Growing sense that mega cap stocks are overbought on a short term basis and are due for a pullback; Russian Budget Deficit Remains at Record High; Global Supply Chain Pressure Index Hits Record Low

GLOBAL CAPITAL MARKETS OVERVIEW, ANALYSIS & FORECASTS:

Author: Dr. Alexander APOSTOLOV (researcher at Economic Research Institute at BAS)

Tuesday was a positive day for European stocks, with the Stoxx 600 gaining 0.5% and Germany's DAX gaining 0.2%. Protective healthcare equities increased by 1.2%, while European mining and lending stocks rose by approximately 1% each. In contrast, lower oil prices exerted downward pressure on oil and gas producers. Residents of the euro zone are more optimistic about inflation, according to a survey by the European Central Bank. In April, inflation expectations for the next 12 months decreased from 5% to 4.1%. In addition, Klaas Knot stated that the ECB's measures are beginning to bear fruit, despite the persistence of core inflation. The FTSE MIB index recovered from early losses to close 0.7% higher at 27,040 on Tuesday, outperforming other European equity benchmarks as Milan's well-capitalized banking sector surged. Banca Monte Paschi Siena led the sector with a 5% increase as fresh rumors circulated that the lender could merge with BPER Banca to establish a third powerhouse in the Italian financial system. In the meantime, utilities recouped yesterday's losses as TTF natural gas prices plummeted since Monday. Tuesday's close for the CAC 40 was slightly above flat at 7,209. Traders remained cautious in the face of indications of slowing global growth and uncertainty regarding the future path of interest rates. Recent comments from ECB officials, including President Lagarde, indicate that the ECB is inclined to stick to its policy of raising borrowing costs, despite expectations that the Federal Reserve will cease raising rates later this month. Publicis Group (+3.5%) was the best performer among individual equities, followed by Eurofins Scientifique (+2.5%) and Worldline (+2.3%); while Orange (-1.1%) and TotalEnergies (-0.9%) were the worst performers. The IBEX 35 erased earlier losses to close marginally higher at 9,310 on Tuesday, mirroring the cautious stance of its European counterparts as investors digested a plethora of economic data and awaited additional insights into central bank paths. Although the Federal Reserve is anticipated to end its tightening campaign by the end of the month, the ECB appears resolute in its pursuit of additional rate increases. The principal champion of the day was Grifols, which gained 1.59%. In the real estate sector, Inmobiliaria (+1.11%) and Meliá Hotels (+1.02%) gained significantly after the latter announced its international expansion in Asia. However, at 2.04%, Telefonica proved to be the largest burden. In terms of the economy, industrial production in Spain declined unexpectedly in April.

As investors remained cautious and assessed the impact of conflicting economic data on the Fed's plans for next week, the Dow remained near the flatline on Tuesday. Meanwhile, the S&P 500 rallied to near a nine-month high of 4,283, and the Nasdaq gained 0.3%. Regional institutions such as BankUnited (10.7%), Independent Bank (9.5%), PacWest (8%), Zions Bancorporation (7.5%), Comerica Inc. (7.5%), Western Alliance (7.3%), and KeyCorp (6.7%) performed the best. Apple shares, on the other hand, fell nearly 1% after declining 0.8% on Monday due to concerns that the company's new mixed reality headset is overpriced.

The Canada S&P/TSX Composite index hovered around the flat line at 19,930 on Tuesday, extending losses from the previous session, as gains in technology and banks negated the majority of gains ahead of tomorrow's interest rate decision by the Bank of Canada. Commodity-supported losses. As previously indicated, it is widely anticipated that the central bank will maintain the status quo with interest rates, although traders will be on the lookout for indications of a resumption of tightening due to rising inflation risks. In contrast, the Ivey Purchasing Managers Index for May was substantially below market expectations, coming in at 53.5 and bolstering the dovish outlook. Energy stocks led declines, as crude oil prices surrendered gains from Saudi Arabia's production cutbacks, with Suncor Energy falling more than 1 percent. On the other hand, Shopify's stock rose roughly 5 percent, contributing to gains in technology stocks.

Under pressure from energy producers and metallurgists, the ruble-based MOEX Russia index fell significantly during early trade on Tuesday, but closed 0.5% lower at 2,681. Oil companies extended losses as crude prices pared gains from Saudi Arabia's voluntary production cuts, while yesterday's Russian government energy revenue data underscored the sector's weaker sales. Energy revenue in May was 570 billion rubles, more than a third lower than the same month last year and 44 billion rubles below the finance ministry's projection, adding to the government's fiscal worries. Steel producers, including Severstal and NLMK, also closed lower, with losses of 1.4% and 0.9%, respectively.

The Hong Kong stock market closed Tuesday at 19,099.28, down 9.22 points, or less than 0.1%, as investors digested lackluster U.S. economic data ahead of next week's Federal Reserve meeting. In addition, there was increased caution in advance of China's May trade data on Wednesday and inflation figures on Friday. In May, Hong Kong's private sector grew at its slowest rate in five months due to a slowdown in new orders and increasing cost burdens. According to Morgan Stanley, China's consumption recovery has entered a second phase, which will be more endogenous and supported by broader employment growth. As Beijing prepared a series of new measures to assist the ailing sector, consumer, financial, and technology equities closed lower, while real estate rose nearly 2 percent. Teck Industries was followed by Haidilao International (-3.3%), China Resources Power (-3%), Tencent Holdings (-2.1%), and OOCL (-1.7%).

The Shanghai Composite Index increased by 0.2% to close at approximately 3,240 points, while Shenzhen Stock Exchange constituent equities decreased by 0.4% to 10,900 points. As China's economic and policy outlook remains extremely uncertain, mainland stock markets struggle to find direction. As the post-pandemic recovery persisted, the services sector accelerated in growth in May, according to data released on Monday. Nonetheless, weaker-than-anticipated economic data in other regions suggested a difficult recovery in China, dampening investor sentiment. Hongbo (5.1%), People.cn (7.7%), China Publishing (10%), Kweichow Moutai (0.9%), and Wuliangye Yibin (1.6%) led the way in Tuesday's gains. Meanwhile, the majority of high-growth technology firms declined, with 360 Security Technology (-2.8%), HKUST Xunfei (-2.8%), and Kunlun Technology (-1.4%) declining.

The Nikkei 225 rose 0.2% to close above 32,250 on Tuesday, lingering at its highest level in over 30 years, as a weaker yen improved corporate prospects for Japan's export-heavy industries and made local assets more appealing to foreign investors. In addition to enthusiasm for semiconductors, artificial intelligence, and related technologies, Japanese equities outperformed their global counterparts in May on the strength of investor interest in these sectors. Tuesday saw significant gains for Socionext (1.2%), Tokyo Electron (0.5%), Fast Retailing (1.6%), Mitsubishi Heavy Industries (2.8%), and Mitsui & Co (1.6%). In the meantime, Advantest (-2,2%), Mitsubishi UFJ (-1,4%), and Rakuten Group (-3%) all experienced declines.

Ahead of the Reserve Bank of India's policy decision this week, the India BSE Sensex closed unchanged at 62,793 on Tuesday, maintaining gains from the previous session, as automakers and banks offset tech gains. plate deterioration. Maruti Suzuki and Tata Motors both increased by nearly 1.5 percent in May, following the release of strong sales figures. Axis Bank was up 1.6%, Bajaj Finserv and Indus Ind Bank were up about 1%, and Indus Ind Bank was up about 1% as well. Tech Mahindra, Infosys, TCS, HCL Technologies, and Wipro fell between 2.6% and 1.2% due to fears of a global economic downturn.

REVIEWING THE LAST ECONOMIC DATA:

Reviewing the latest economic news, the most critical data is:

- US: The US IBD/TIPP Economic Optimism Index edged up to 41.7 in June 2023 from 41.6 in May, but remained well below the benchmark of 50, indicating optimism and a market forecast of 45.2. The six-month outlook for Americans fell 0.3 percent to 34.5, the lowest reading since November. 51 percent of respondents see the economy in recession, the lowest level since May 2022, but only 25% see it improving. Elsewhere, support for federal economic policy plunged 3.5 percent to 38.6, the lowest level since last August's eight-year low, likely due to a debt-ceiling agreement, which included an The moratorium on most student loan payments ends later this summer. Meanwhile, a sub-index measuring personal finances rose 3.6% to 51.9, though "people are still a long way from feeling comfortable with the economy," said Ed Carson, IBD's news editor. Eighty-nine percent said they were concerned about inflation, and only 22 percent thought wages could keep up.

- US: U.S. stocks were flat on Tuesday, as investors assessed the potential impact of mixed economic data on the Federal Reserve's plans for next week. Some 75% of traders expect the central bank to pause its tightening cycle this month, while the probability of another 25 basis point hike in July is closer to 52%. On the corporate front, Apple shares fell nearly 1%, having fallen 0.8% on Monday, amid concerns that the price of its new mixed reality headset is too high. Meanwhile, shares of Coinbase fell about 20% after the SEC sued the cryptocurrency exchange. Also, oil stocks, including ExxonMobil and Chevron, fell about 1% as oil prices fell.

- US: The Logistics Managers Index hit a record low for the third straight month in May 2023 at 47.3, compared with 50.9 in April. The data also pointed to the first contraction in the logistics industry in almost seven years, mainly due to continued weakness in the freight market. The transport utilization indicator (-9.5 to 45.5) indicates a contraction in transport and indicates that shippers are using less available space. Additionally, transport prices (-8.9 to 27.9) saw their largest contraction on record. Meanwhile, airlines have little hope of relief in the form of restocking. As a result of inventories at upstream manufacturers and wholesalers, inventory levels decreased for the first time since February 2020 (-1.5 to 49.5), while downstream retail inventories continued to increase. Storage prices have risen since at least June 202 (-7 to 62.8) and may continue to fall as more long-term contracts signed in 2020 and 2021 continue to disappear from the books.

- CA: In May 2023, Canada's Ivy Purchasing Managers' Index further fell to 53.5 from 56.8 in the previous month, far below the market forecast of 57.2. The latest data showed that growth in Canadian economic activity slowed for a second straight month in May as the pace of job creation slowed (56.2 to 55.8 in April) and inventories rose (49 to 48.6). Meanwhile, supplier delivery times were longer (52.1 to 51.2), and inflation accelerated (60.3 to 59).

- CA: The total value of building permits in Canada fell 18.8% from the previous month to $9.6 billion in April 2023, after rising 12.3% in the previous month and well below the market forecast of 5%. That was the lowest level since December 2020, with the non-residential sector plunging 34.6% to $3.4 billion after hitting an all-time high of $5.2 billion in March, with all components down: industrials (-49.6%) , commercial (-40.2%), and institutional (-1.6%). In addition, construction intentions in the residential sector also fell (-6.1% to $6.1 billion), largely due to a decline in Ontario (-10.5% or $296.4 million).

- EU: Eurozone retail sales were unchanged in April 2023 after a revised 0.4% decline in March, below market expectations for a 0.2% growth. With a notable 2.7% increase in online trade, non-food trade increased by 0.5%. However, sales of food, beverages, and tobacco (-0.5%) and trade in fuels (-2.3%) were reported to have declined. Compared with the annual figure, retail sales fell 2.6%, marking the seventh straight month of contraction.

- EU: The HCOB Eurozone Construction PMI fell to 44.6 in May 2023 from 45.2 the previous month, indicating the largest monthly decline in overall construction activity so far in 2023. The real estate sector fell the most, while commercial construction slumped at the fastest pace in five months. Civil engineering was the only sub-sector where contraction slowed, although the decline was still substantial. New orders from construction firms in the euro zone fell sharply—the biggest drop since December—largely due to heightened economic uncertainty. In addition, layoffs accelerated, input purchases fell for the twelfth consecutive month, and average supplier performance improved for the first time since August 2012. On the pricing front, input cost inflation moderated to its highest level in three years.

- UK: In May 2023, the S&P Global/CIPS UK Construction Purchasing Managers Index rose to 51.6, higher than May's data and market expectations of 51.1. Even though it was only a slight increase, the most recent purchasing managers' index revealed the strongest uptick in overall construction activity since February, driven by faster growth in commercial construction and civil engineering activity. Total new business rose by the most since April 2022, despite weakness in the homebuilding sector and concerns over the impact of rising interest rates. Also, employment increased for the fourth straight month, while average lead times for construction products and materials shrank by the most since August 2009, as logistical bottlenecks decreased and the balance between supply and demand improved. On the price front, purchase price inflation was the lowest in two and a half years. Finally, business confidence fell to a four-month low amid concerns about the outlook for the UK economy.

- TW: Taiwan's annual inflation rate fell to 2.02% in May 2023 after stabilizing at 2.35% in the previous two months, below market expectations of 2.29%. That was the lowest level since July 2021, as prices for food (2.96% vs. April's 4.20%), housing (2.14% vs. 2.33%), and education and entertainment (3.01% vs. 3.29%) slowed. In addition, the cost of clothing (-0.64% vs. -0.61%) and transportation communications (-0.11% vs. -0.02%) continued to decline. On a seasonally adjusted basis, consumer prices fell 0.11% on a monthly basis, the first decline since August 2022.

- IT: The HCOB Italian Construction PMI fell to 47.9 in May 2023 from 49 in the previous month, marking the sector's sixth consecutive month of decline. The number of new contracts fell at the fastest pace since February, widening its impact on the sector's performance, with firms citing increased economic uncertainty and the headwinds of flooding across the country. As a result, builders have further cut back on purchases. At the sectoral level, commercial and housing construction both accelerated contraction, while civil engineering extended a persistent negative trend but limited its decline. Still, the company chose to add staff during this period. On the price front, lower demand for input procurement and improved supply chains contributed to the easing of inflation. Looking ahead, businesses remain optimistic about securing bids through the government's recovery plan.

- GE: The HCOB German Construction Purchasing Managers' Index rose to 43.9 in May 2023 from 42 in April, but indicated the 14th straight month of decline in construction. Housing activity remained the biggest drag, with businesses in the sector having been in austerity mode, cutting workforce numbers and reducing purchases of construction materials and products. On the supply side, supplier lead times hit a record high, and construction input costs fell for the first time in nearly 14 years. Meanwhile, conditions are expected to remain difficult over the next 12 months against a backdrop of rising interest rates and customer uncertainty.

- GE: Factory Orders in Germany unexpectedly fell by 0.4% in April 2023, missing market expectations for a 3.0% rise and following a revised 10.9% drop in March. It was the second straight month of decline in industrial orders, dragged down by a 34.0% drop in demand for the manufacture of miscellaneous vehicles, which include ships, rail vehicles, aircraft, spacecraft, and military vehicles. Excluding large orders, it rose 1.4% in April. Meanwhile, orders for motor vehicles and auto parts jumped 2.4%. Capital goods orders fell 1.7%, while consumer goods orders fell 2.5%. In contrast, demand for intermediate goods rose 2.3 percent. While domestic orders increased 1.6%, foreign orders fell 1.8%, driven primarily by a 2.7% decline in orders from the euro zone.

- AU: Final figures showed that the total number of dwellings approved in Australia in April 2023 fell by a seasonally adjusted 8.1% month-on-month to 11,594 units in April 2023, up from a revised 1.0% in March. Private sector housing fell 3.8% to 7,939 in April, while private sector housing excluding housing fell 16.5% to 3,469. Geographically, total dwelling approvals fell in Queensland (-22.8%), Victoria (-18.6%) and Western Australia (-5.8%). Meanwhile, the total number of dwellings rose in South Australia (19.8 per cent), New South Wales (12.5 per cent) and Tasmania (3.5 per cent).

LOOKING AHEAD:

Today, investors should watch out for the following important data:

- CAD: Labor Productivity q/q, Trade Balance, BOC Rate Statement, and Overnight Rate.

- CHF: Unemployment Rate, and Foreign Currency Reserves.

- CNY: Trade Balance, and USD-Denominated Trade Balance.

- AUD: RBA Gov Lowe Speaks, RBA Deputy Gov Bullock Speaks, and GDP q/q.

- USD: Trade Balance, Crude Oil Inventories, and Consumer Credit m/m.

- JPY: Leading Indicators.

- EUR: French Trade Balance, Italian Retail Sales m/m, and German Industrial Production m/m.

- GBP: Halifax HPI m/m.

KEY EQUITY & BOND MARKET DRIVERS:

Кey factors in the stock and bond market are currently:

- US: U.S. futures were little changed on Tuesday, as investors assessed the potential impact of mixed economic data on the Federal Reserve's plans for next week. Some 75% of traders expect the central bank to pause its tightening cycle this month, while the chances of another quarter-point hike in July are closer to 54%. On the corporate front, Apple shares were slightly lower in premarket trading after falling 0.8% in the previous session on concerns that the price of its new mixed reality headset was too high. Elsewhere, banking stocks fell, with Goldman Sachs, Bank of America and Morgan Stanley all down more than 0.5% after news that Bank of America could face a capital increase under upcoming regulations. Oil stocks including Exxon Mobil and Chevron also fell about 1% as they tracked the decline in oil prices.

- AU: Australian 10-year government bond yields surged above 3.8%, the highest since March 3. The Reserve Bank of Australia unexpectedly raised interest rates by 25 basis points to the highest level in 11 years and said further monetary tightening may be needed to bring inflation back into its target range. Policymakers have expressed concern about persistently high inflation and aim to prevent rising price expectations from becoming entrenched in the economy. The RBA's current tightening cycle is the most aggressive in its modern history, with an impressive 400 basis points of interest rate hikes since May 2022. Inflation is only expected to return to the upper end of the Reserve Bank of Australia's 2-3% target range by mid-2025.

- AU: The Reserve Bank of Australia unexpectedly raised the cash rate by 25 basis points to 4.1% in June after raising rates by the same amount in May, while leaving the door open for further tightening as inflation Persistently high, while wage growth accelerated. Tuesday's decision raised rates by a total of 400 basis points since May 2022, pushing borrowing costs to their highest level since April 2012 and breaking the market's consensus pause. Policymakers see increased upside risks to Australia's inflation outlook, largely due to higher service prices. The board added that it was still seeking to keep the economy on an even keel as inflation returned to its 2% to 3% target, but the path to a soft landing remained narrow. The committee said it remained firmly determined to bring inflation back to target and would take the necessary steps to achieve this. The central bank also raised the interest rate on foreign exchange settlement balances by 25 basis points to 4.0%.

- JP": In April 2023, Japanese household spending fell by 4.4% in real terms year-on-year, compared with a consensus estimate of a 2.3% decline in Japanese household spending and a 1.9% decline in the previous month. It was the third contraction so far this year and the biggest drop since June 2021 amid intense cost pressures. Housing (-15.3% vs -5.5%), furniture and appliances (-6.9% vs -4.2%), education (-19.5% vs -16.7%) and furniture and appliances (-6.6% vs - 4.20%), the decline was even greater. Elsewhere, spending on apparel and footwear fell 9.5 percent after rising 1.5 percent previously. Meanwhile, healthcare (2.5% vs. 4.7%), transportation and communications (2.6% vs. 3.0%), fuel, lighting and water (1.6% vs. 6.7%), and culture and entertainment (4.6% vs. 10.4%) Spending growth slowed.

LEADING MARKET SECTORS:

- Strong sectors: Financials, Materials, Communication Services.

- Weak sectors: Health Care, Consumer Staples, Information Technology.

TOP CURRENCY & COMMODITIES MARKET DRIVERS:

Кey factors in the currency and commodities market are currently:

- CAD: The Canadian dollar rose to C$1.34 against the U.S. dollar in early June, overcoming the DXY's strength to reach its highest in almost a month, as investors factored in hawkish signals at the upcoming Bank of Canada meeting. While the central bank is widely expected to hold interest rates steady at 4.5%, red-hot inflation and strong growth data have fueled bets the central bank may eventually be forced to extend its tightening cycle. Consumer prices rose an annualized 4.4% in April, well above the market forecast of 4.1%, unexpectedly accelerating from 4.3% in the previous month. In contrast, the Bank of England forecasts that inflation will fall to 3% by mid-year.

- USD: The U.S. dollar index edged up above 104 on Tuesday, near its highest level since mid-March, as traders tried to assess the resilience of the U.S. economy and the Federal Reserve's next move. Factory orders rose 0.4% in April, half the consensus forecast, and the ISM Services PMI fell sharply to its weakest level in five months in May. Last week, the jobs report painted a mixed picture, with the economy adding 339,000 jobs in May, while the unemployment rate rose 0.3 percentage points to 3.7% and growth in hourly wages slowed. Some 75% of traders expect the Fed to pause its tightening cycle this month, but the chance of another 25 basis point hike in July is closer to 52%. Despite the overall strength, the greenback weakened against the Australian dollar after the Reserve Bank of Australia unexpectedly raised borrowing costs by 25 basis points.

- OIL: Brent futures traded near $76 a barrel on Tuesday, halting a 3-day rally as investors eyed threats to supply and demand. Saudi Arabia, the world's top exporter, said at the weekend it would cut output by 1 million barrels per day (bpd) to 9 million bpd in July, the biggest cut in years, to boost weak oil prices. Oil prices have recently come under pressure amid heightened concerns about China's slowing economy and potential recessions in the US and Europe. Still, the World Bank raised its outlook for global growth in 2023 as the US, China and other major economies proved more resilient than forecast.

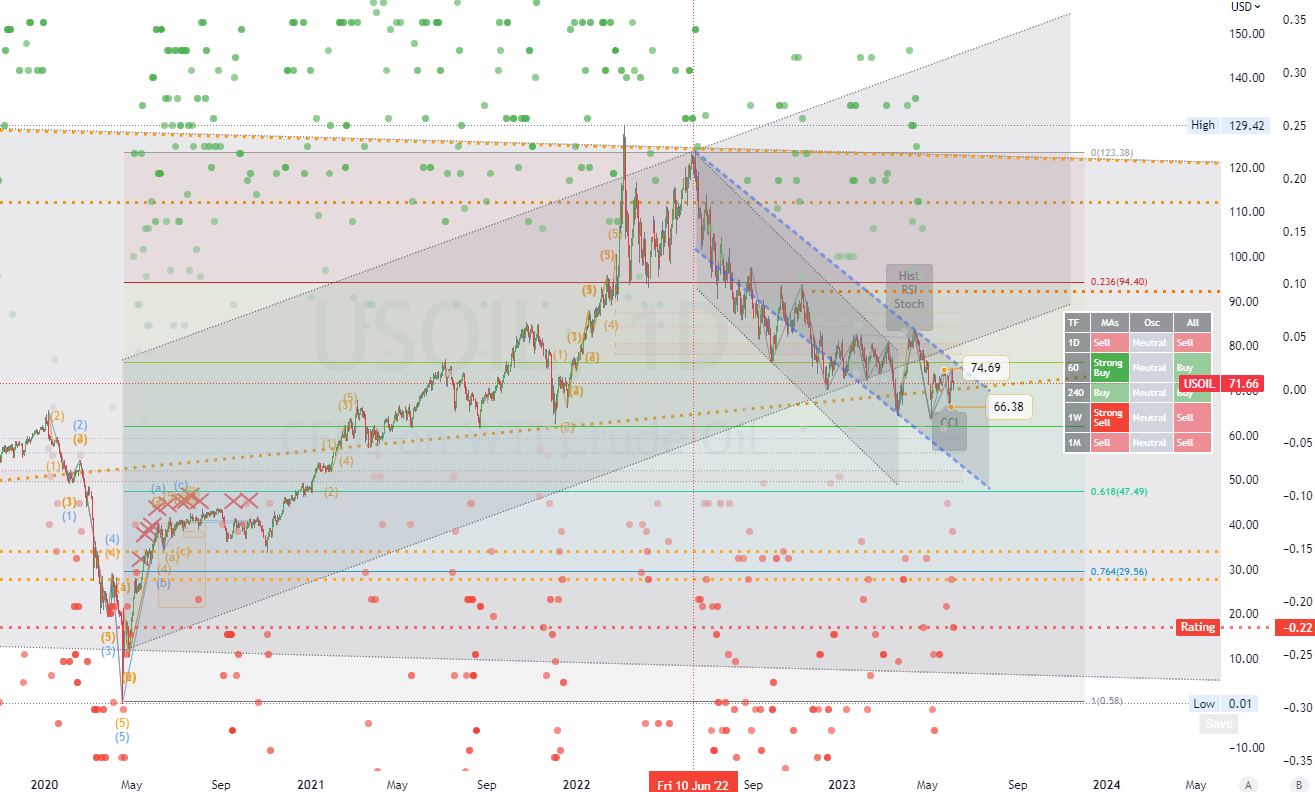

CHART OF THE DAY:

On Tuesday, WTI crude oil futures settled near $72 per barrel as investors closely monitored supply and demand factors. Saudi Arabia, the world's leading exporter, announced over the weekend its intention to reduce production by 1 million barrels per day to 9 million barrels per day in July, the largest reduction in years, in an effort to prop up falling oil prices. However, recent concerns about China's slowing economy and prospective US and European recessions are exerting pressure on oil prices. The resilience shown by the United States, China, and other main economies led the World Bank to upgrade its global growth forecast for 2023.

Long-term Channels Trading Strategy for: (WTI crude oil).Time frame (D1). The primary resistance is around (74.69). The primary support is around (66.38). Therefore, the next most probable price movement is a (consolidation/down) trend. (*see all other details on the chart).

Start trading in four simple steps

1. Register

Open your live trading account

2. Verify

Upload your documents to verify your account

3. Fund

Deposit funds directly into your account

4. Trade

Start trading and choose from 130+ instruments

Demo account

The Blue Suisse Trading Account with virtual funds in a risk-free environment

Demo accountLive account

The Blue Suisse Trading Account in our transparent live model environment

Open an Account- Trading Account types Trading conditions Trading hours Transparency Market Information

- Products Currencies Commodities Indices Stocks

- Tools MetaTrader 4 / 5 Mobile CRM, MAM and DSP

- Education Currency Trading for Beginners How to improve your trading CFD Trading

- Partnerships Asset- and Moneymanager Tied agent White labels FIX API

- Company About us Regulatory Our philosophy Careers FAQs Contact us