Canada’s 10-year government bond yield jumped more than 12 basis points in June, near a three-month high of 3.4%, after the Bank of Canada unexpectedly raised rates by another 25 basis points and signaled it could raise rates further if needed. The central bank said excess demand in the economy appeared to be more persistent than expected, and inflation was likely to run well above its 2% target. The central bank is widely expected to keep interest rates steady at its third meeting. The Canadian economy expanded more than expected in the first quarter, and the labor market remains tight, while inflation rose to 4.4 percent in April for the first time in ten months, more than double the Bank of England's target.

- CA: The loonie gained more than 1.335 against the U.S. dollar in June, its strongest level in two months, after the Bank of Canada defied market expectations and raised its key interest rate by 25 basis points to 4.75%. The decision, which marks the restart of the central bank's tightening cycle after three straight hikes, runs counter to the central bank's signal that rates may have peaked and suggests that borrowing costs in the Canadian economy are not as constrained as policymakers had expected. After raising rates, policymakers maintained their forecast that headline inflation would slow to 3% by the summer, although the bank warned that price growth was likely to remain above its 2% target. The latest data showed that Canadian CPI rose 4.4% in April, well above the market forecast of 4.1% and higher than March's 4.3%. At the same time, crude oil prices rebounded from recent lows, supporting the buying activity of maniacs.

- FR: In April 2023, France announced a current account deficit of 100 million euros, which was different from the surplus of 300 million euros revised down last month, but exceeded market expectations for a gap of 800 million euros. The deficit in the goods account widened from €6.2 billion to €7 billion due to higher energy bills; while the gap in secondary income remained unchanged at €3.5 billion. On the other hand, the services surplus rose from 3.7 billion euros to 4.2 billion euros, driven by growth in tourism services; while the primary income surplus also reached 6.2 billion euros. In April 2022, the country's current account deficit was 4.4 billion euros.

- FR: France's trade deficit widened to 9.7 billion euros in April 2023, after an upward revision of 8.4 billion euros the month before, above market forecasts of 7.7 billion euros. Imports rose by 1.4% month-on-month to 59.5 billion euros. Exports, meanwhile, decreased 0.1% to 49.8 billion euros, with a decline in energy exports and a slight increase in non-energy exports as the main drivers. The energy gap ballooned to 6.8 billion euros from 5.4 billion euros in March. Excluding energy, the trade deficit edged down to 4.9 billion euros from 5 billion euros. With regard to manufacturing, the trade balance of consumer goods decreased slightly (-100 million), while the trade balance of capital goods and intermediate goods increased slightly, each by 100 million.

LEADING MARKET SECTORS:

- Strong sectors: Energy, Utilities, Real Estate, Materials, Industrials.

- Weak sectors: Communication Services, Information Technology, Consumer Discretionary, Health Care, Consumer Staples.

TOP CURRENCY & COMMODITIES MARKET DRIVERS:

Кey factors in the currency and commodities market are currently:

- USD: The U.S. dollar index was little changed at around 104 on Wednesday, reflecting caution over inflation data and the Federal Reserve's decision next week. The Fed is expected to keep rates on hold this month, but markets are pricing in a possible rate hike in July. Consumer inflation data for May is expected to show a 0.30% rise in prices, which could influence the Fed's decision. In addition, investors have been unwinding long-term bets on the dollar, which are considered a hedge until the U.S. government raises the debt ceiling. Markets are monitoring the U.S. Treasury's increase in Treasury issuance to rebuild cash balances, as any potential demand issues could weigh on markets. According to the most recent data, higher imports and lower exports caused the U.S. trade deficit to widen in April. Elsewhere, recent rate hikes by the Bank of Canada and the Reserve Bank of Australia lured investors away from the greenback.

- OIL: U.S. crude inventories fell by 451,000 barrels in the week ending June 2, 2023, compared with market expectations for a draw of 1.022 million barrels, according to the EIA Oil Status Report. Crude inventories at the Cushing, Oklahoma, delivery hub, on the other hand, rose by 1.721 million barrels after rising by 1.628 million barrels. Elsewhere, gasoline inventories rose by 2.746 million barrels, beating forecasts for a 880,000-barrel increase, while distillate stockpiles, which include diesel and heating oil, surged by 5.075 million barrels, the most since early December, beating consensus estimates of 1.328 million barrels. Brent crude futures rose to $77 a barrel on Wednesday, recovering from a 0.6% loss in the previous session, as traders weighed the prospect of tighter supplies against concerns about weakening global demand. Saudi Arabia, the world's top oil exporter, announced over the weekend its intention to cut output by 1 million barrels a day to 9 million barrels a day in July, the lowest level in years, amid efforts to raise raw material prices. The latest EIA report also showed U.S. crude inventories fell by 451,000 barrels last week, missing expectations for a 1.022 million barrel increase and in line with industry data reported on Tuesday.Meanwhile, recent concerns about China's slowing economy and potential recessions in the US and Europe have put pressure on oil markets.

- CNY: The offshore yuan traded around 7.15 per dollar, hovering near its weakest level in six months, as disappointing Chinese economic data continued to dampen investor sentiment. China's exports fell more than expected in May, the latest data showed, reflecting a challenging recovery in the country as external demand slows. That, along with weak data from other parts of the economy, has reinforced speculation that the People's Bank of China may cut interest rates again to boost the world's second-largest economy. The lack of direct intervention by the People's Bank of China to support the yuan has also weighed on the currency, although some major state-owned banks have recently sold dollars in the spot market to prevent further falls. Chinese authorities have also reportedly asked major state-owned banks to lower interest rates on dollar deposits, further boosting the currency.

- GAS: U.S. gasoline futures rose to nearly $2.6 a gallon, the highest level in more than a week, as demand improved and domestic inventories fell more than expected. According to new data from the Energy Information Administration (EIA), natural gas demand increased from 9.098 million b/d to 9.218 million b/d last week. Meanwhile, total domestic gasoline inventories rose 2.745 million barrels to 218.815 million barrels, more than market expectations for an increase of 88 thousand. Gasoline prices, however, remain well below the record high of $4 seen in June 2022. The US government forecast a slight increase in gasoline consumption from last year to 9.09 million barrels per day between June and August, but still below levels before the pandemic by more than 6%.Additionally, refiners that have been profitable in recent years may consider cutting production if demand does not support their margins.

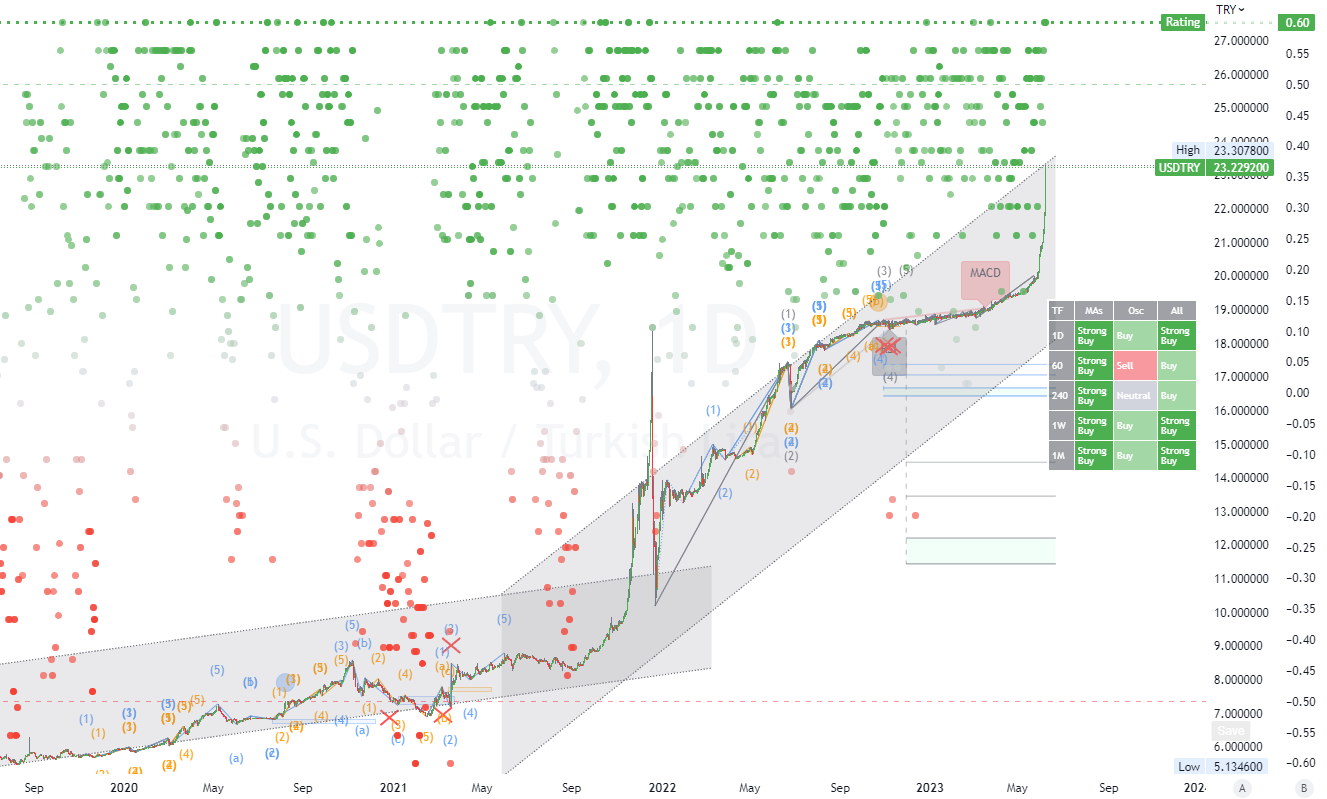

CHART OF THE DAY:

The Turkish lira fell more than 6% to a new record low of 23 per dollar on June 7, marking the largest daily decline since 2021 and bringing the total depreciation since the second round election on May 28 to more than 16%. There were reports that state lenders had ceased selling dollars to protect the lira, an indication of a change in the country's market interventions to curb demand for foreign currency, which has lately pushed Turkey's net foreign exchange reserves into negative territory for the first time since 2022 d. Following the appointment of Mehmet Simsek, a former deputy prime minister renowned for his pro-market policies, as the new finance minister, investors are betting more and more on a change to a more conventional economic approach. Additionally, traders await the selection of a new central bank governor.

Long-term Channels Trading Strategy for: (USDTRY).Time frame (D1). The primary resistance is around (N/A). The primary support is around (20.00). Therefore, the next most probable price movement is a (up/consolidation) trend. (*see all other details on the chart).

Start trading in four simple steps

1. Register

Open your live trading account

2. Verify

Upload your documents to verify your account

3. Fund

Deposit funds directly into your account

4. Trade

Start trading and choose from 130+ instruments

Demo account

The Blue Suisse Trading Account with virtual funds in a risk-free environment

Demo accountLive account

The Blue Suisse Trading Account in our transparent live model environment

Open an Account- Trading Account types Trading conditions Trading hours Transparency Market Information

- Products Currencies Commodities Indices Stocks

- Tools MetaTrader 4 / 5 Mobile CRM, MAM and DSP

- Education Currency Trading for Beginners How to improve your trading CFD Trading

- Partnerships Asset- and Moneymanager Tied agent White labels FIX API

- Company About us Regulatory Our philosophy Careers FAQs Contact us