Rising oil prices after Saudi Arabia said it will voluntarily cut its own production by one million barrels per day; US Stocks Slip; Gold Prices Edge Up after ISM Services Data

GLOBAL CAPITAL MARKETS OVERVIEW, ANALYSIS & FORECASTS:

Author: Dr. Alexander APOSTOLOV (researcher at Economic Research Institute at BAS)

The Dow fell more than 150 points on Monday as investors digested fresh economic data and the outlook for monetary policy. Factory orders rose 0.4% in April, half the consensus forecast, and the ISM Services PMI fell sharply to its lowest level in five months in May. Cyclical stocks sensitive to economic performance weighed on the Dow, with Caterpillar, Boeing, and 3M among the worst performers. In the meantime, helped along by technology stocks, the S&P 500 reached a nine-month high and the Nasdaq reached a 14-month high.had a 14-month high. Apple shares rose about 2 percent to hit an intraday all-time high of $184.8 as the Worldwide Developers Conference kicked off today, with Apple set to unveil a "mixed reality" headset. Also, Netflix, Alphabet, Oracle, Amazon, and Microsoft are slowly rising.

The Canada S&P/TSX Composite was flat at 20,035 on Monday, extending gains from the previous week, as investors assessed the outlook for Bank of Canada monetary policy and commodity prices, which have had an impact on the performance of Toronto's largest companies. had a major impact. Oil companies led the gains, tracking gains in crude prices after Saudi Arabia announced in July that it would cut output by 1 million bpd. Canadian Natural Resources and Suncor Energy both rose more than 0.6%. On the other hand, gold prices fell, putting pressure on Canadian heavyweight miners. Investors await the Bank of Canada's interest rate decision this week for a potential signal of a policy shift this year.

European shares closed lower on Monday, with Germany's DAX 40 and the pan-European STOXX 600 both down 0.5 percent, after comments from ECB President Christine Lagarde suggested the central bank was inclined to maintain its current policy trajectory. Lagarde acknowledged that there were "signs of moderation" in core inflation, but stressed that it was too early to determine whether price growth had peaked. Earlier in the session, the release of the latest PMI data highlighted a slowdown in the euro zone's private sector economy, while higher crude prices provided support for energy companies after Saudi Arabia pledged to implement additional production cuts starting in July. In terms of notable corporate developments, Goldman Sachs bought Norwegian aquaculture services group Froy for $600 million, while Novo Nordisk began discussions to buy a controlling stake in French medical device designer Biocorp.The FTSE MIB extended early losses to close 0.8% lower at 26,860 on Monday, retreating from the previous week, as higher commodity prices highlighted upside risks to inflation and raised concerns about a rate hike by the European Central Bank. Crude oil prices rose after Saudi Arabia announced another voluntary production cut, while natural gas prices surged 20% on fresh supply pressure. The developments reinforced ECB President Christine Lagarde's warning that inflation may not have peaked yet, adding to the bank's hawkish rhetoric. Utilities posted sharp losses as wholesale prices rose, with Hera slipping 3 percent. UniCredit fell 2.3 percent as concerns over rising borrowing costs and increased domestic bond supply weighed on BTP prices and Italian heavyweights with the launch of new Italian bonds. The CAC 40 index fell about 1% to close at 7,201 on Monday, as traders weighed hawkish comments from current ECB President Christine Lagarde against signs of slowing economic activity in the euro zone. On the corporate front, a number of businesses reported losses, including Pernod Ricard (-2.5%), Essilor Luxottica (-2.4%), and Teleperformance (-2.2%). In addition, LVMH (-2%), Hermès (-2%). On the other hand, Airbus (+0.7%) gained the most. The IBEX 35 closed marginally lower at 9,289 on Monday, snapping two sessions of gains and trailing its European peers as investors digested the latest PMIs, hawkish remarks from the ECB, and Saudi Arabia's decision to cut more oil production. Banks pared previous gains, with Banco Sabadell the main antagonist, down 1.87%. Also, Aena and Sacyr were down over 1%. Conversely, Laboratorios Farma and Merlin properties supported the index, rising 2.82% and 1.11%, respectively.

The FTSE 100 fell below 7,600 on Monday, with mining shares falling as metals prices fell and gains in oil prices faded. Base and precious metals miners fell 0.5 percent and 3.0 percent, respectively. The telecom sector, on the other hand, rose 2.0 percent after a report that Amazon was negotiating a cost-effective wireless service for its Prime members. In terms of individual stocks, ASOS rose more than 7% after reports that Turkish online retailer Trendyol made a £1 billion bid for ASOS.

India's BSE Sensex rose 240 points to close at 62,790 on Monday, extending gains from the previous session and approaching a six-month high hit in the previous week, tracking positive momentum in Asian equities as markets continued to assess the outlook for monetary policy from major central banks . Despite rising bond yields, stocks reacted positively to a mixed U.S. jobs report after the close on Friday, as investors remained focused on signals from Fed officials to skip raising interest rates this month. Domestically, the Reserve Bank of India is expected to keep rates on hold for the second time in a row at its upcoming meeting later this week as Indian inflation has slowed from last year's highs. Automakers led gains in Mumbai, with Mahindra and Mahindra up 3.3 percent each, while Maruti Suzuki and Tata Motors rose nearly 1 percent each.

The ruble-based MOEX Russia index erased early gains to close 0.9 percent lower at 2,694 on Monday, as banks and miners fell sharply, giving back gains made the previous week. Miners fell, with Polymetal plunging nearly 7% and Polyus down 3%, pressured by a fall in the global benchmark gold price. Financial firms also retreated, with VTB and Sberbank down 2.6 percent and 2 percent, respectively. Meanwhile, oil stocks ended mixed as investors digested the latest news for the sector. The Russian government’s oil and gas revenue fell 36% in May from a year earlier as demand from Asian economies that haven’t shied away from direct business with Moscow remained sluggish. The value was 44 billion rubles lower than the finance ministry's forecast, adding to the government's fiscal concerns. On the other hand, companies have found some support from Saudi Arabia's voluntary production cuts. Lukoil fell 3 percent after Friday's dividend divestiture, while Transneft fell 3.2 percent.

On Monday, the Shanghai Composite rose 0.2% to around 3,235, while the Shenzhen Composite fell 0.4% to 10,950 in a mixed trade, as investors reacted to data that showed China's post-epidemic recovery continued. China's service sector growth accelerated in May. Still, investors remained cautious amid a highly uncertain outlook for the world's second-largest economy, with markets divided on whether Chinese authorities would roll out further policy support. Mainland stock markets were mixed on Monday, with heavyweights such as Naura Technology (6.1%), Hongbo (10%), and 360 Security Technology (4%) gaining notably. Meanwhile, Modern Amperex (-4.1%), Sungrow (-2.8%), and Tianqi Lithium (-1.6%) posted losses.

In early trade at the start of the week, the Hang Seng rose 80 points, or 0.42%, to 19,030, up from the previous session after U.S. President Joe Biden signed a debt-ceiling bill over the weekend that would keep the country from defaulting. The index followed Wall Street's upbeat run on Friday, supported by gains in big technology stocks and bets that the Federal Reserve will keep interest rates on hold this month. Investors also cheered private survey data showing activity in China's services sector accelerated in May amid strong domestic demand and continued foreign orders. Financial, industrial, and utility sectors led the gains, with Shenzhou International Group (1.7%) and Xinyi Solar Energy Company performing outstandingly in early trading. Trip.com is up 4.5 percent since joining the benchmark index on June 5.

The Nikkei 225 rose 1.6 percent to close above 32,000, while the Topix rose 1.1 percent to close at 2,210. Both benchmarks hit fresh 33-year highs as U.S. President Joe Biden signed the debt ceiling bill into law, averting a potentially catastrophic U.S. government default, boosting sentiment. Japanese stocks have outperformed their global peers since May on strong domestic earnings and a weaker yen, boosted further by enthusiasm for artificial intelligence and related technologies.

The S&P/ASX 200 rose 1.2% to close above 7,200 on Monday, its third straight session of gains, with stocks broadly rising as the signing of the U.S. debt ceiling bill into law boosted risk appetite. Expectations that the Reserve Bank of Australia would pause interest rate hikes at its meeting on Tuesday also boosted investor sentiment. Heavyweight mining stocks led gains in iron ore prices, with gains in BHP Billiton Group (2%), Fortescue Metals (2.8%), and Rio Tinto (2.1%). Oil prices surged after Saudi Arabia pledged to further cut output, as did energy companies, with industry leaders Woodside Energy and Santos Ltd. up 1.9 percent and 2.2 percent, respectively. Major companies in the financial, technology, healthcare, industrial, and consumer sectors also rebounded.

REVIEWING THE LAST ECONOMIC DATA:

Reviewing the latest economic news, the most critical data is:

- US: The ISM Services PMI fell to 50.3 in May 2023 from 51.9 in April, indicating the fifth straight month of expansion in services but the slowest in the current series. The figure was below forecasts for 52.2 as business activity (51.5 vs. 52), new orders (52.9 vs. 56.1), and new export orders (59 vs. 60.9) slowed, while employment contracted (49.2 vs. 50.8). Additionally, supplier lead times accelerated (47.7 vs. 48.6) and capacity increased, which in many ways was a product of weaker demand. Meanwhile, inventories rebounded (58.3 vs. 47.2), and price pressure fell to the lowest level since May 2020 (56.2 vs. 59.6). "A majority of respondents said business conditions are currently stable; however, there are also concerns about a slowing economy," said Anthony Nieves, chairman of the ISM Services Business Survey Committee.

- US: The S&P Global U.S. Services PMI was revised down slightly to 54.9 in May 2023 from a preliminary reading of 55.1, but continued to point to the strongest expansion in the services sector since April 2022, mainly supported by new business. Improved demand conditions in both domestic and export markets were what drove the increase in new orders. At the same time, companies have once again stepped up their hiring activities, and employment has grown steadily. There was enough capacity to handle new business, allowing the company to reduce its backlog for the first time in four months. On the price front, both input price and output cost inflation have declined since April, but are still on the rise. Meanwhile, business confidence returned to its highest level in a year, although it remained below the series average.

- US: U.S. stocks traded near flatline on Monday, pausing after Friday's sharp gains, as investors awaited new economic data, including the ISM services PMI, and digested Saudi Arabia's pledge to cut oil supply. Shares of Chevron and Exxon rose about 1% as oil prices soared. Meanwhile, Apple shares rose 1% as the company's Worldwide Developers Conference kicked off today, with the company set to unveil a "mixed reality" headset. On the other hand, Estée Landa shares fell more than 1% after Oppenheimer downgraded the stock to perform from outperform. Shares of 3M and Salesforce also fell about 1%.

- UK: The S&P Global/CIPS UK Composite Purchasing Managers' Index fell to 54 in May 2023 from a one-year high of 54.9 last month, revised up from an initial estimate of 53.9 but still pointing to a solid pace of growth in the UK private sector. Consistent with trends across Europe, the divergence between services and manufacturing continued as expansion in service providers (55.2 to 55.9 in April) offset declines in goods producers (47.1 to 47.8), underscoring a more initial impact of high interest rates on factory activity. Differences between industries are widespread in terms of total output, new orders, and employment. Meanwhile, aggregate prices rose at the slowest pace since March 2021, largely as lower commodity prices and improving supply chains hit manufacturers.

- UK: The S&P Global/CIPS UK Services PMI was revised up slightly to 55.2 in May 2023 from a preliminary reading of 55.1, close to April's 12-month peak of 55.9. It marked the fourth straight month of expansion in the country's services sector, with strong gains in output and new orders attributed to resilient consumer demand. Higher levels of output in the services sector tend to be associated with higher spending on consumer services, especially travel and leisure and technology services. Export sales also rose sharply, attributable to higher numbers of international tourists and stronger demand for business services from U.S. and European customers. At the same time, the pace of job creation has slowed. On the price front, headline inflation in input prices edged up to a three-month high, largely linked to higher wages for workers. As a result, average prices charged in May continued to rise sharply despite inflation falling to the second-lowest rate since August 2021.

- EU: For May 2023, the HCOB Eurozone Composite PMI was revised down to 52.8 from an initial estimate of 53.3, down from April's 11-month high of 54.1. The latest data marked the first slowdown in growth since economic activity picked up again in early 2023, with output rising at the slowest pace in three months. Service sector activity continued to grow, albeit at a slower pace, while manufacturing production fell at the fastest pace since November as orders deteriorated rapidly. Total new business was virtually stagnant in May, new export sales fell for the 15th straight month, and the pace of job creation, while weaker than in April, was faster than the average for the entire series. Finally, cost pressures cooled further, and business sentiment weakened to a five-month low.

- EU: The HCOB Eurozone Services PMI for May 2023 was revised down to 55.1 from a preliminary reading of 55.9, but continued to point to strong growth in services. This followed April's reading of 56.2. Demand improved further in May, with new business rising for the fifth month in a row and new export sales rising at the fastest pace on record. In addition, job gains continued, with backlogs of work rising for the fourth straight month, pointing to pressure on capacity and yet another sharp rise in prices. Finally, businesses remained optimistic, although confidence was the lowest so far this year.

- TW: In May 2023, Taiwan's foreign exchange reserves rose to US$562.87 billion from US$561.12 billion in the previous month, the largest on record. The increase was mainly attributable to returns on investments in foreign exchange deposits and exchange rate movements of other reserve currencies against the US dollar. In May 2022, foreign exchange reserves will be 548.85 billion US dollars.

- FR: The S&P Global French Services PMI for May 2023 was revised down to 52.5 from a forecast of 52.8, but the latest figures mark the sector's fourth straight month of expansion. New business inflows fell for the first time since January, largely due to weaker domestic sales to foreign customers. Meanwhile, output price inflation climbed to a three-month high and input cost inflation slowed to a 20-month low, but the companies have been aggressive in pricing amid rising output charges since February. In addition, employment levels continued to grow, extending the current rate of job growth to nearly two and a half years. Overall, French service companies are upbeat, mainly due to strong demand.

- FR: In May 2023, the HCOB French Composite Purchasing Managers Index was revised down slightly to 51.2 from an initial estimate of 51.4, down from 52.4 in April. It marked the fourth straight month of expansion in the private sector, albeit the slowest in the current sequence of growth. A slowdown in the services sector, where output growth was weak and new orders decreased (PMI was 52.5 in April versus 54.6 in April), was the primary cause of the weak expansion. Meanwhile, manufacturing activity contracted for the fourth month in a row in May (PMI 45.7 from 45.6 in April). New orders fell again, at the fastest pace since November, as demand in both sectors fell. Meanwhile, employment grew for the 29th straight month. On the price front, input inflation fell to its lowest level in 23 months, but sales prices accelerated. Finally, business confidence fell to a three-month low.

- IT: In May 2023, the HCOB Italian Composite Purchasing Managers' Index fell to 52.5 from 53.4 the previous month, below market expectations and the slowest pace of expansion in four months. Still, it extended the current growth trend to five months, as a strong but slower expansion in services (54 to 57.9 in April) offset a sharp contraction in manufacturing (45.9 to 46.8). The level of new orders and production in Italy's private economy widened the persistent divergence between sector performance, with the impact of ECB rate hikes more pronounced on commodity producers. At the same time, both industries added jobs. On the price side, service providers have experienced significantly higher cost inflation due to increases in energy and worker wages. On the other hand, lower commodity prices and improved supply chains led to the largest drop in factory costs in 14 years. While business confidence fell to a four-month low, the outlook remained positive.

- IT: The HCOB Italian services PMI fell to 54 in May 2023 from 57.6 in April, the highest reading in 20 months, compared to a forecast of 57. Despite the economic slowdown, data continued to point to strong, above-trend growth in the services sector. The improvement in market demand supports new business, while the pressure on production capacity is obvious, and the company continues to add employees at the fastest rate in nearly a year. Cost inflation, on the other hand, remained high as growth in activity and new jobs slowed due to the prices of fuel, energy, and other variable costs. Finally, business confidence remained positive, but was the weakest since January, with some firms expressing concern about the trajectory of monetary policy and its potential to limit economic activity.

- GE: The HCOB German Services PMI for May 2023 was revised down to 57.2 from a preliminary reading of 57.8, but still showed the strongest growth in services since last April. A pickup in demand and an increase in the number of customers drove business activity to rise broadly for the fourth consecutive month. In addition, new export businesses grew at a record pace. At the same time, the level of outstanding business has increased, suggesting that operational capacity is under pressure. Employment continues to rise amid rising labor costs, input prices continue to rise, and elastic demand enables many service firms to pass on higher costs to customers. Finally, companies remained optimistic, but confidence was further weakened by concerns about high inflation, tightening financiaconditions,ns and the general economic outlook.

- GE: Germany's trade surplus widened to 18.4 billion euros in April 2023, compared with a downward revision of 14.9 billion euros in the previous month, beating market expectations of 16 billion euros. This was the largest trade surplus since January 2021, mainly due to higher sales to the EU (4.5%) and a 1.2% increase in exports. In contrast, exports to countries outside the EU fell by 2.4%, with sales to Russia (17.8%) and the UK (5.2%) falling significantly. However, exports to the US and China showed positive growth, rising by 4.7% and 10.1%, respectively. Imports fell 1.7%, with imports falling to the lowest level since January 2022. Purchases from the European Union fell 0.4%, while imports from third countries fell 3%. Among the third countries, imports from Russia (-7.6%) and the United Kingdom (-6.4%) fell, but imports from China (1.9%) and the United States (2.9%) increased.

- SW: The Swedish services PMI fell to 50.2 in May 2023 from 50.6 in the previous month. The services sector experienced growth for the second month in a row, but it slowed from April due to smaller increases in new orders (51.2 compared to April's 54.2) and business volumes (51.4). Delivery times also improved (42.7 versus 40.6), but remained below the 50 mark. Employment, meanwhile, rose to a four-month high of 55.3 (52). On the price front, input costs fell to 57.3 (vs. 57.9), the second month in a row that the index was below its historical average of 58.1. Looking ahead, downside risks to the services sector have increased due to weakening economic signals in the sector and a general decline in housing construction.

- RU: The S&P Global Russia Services PMI fell to a three-month low of 54.3 in May 2023 from 55.9 in the previous period. It was the fourth straight month of expansion for the sector, with new business picking up again and businesses noticing another rise in new export orders. The continued rise in new orders led businesses to expand employment, the second-fastest pace of growth since June 2021. On pricing, input cost inflation slowed to its second lowest since January 2021, while output cost inflation eased as companies struggled to stay competitive and drive new sales. Finally, business sentiment deteriorated to a four-month low, which is only moderate in the historical context of the series. However, market sentiment remained positive amid hopes for a further demand uptick and marketing investment plans.

- RU: The S&P Global Russia Composite PMI fell to a three-month low of 54.4 in May 2023 from 55.1 the previous month. Still, it was the fourth straight month of expansion in private sector activity, with a slower pick-up in services sector output holding back the overall pace of growth. New orders rose steadily as weak demand in the services sector offset a sharp rise in manufacturing orders. Employment, meanwhile, grew at the second fastest rate since June 2021, as backlogs dwindled and greater capacity allowed companies to do their excellent business. However, new export orders returned to contraction territory as demand from foreign customers in manufacturing fell again. On the cost side, price increases have intensified and are generally significant. The pace of growth was the fastest in three months due to higher supplier and wage costs. That said, efforts to boost sales led to modest increases in output expenses in the two monitored industries.

- CN: The Caixin China Composite Services PMI rose to 57.1 in May 2023 from 56.4 in the previous month. Still, it was the fifth straight month of expansion in services sector activity and the second-fastest since November 2020, as the post-COVID-19 recovery continued. New orders rose faster, new export business continued to grow, there were reports of stronger market conditions, customer turnout increased, employment climbed slightly, and order backlogs increased further. On the price front, input cost inflation eased from a one-year high in April, but was generally stable due to higher personnel costs and higher raw material prices. Meanwhile, output cost inflation accelerated to its fastest pace since February 2022 and was above the series average as firms sought to raise fees again. Finally, business sentiment remained upbeat, but optimism fell to its lowest level in five months.

- AU: In the first quarter of 2023, Australian business inventories increased by 1.2% quarter-on-quarter on a seasonally adjusted basis, beating consensus forecasts for a 0.5% increase and following an upward revision of 0.3% in the previous quarter. By industry, business Inventories in Mining (5.0% vs -0.2%), Retail (0.9% vs -1.8%), Wholesale (2.9% vs 1.1%) and Lodging & Services (5.7% vs 1.6%) has grown. In contrast, manufacturing (-0.7% vs. 0.7%) and electricity, gas, water, and waste services (-2.8% vs. 7.2%) saw business inventories rise 4.1% through March, well below the fourth quarter's growth of 7.6%.

- AU: Australian corporate profits rose 0.5% quarter-on-quarter in the first quarter of 2023, missing consensus estimates of 2.0% and slowing sharply from an upward revision of 12.7% in the previous quarter, the strongest growth since the fourth quarter of 2016. Manufacturers (5.0% vs. 10.5% in Q4), utility providers (7.9% vs. 10.2%), builders (2.9% vs. 3.5%), information providers (0.4% vs. 5.6%), other services (profit growth was slower in administrative and support services (11.5 percent versus 23.2 percent), and professional and scientific industries (7.0 percent versus 12.3 percent). Also, miners (-2.2% vs. 15.6%), retail traders (-2.1% vs. 9.7%), wholesale traders (-4.5% vs. 16.5%), and arts and entertainment services (-7.9% vs. 12.8%). In contrast, financial and insurance services (33.4 percent vs. 15.2 percent) and transportation providers (10.1 percent vs. 6.9 percent) posted gains. Corporate profits rose 7.1% through March, well below the 16.0% gain in the fourth quarter.

- AU: The final data showed that in May 2023, the Judo Bank Australian Services PMI came in at 52.1, down from 53.7 in the previous month. The services sector in Australia experienced expansion for the second month in a row, though at a slower rate than in April due to faster new business growth. New business growth accelerated in May, extending a sales expansion that began in April. According to panelists, the most recent improvement was a result of increased tourism activity and new customer wins. Higher demand for Australian services drove the increase in activity, further contributing to the continued expansion of the workforce in the middle of the second quarter. Finally, overall sentiment in Australia's services sector remained positive in May, with business confidence levels improving from April. Still, concerns about inflation, rising interest rates and the economic environment continued to weigh on market sentiment.

- JP: For May 2023, the ANZ Japan Services PMI was revised down to an all-time high of 55.9, compared with a peak of 56.3 in the preliminary data and 55.4 in the previous month. It was also the ninth straight month of growth in the services sector, as customer demand recovered as the impact of COVID-19 continued to wane. Superior business growth was strongest as foreign demand grew at an unprecedented rate, largely due to strength in inbound tourism. As a result, employment grew at the second-fastest pace in the history of the survey, behind only April 2019. On the inflation front, input cost inflation fell to its lowest level in 14 months. Meanwhile, output cost inflation rose at a slower pace for the first time since the start of the year. Finally, while the data softened from April's series peaks, market sentiment remains upbeat amid hopes that the current recovery will continue as the fallout from the pandemic continues to dissipate.

- JP: The au Jibun Bank Japan Composite Purchasing Managers' Index for May 2023 was 54.3, compared to 52.9 in April. The latest data showed private sector activity growing for a fifth straight month, the fastest pace since October 2011 and the second-strongest pace in the survey's history, as the recovery from the outbreak's disruptions gained momentum. The services sector expanded at a record pace for the second straight month, while manufacturing production returned to growth for the first time in 11 months. A series of record upturns in new order inflows have resulted in the worst backlog of work since the June 2022 survey records. Also, job growth was the largest since June 2017. On the price front, input cost inflation fell to its lowest point since October 2021, while output price inflation slowed for the first time since January. Finally, market sentiment is near April's 17-month high.

LOOKING AHEAD:

Today, investors should watch out for the following important data:

- EUR: German Factory Orders m/m, and Retail Sales m/m.

- GBP: BRC Retail Sales Monitor y/y, Construction PMI, and 30-y Bond Auction.

- JPY: Average Cash Earnings y/y, Household Spending y/y, and 30-y Bond Auction.

- NZD: ANZ Commodity Prices m/m, and GDT Price Index.

- AUD: Current Account, Cash Rate, and RBA Rate Statement.

- CAD: Building Permits m/m, and Ivey PMI.

KEY EQUITY & BOND MARKET DRIVERS:

Кey factors in the stock and bond market are currently:

- US: U.S. 10-year Treasury yields reversed earlier gains to trade around 3.7% as recent data raised some concerns about the resilience of the economy. The ISM Services Purchasing Managers' Index showed activity in the services sector slowed more than expected last month, while factory orders rose well below market forecasts. Last week, the jobs report painted a mixed picture, with the economy adding 339,000 jobs in May, while the unemployment rate rose 0.3 percentage points to 3.7% and growth in hourly wages slowed. About 80% of market participants expect the Fed to keep rates steady when it meets next week, but traders now appear divided on the July move, with only about half expecting a 25 basis point rate hike, compared with the 25 basis point hike before the ISM service release. The proportion is 56%. Meanwhile, the Treasury Department will now resume new debt issuance after President Biden signed the new debt bill into law on Saturday, avoiding a U.S. default.

- US: U.S. futures were little changed on Monday, pausing after sharp gains on Friday, as investors awaited new economic data including the ISM services PMI and digested Saudi Arabia's pledge to cut oil supplies. In premarket trading, shares of Chevron and Exxon rose as oil prices surged. Meanwhile, Apple shares are also in the green as the Worldwide Developers Conference kicks off today and Apple will unveil a "mixed reality" headset. Shares of Dollar General, on the other hand, fell nearly 1% in pre-market trading after Morgan Stanley downgraded shares of Dollar General to Equal Weight from Overweight, while Oppenheimer downgraded the stock from Outperform to . Estée Lauder also fell about 1% after the broader market was downgraded to perform well.

- UK: U.K. 10-year gilt yields rose above 4.2 percent, near a seven-month high of 4.384 percent on May 25, as investors expect the Bank of England to raise rates to 4.75 percent on June 22 and close before the end of the year. reached a peak of 5.5%. Bank of England policymaker Catherine Mann echoed persistent inflation concerns, with NatWest forecasting that core inflation in the UK has yet to peak. In addition, Saudi Arabia's sharp production cuts have added to inflation concerns. The latest CPI report showed that UK annual inflation fell to 8.7% in April from 10.1% in March, the first time it has fallen below double digits since last summer.

- IT: Italian 10-year bond yields bounced back above 4%, recovering from a more than two-month low of 3.994% reached on June 1. Saudi Arabia's announcement of deeper production cuts sparked the most recent increase in crude oil prices, raising concerns about persistently high inflation and the potential need for major central banks to tighten monetary policy. The ECB is expected to continue its policy actions, with market forecasts pointing to at least two more rate hikes this month and next. Also, according to the market outlook, interest rates are expected to peak at 3.75%.

- FR: French 10-year OAT yields rebounded above 2.9%, recovering from a recent low of 2.801% reached on June 1. Crude oil prices rose after Saudi Arabia announced deeper production cuts, raising the possibility that major central banks will keep borrowing costs high for an extended period, fueling concerns about inflation. Market expectations suggest the ECB rate will peak at 3.75% later this year. Currently, the market is pricing in at least two more rate hikes in June and July. Notably, rating agency Standard & Poor's maintained France's AA rating and maintained a negative outlook, as there are downside risks to our forecast for the country's public finances at a time when ordinary French government debt has already risen.

- GE: Germany's 10-year government bond yield rebounded to above 2.3% after sharp losses last week, as a rebound in oil prices sparked by Saudi Arabia's announcement of deeper output cuts stoked inflation concerns. The development has raised concerns about persistent global inflation, which could prompt major central banks to keep interest rates higher for an extended period. Market traders now expect the ECB to raise interest rates to a peak of around 3.75% later this year from the current 3.25%. Many investors expect a 25 basis point hike this month and next. European Central Bank President Christine Lagarde recently emphasized that inflation in the euro zone remains high, which points to the need for further tightening of monetary policy.

LEADING MARKET SECTORS:

- Strong sectors: Energy, Utilities, Consumer Discretionary, Health Care.

- Weak sectors: Financials, Industrials, Real Estate, Energy.

TOP CURRENCY & COMMODITIES MARKET DRIVERS:

Кey factors in the currency and commodities market are currently:

- USD: The U.S. dollar index edged lower on Monday around 104 points as investors tried to assess the health of the U.S. economy and the Federal Reserve's next move. Factory orders rose 0.4% in April, half the consensus forecast, and the ISM Services PMI fell sharply to its weakest level in five months in May. Last week, the jobs report painted a mixed picture, with the economy adding 339,000 jobs in May, while the unemployment rate rose 0.3 percentage points to 3.7% and growth in hourly wages slowed. About 80% of market participants expect the Fed to keep rates steady when it meets next week, but traders now appear divided on the July move, with only about half expecting a 25 basis point rate hike, compared with the 25 basis point hike before the ISM service release. The proportion is 56%.

- CAD: The Canadian dollar remained below $1.35, near a two-week high of $1.34 touched last week, as investors cautiously awaited the Bank of Canada's monetary policy meeting on Wednesday. Money markets expect rates to remain unchanged at 4.5%, but the bank could resume raising rates. The latest data showed that consumer prices rose an annualized 4.4% in April, beating expectations for a 4.1% increase and snapping a 10-month streak of slowing inflation amid sharp increases in mortgage costs and rents. Also, over the weekend, Saudi Arabia announced its biggest oil production cut in years, further stoking inflation concerns.

- EUR: The euro traded around $1.07, holding near a two-month low of $1.0633 hit on May 31, as investors weighed easing inflationary pressures in the bloc against hawkish comments from European Central Bank President Christine Lagarde. On the one hand, data showed a sharper-than-expected slowdown in consumer and producer prices, suggesting the ECB could peak interest rates in September, earlier than previously forecast in December. However, Lagarde said that inflation in the euro zone remained high, suggesting further monetary tightening was needed. Deputy Governor Luis de Guindos and Bank of France President François Villeroy de Galhau mentioned that rate hikes are starting to affect inflation and that any future hikes will be minimal.

- CNY: The offshore yuan fell below 7.1 against the dollar, retreating to its weakest level in six months, as a strong U.S. jobs report boosted bets that the Federal Reserve will keep interest rates higher for longer. Markets are now pricing in a 25% chance of another 25 basis point rate hike from the Fed this month, with a potential pause in the tightening cycle still the base case. Domestically, growth in China's services sector accelerated in May as the country's post-epidemic recovery continued, a private survey showed. Still, mixed data on manufacturing and other economic activity suggests China's recovery is not going to be smooth. That reinforced speculation that the People's Bank of China may cut interest rates again to boost the world's second-largest economy. The lack of direct intervention by the People's Bank of China to support the yuan also weighed on the currency, even after some major state-owned banks sold dollars in the spot market to prevent the yuan from falling further.

- JPY: The yen fell below 140 against the dollar, retreating to its weakest level in six months, as a strong U.S. jobs report increased bets that the Federal Reserve will keep interest rates higher for longer. Markets are now pricing in a 25% chance of another 25 basis point rate hike from the Fed this month, with a potential pause in the tightening cycle still the base case. That stands in stark contrast to the Bank of Japan, which has stuck to its ultra-low interest rate policy despite market pressures and persistent inflation. The yen's weakness prompted the country's top currency diplomat to warn that the Japanese government "will closely monitor currency market movements and respond appropriately as needed."

- AUD: The Australian dollar was steady around $0.66, holding on to recent gains as investors braced for the Reserve Bank of Australia's interest rate decision. Australia's monthly inflation gauge showed prices accelerated to a four-month high of 0.9% in May, suggesting persistent inflation could weigh on the central bank. Reserve Bank of Australia Governor Philip Lowe recently pledged to do whatever is necessary to bring inflation back to target, warning that despite a moderation in inflation expectations, risks to inflation remain elevated. Positive service data from China, Australia's largest trading partner, and a rise in commodity prices also supported the Australian dollar.

- GLD: Gold prices rose slightly above $1,950 an ounce on Monday, following a moderate weakening of the U.S. dollar and a slight drop in U.S. Treasury yields after weak U.S. economic data reinforced views that the Fed will end its tightening cycle next week . The ISM Services PMI pointed to sluggish growth in the U.S. services sector in May, while new orders for industrial goods rose less than expected and only because of a rise in defense spending. Still, gold prices remain well below the near-record high of $2,050 reached on May 5, as traders expect interest rates will have to remain elevated for an extended period in the US, Europe, and the UK due to persistent inflationary pressures.

- CRN: Corn futures rebounded to the $6 a bushel mark, sharply above the 18-month low of $5.50 hit on May 19, as poor US growing weather threatened the health of the incoming crop. USDA checks showed 69 percent of U.S. corn was in good to excellent condition at the end of May, the lowest in four years and below market estimates of 71 percent due to dry weather in the U.S. West Corn Belt. Russia also continued to say that the current grain deal to protect Ukrainian exports was unlikely to be renewed, dimming hopes for stable supplies from one of the world's biggest exporters.On the other hand, growing supply from South America, particularly Argentina and Brazil, led the USDA to predict that world corn production could reach a record high next marketing year.

- OIL: Brent crude futures pared gains to around $77 a barrel on Monday, after jumping as much as 3.4% to $78.7 a barrel in the early session, as investors weighed supply cuts against concerns about demand. Saudi Arabia pledged to cut output by another 1 million barrels a day to about 9 million barrels in July, the lowest level in years.Saudi Energy Minister Prince Abdulaziz bin Salman said he would "do whatever it takes to ensure stability in this market" at a high-stakes OPEC+ meeting at the weekend, but other members vowed to maintain existing cuts until the end of 2024. At the same time, Russia did not commit to cutting production further, and the United Arab Emirates was allowed to raise production targets for next year. Brent crude futures fell 10% in May and are down nearly 10% so far this year.

- GAS: US natural gas futures rose more than 6% to over $2.3/MMBtu on stronger demand and reduced supply. More natural gas is used to generate electricity due to lower wind power generation, which reduces the availability of fuel for storage. Meanwhile, US gas production fell slightly in June from the previous month and is likely to fall further after the latest data from Baker Hughes showed a 15-week decline in active US oil rigs. More than a third of gas production in shale regions comes from associated gas, which is extracted at the same time as oil is pumped.Adding further pressure, European gas prices jumped more than 20% on Monday on concerns about global competition for LNG cargoes this summer and several maintenance projects at production facilities.

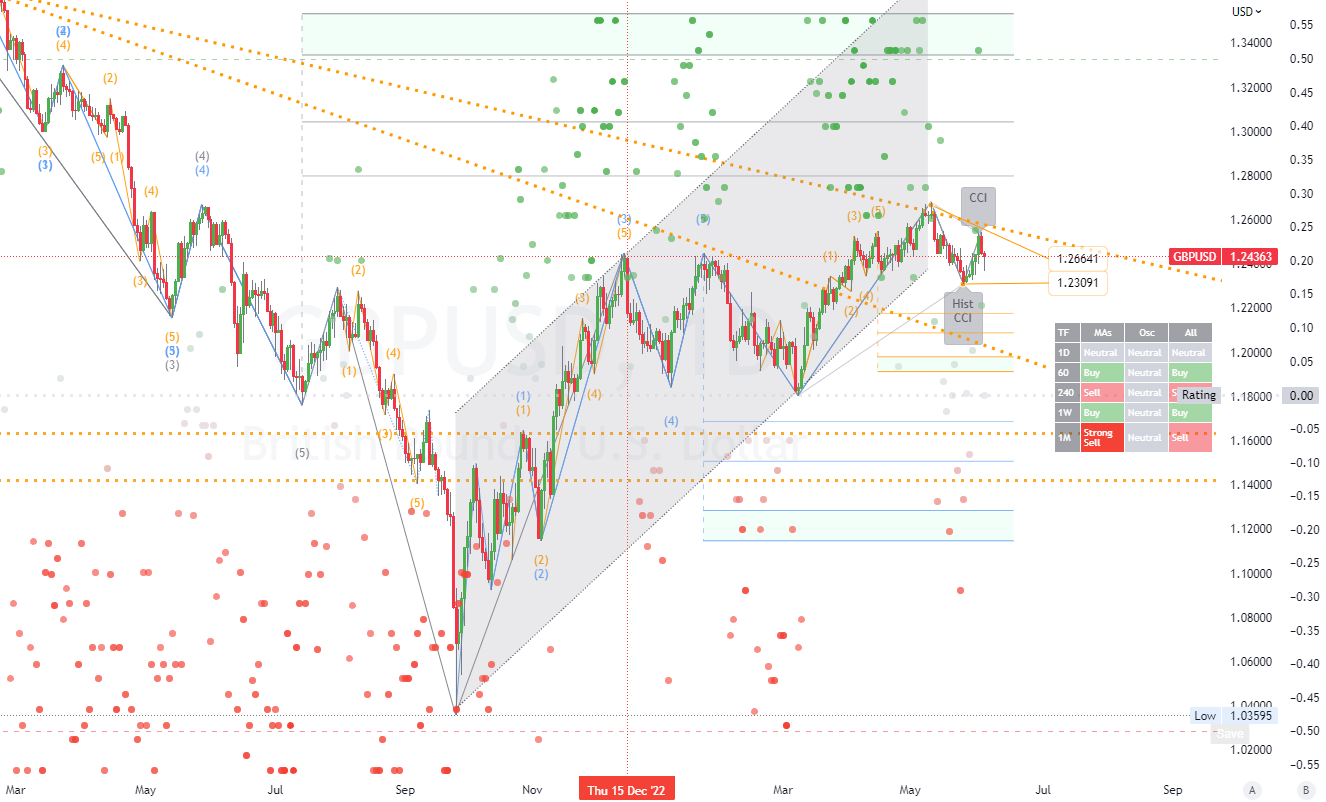

CHART OF THE DAY:

As investors wager that the disparity between U.S. and U.K. interest rates is narrowing, the pound fell below $1.24, approaching a two-month low of $1.2306 set on May 25. The Bank of England is anticipated to increase interest rates to 4.75 percent on June 22 and to 5.50 percent by the end of the year. Traders were increasingly anticipating another U.S. rate hike following last week's employment report. Activity data released on Monday revealed that input costs for UK service providers were under the greatest pressure in three months in May, while charges also rose significantly. Saudi Arabia's sharp production reduction has exacerbated inflationary concerns. However, according to the most recent CPI report, annual inflation in the United Kingdom fell to 8.7% in April from 10.1% in March, marking the first time since last summer that it has fallen below 10%.

Long-term Channels Trading Strategy for: (GBPUSD).Time frame (D1). The primary resistance is around (1.26641). The primary support is around (1.23091). Therefore, the next most probable price movement is a (consolidation) trend. (*see all other details on the chart).

Start trading in four simple steps

1. Register

Open your live trading account

2. Verify

Upload your documents to verify your account

3. Fund

Deposit funds directly into your account

4. Trade

Start trading and choose from 130+ instruments

Demo account

The Blue Suisse Trading Account with virtual funds in a risk-free environment

Demo accountLive account

The Blue Suisse Trading Account in our transparent live model environment

Open an Account- Trading Account types Trading conditions Trading hours Transparency Market Information

- Products Currencies Commodities Indices Stocks

- Tools MetaTrader 4 / 5 Mobile CRM, MAM and DSP

- Education Currency Trading for Beginners How to improve your trading CFD Trading

- Partnerships Asset- and Moneymanager Tied agent White labels FIX API

- Company About us Regulatory Our philosophy Careers FAQs Contact us