Uncertainty about the debt ceiling hanging over the market, again; Wall Street Fall on Debt Ceiling Talks Worries; Baltic Exchange Dry Index Extends Slide to 9th Session

GLOBAL CAPITAL MARKETS OVERVIEW, ANALYSIS & FORECASTS:

Author: Dr. Alexander APOSTOLOV (researcher at Economic Research Institute at BAS)

On Tuesday, European stocks declined, with Germany's DAX falling 0.4% and the Stoxx 600 declining 0.6%. The luxury goods sector was the worst performer, with shares of luxury goods companies such as LVMH, Hermès, and Kering declining between 4.5% and 7.5% due to fears of weakening demand in the United States. Deutsche Bank advises investors to be more selective with luxury stocks amidst mounting concerns about a slowdown in U.S. economic growth despite the strength of the Chinese and European economies. Aside from this, shares of Swiss bank Julius Baer fell more than 7 percent after the bank reported a modest rise in assets under management and inflows during the first four months of the year. Tuesday's closing price for the CAC 40 index was 7379 points, a reduction of approximately 1.1% from its opening price. Its performance was inferior to that of its regional competitors, and the luxury industry exerted pressure on it. Hermès (-6.5%), LVMH (-5%) and Kering (-3%) shares were the hardest impacted following a report by Deutsche Bank AG analysts. The U.S. decline is "worrisome," despite China's strong rebound and Europe's robust growth. Traders weighed the lack of real progress in U.S. debt ceiling negotiations against a succession of mixed PMI data from Britain and the U.S., the largest economy in the euro zone. Turning to domestic data, PMI data indicated that French business activity expanded for the fourth consecutive month in May. However, the expansion rate was the weakest in the current series and weaker than analysts had predicted. On Tuesday, the FTSE MIB index dropped approximately 0.5 percent to conclude at a near two-week low of 27,175, its second consecutive session of losses and in line with its European counterparts. The trajectory of interest rates and the continuing impasse in U.S. debt negotiations continue to dominate market sentiment. In May, business activity in the euro zone grew more slowly than anticipated, according to a new PMI survey, as manufacturing contracted further while services remained robust. Moncler (-5.4%), Ferrari (-3.3%), Amplifon (-2.6%), and Interpump Group (-2.6%) all had the worst performance among single hosiery.

Tuesday was a dull day for the FTSE 100 as investors analyzed PMI data and monitored the impasse in the U.S. debt trade. The purchasing managers' index from S&P Global fell short of expectations, indicating divergent trends in manufacturing and services. The production of service providers slowed, while manufacturing output declined for the third consecutive month. The fast-food chain SSP Group achieved a near three-month peak among individual stocks due to optimistic earnings projections. The stock price of Cranswick Plc increased by more than 4.5% following a report that robust demand increased annual profits. Patrick Drahi, a billionaire who increased his stake in BT Group, clarified that there are no intentions for a full takeover. The faulty performance of Pennon Group Plc prompted the water industry regulator Ofwat to launch an enforcement investigation into the company's stock price. In the meantime, market research firm Kantar reported a modest decline in domestic grocery inflation.

After a 173-point drop earlier in the session, the Dow traded near neutral. Early PMI data showed that the U.S. private sector, with services as its main driver, expanded more quickly than anticipated. Meanwhile, the S&P 500 and Nasdaq fell nearly 0.2% as investors remained wary of placing large wagers ahead of today's debt ceiling talks. Monday's meeting between Vice President Biden and House Speaker Kevin McCarthy was productive, but no agreement was reached. In the meantime, Lowe's stock rose nearly 3 percent, reversing a pre-IPO decline, after the company surpassed profit estimates but lowered its full-year sales forecast. Chevron shares rose roughly 2 percent after HSBC upgraded the stock to hold-buy status. Zoom, on the other hand, fell 7% despite reporting an increase in earnings per share and in-line guidance.

As investors returned from a long weekend, they weighed the lack of progress in U.S. debt talks and the Federal Reserve's more hawkish remarks, and the Canada S&P/TSX Composite dipped to around 20,270. Industrials and mining were the primary burdens on the market, while healthcare and energy companies advanced. Traders are awaiting earnings reports from the nation's leading banks this week. In recent business news, Scotiabank upgraded Meg Energy Corp to "sector outperform" from "sector perform." Canada's industrial price index decreased 0.2% in April from the previous month, marking the third consecutive monthly decline, while the producer price index decreased 3.5% on an annualized basis.

Since mid-May, the Russia ruble-based MOEX Russia index has remained above 2,600 points, close to April's all-time high, as stringent capital controls and an uncertain geopolitical backdrop prompted investors to prioritize the probability of dividend payments. Estimate revenue. This year, financials have outperformed, accumulating more than 30%. Recent EIA data indicating robust demand in China and India has fueled speculation that the discount of Russian oil to international benchmarks may continue to narrow. The mining industry increased by 16%, while gold producer Polymetal International PLC encountered difficulties with its relocation plans. Britain imposed a moratorium on Russian diamonds and restricted imports of copper, aluminum, and nickel originating from Russia. Additionally, the government issued new identities for individuals and businesses in Russia's energy, metals, defense, transportation, and financial sectors.

On Tuesday, the Hong Kong stock market closed at 19,431.25, down 246.92 points, or 1.25 percent, wiping out gains from the previous session and closing near their lowest level in two months, with technology, financial, consumer, and real estate equities all down more than 1 percent. Ten days before a potential U.S. default, investors were also apprehensive on Monday, when Washington leaders failed to reach an agreement on how to raise the debt ceiling. According to the Wall Street Journal, a surge in demand for travel, dining out, and other services has been the main factor supporting China's recovery. A slew of economic data in April fell short of market expectations, escalating uncertainty for a global economy already struggling with banking turmoil and high inflation. CK Hutchison Hlds. (-5.3%), China Hongqiao Group (-5.3), CK Assets Co., Ltd. (-5%) and Country Garden Hlds.

The Baltic Exchange's main sea freight index, which measures the cost of shipping goods around the globe, fell for the ninth consecutive day on Tuesday, falling approximately 1.1% to its lowest level since March 8 at 1,348 points, due to weak demand in all vessel segments. The capesize index, which tracks vessels typically carrying 150,000 metric tons of cargo such as iron ore and coal, fell 1.2% and held near a one-month low of 2,040; and the panamax index, which tracks ships that typically carry coal or grain cargoes of about 60,000 to 70,000 metric tons, posted its 20th straight daily decline, falling about 0.7 percent to its lowest level since Feb. 23 on 1212 points. The supramax index for smaller vessels fell 20 points, or 1.9%, to 1,040 points.

The Nikkei 225 fell 0.42% to close at 30,958, while the broader Topix fell 0.66% to close at 2,161, as investors retreated after the benchmark index rebounded strongly to its highest level since 1990. Expel some profits. Investors were also cautiously awaiting the latest news on U.S. debt-ceiling talks, with Treasury Secretary Janet Yellen reiterating that the U.S. could be at risk of defaulting on its debt by June 1. Meanwhile, data showed Japan's manufacturing sector returned to growth in May for the first time since October, while services sector activity hit a record high. Tokyo Electron (-2.6%), Toyota Motor (-4.8%), Advantest (-1.7%), Sony Group (-2.2%), Nintendo (-1.2%) and Daikin Industries (-1.7%).

Australia S&P/ASX 200 fell 0.05% on Tuesday to close at 7,260, falling for a second straight session as investors waited cautiously for the latest news on U.S. debt-ceiling talks, with Treasury Secretary Janet Yellen reaffirming that until June On the 1st, the United States may face the risk of debt default. Investors also digested data showing that manufacturing activity in Australia continued to contract in May, while service sector activity slowed. Index heavyweights fell significantly, such as BHP Billiton Group (-0.7%)

India's S&P BSE Sensex closed near the flat line at 61,982 on Tuesday after two consecutive sessions of gains, driven mainly by losses in IT stocks amid uncertainty over U.S. debt-ceiling talks. However, with continued upward momentum in the Adani stock and metals indices, the blue-chip Nifty 50 increased 0.2 percent to close at 18,348. Shares in Adani Group rose for a third straight session after market regulator the Securities and Exchange Board of India found no evidence of alleged irregularities in the group's overseas investments during an investigation. In other corporate news, shares in Divis's Laboratories Ltd. surged 3.6 percent, their second straight session of gains. The active pharmaceutical ingredient maker reported revenue and core profit figures for the March quarter that topped expectations.

The NZD 50 index fell 48.89 points, or 0.41%, to 11,944.20 on Tuesday, falling for a second straight session, as traders continued to take a cautious stance ahead of the Reserve Bank of New Zealand's interest rate decision on Wednesday. The central bank is widely expected to raise the cash rate by 25 basis points to 5.5% for the 12th consecutive time and could leave the door open for further tightening. The cash rate is expected to peak at 5.75% in July, according to Bloomberg News. Meanwhile, inflation fell to 6.7% in the first quarter of 2023, but remains far short of the board's 1-3% target. Separately, concerns about a U.S. debt default persisted as talks between President Biden and House Speaker McCarthy failed to make any progress. Consumer durables, healthcare, and manufacturing dragged down Gentrack Group Ltd. (-4.4%), Hallenstein Glasson (-3.2%), Scales Corp. (-2.7%), Fisher & Paykel Healthcare (-2.4%), and Mercury NZ Ltd. (-1.7%) sharply.

The Shanghai Composite Index fell 0.2% to close below 3,290 points, while the Shenzhen Composite Index fell 0.2% to 11,100 points, giving up some of the previous session's gains, with almost all sectors participating in the decline. On Monday, the People's Bank of China kept its key lending rate unchanged for the ninth straight month in a May revision to maintain support for the economy, even as the central bank remains under pressure to cut the reserve requirement ratio. Technology stocks led the decline, with TRS Information (-4%), 37 Interactive (-4.9%), Inspur Electronics (-2.5%), Shenzhen Kaiflux (-5.2%), and Zhejiang Jinke (-4.5%) falling sharply. Other heavyweights also fell, including China Shipbuilding Holdings (-25%), CSSC Technology (-8%), and Shanxi Xinghuacun (-2.9%).

REVIEWING THE LAST ECONOMIC DATA:

Reviewing the latest economic news, the most critical data is:

- US: In May 2023, the Fifth Region Service Industry Activity Receipts Index fell to -10 from -23 in April, against a consensus forecast of -29. Meanwhile, the demand index rose to -5 in May from -11 in April, but both indices remained in negative territory. Expectations about future income and demand also improved, with the income expectations index rising slightly to 0 in May from -5 in April, and the demand expectations index rising to 1 in May from -6 in the previous month. Additionally, the local current business conditions index rose to -17 in May from -27 in April. However, the local business conditions index is not expected to improve, rising to -20 from -19 in the previous month. All three spending indices edged up, with services spending showing the biggest gain, rising to 3 in May from -3 in April. The employment index rose to 0 in May from -4 in April, ending its steady decline since the start of the year as wages continued to rise.

- US: Sales of new U.S. single-family homes unexpectedly rose 4.1% month-over-month in April 2023 to a seasonally adjusted annualized rate of 683,000 units, the highest level since March last year, versus the forecast of 665,000 units. However, the March 2023 figure was revised down sharply to 656,000 from the initial estimate of 683,000. In April, sales in the South and Midwest rose 17.8 percent and 11.8 percent, to 443,000 and 76,000, respectively, but sales in the Northeast and West fell 58.6 percent and 9.1 percent, to 24,000 and 14,000, respectively. The median new home sale price was $420,800, and the average sale price was $501,000, compared with $458,200 and $562,400, respectively, a year ago. There are 433,000 homes left for sale, which equates to a 7.6-month supply at the current sales pace.

- US: Preliminary estimates showed the S&P Global U.S. Composite PMI rising to 54.5 in May 2023, up from 53.4 the previous month. Growth in the services sector accelerated to a 11-month high, helped by stronger demand conditions, the latest data showed, marking the fastest expansion of the country's private sector since April 2022. Meanwhile, manufacturing output rose only marginally. While exports fell for a 12th straight month, total new orders rose for a third straight month, and employment rose at the fastest pace since July 2022. On the price front, input prices for manufacturers fell for the first time in three years, while cost burdens for service providers continued to rise significantly. On the other hand, output cost inflation is still rising by the survey's historical standards. Finally, business expectations for the coming year improved on hopes of a pick-up in demand conditions and plans to invest in new products and marketing.

- US: Preliminary estimates showed the S&P Global U.S. manufacturing PMI falling to 48.5 in May 2023 from 50.2 in April, well below the 50 forecast. The data showed that the manufacturing sector contracted the most in three months, and business conditions deteriorated again. The decline was mainly due to weaker demand and lower demand for holding inputs following shorter lead times and a lower inflow of new orders. Meanwhile, output slowed, while payrolls posted their biggest gain since September. Increased capacity helps companies grapple with unfinished work. The backlog of orders fell sharply and at the fastest rate in three years. Meanwhile, input prices fell for the first time since May 2020, and supplier lead times also saw their biggest improvement on record. Finally, optimism about the outlook for output over the next 12 months hit its highest level in a year as companies sought to invest in new product development and hoped that customer demand would increase.

- US: Preliminary estimates show that in May 2023, the S&P Global U.S. Services PMI rose to 55.1 from 53.6 in the previous month, well above market expectations of 52.6. The pace of activity growth was the fastest in more than a year, with the company linking the growth to greater demand from new and existing customers. New orders rose at the fastest pace since April 2022, and new export orders rose at a steady pace for the first time in a year. In addition, the pace of job creation was the fastest in ten months. On the price side, input prices and output charges increased faster than their respective series averages. Looking ahead, confidence returned to its highest level in a year on hopes of continued growth in customer demand.

- CA: Canadian Industrial Producer Prices unexpectedly edged down 0.2% on a month-to-month basis for April 2023, compared to market expectations for a 0.2% rise and following a revised 0.1% decline the previous month. This marked the third consecutive month of deflation for producers, largely due to lower prices for refined petroleum energy products (-2.1%), namely diesel (-8.7%), jet fuel (-7.5%), and light fuel oil ( -10.2%). Softwood lumber (-4.7%) provided additional downward pressure, partly due to cooling housing markets in the US and Canada amid rising interest rates; and chemicals and chemical products (-1%), with ammonia and fertilizers (-9.3%) because of lower natural gas prices. In contrast, the IPPI increased for non-ferrous metal products (+1.8%) and meat products (+2%). On an annualized basis, producer prices fell 3.5% in April, the biggest drop since May 2020, after an upwardly revised 2.2% drop the previous month and compared with market forecasts for a 5.6% drop.

- CA: In April 2023, the Canadian raw material price index rose by 2.9% month-on-month, the largest increase since May 2022, and the increase exceeded market expectations of 0.7%. Crude energy product prices rose by 4.4%, mainly due to higher conventional crude oil prices (+5.3%). On the other hand, crop product prices fell by 1.8%, mainly due to lower prices of rapeseed (-3.1%) and other crop products (-1.8%). Canadian raw material prices fell 10.8% year-over-year.

- IT: In March 2023, Italy posted a current account surplus of 3.711 billion euros, fluctuating from a year-ago deficit of 1.178 billion euros, as the goods surplus widened significantly from 488 million euros to 8.210 billion euros due to lower energy prices. At the same time, the primary income surplus narrowed from 2.926 billion euros to 0.69 billion euros; the secondary income gap increased from 2.464 billion euros to 2.753 billion euros, and the service deficit increased from 2.128 billion euros to 2.411 billion euros.

- TW: In April 2023, Taiwan's retail sales rose 7.5% year-on-year, up from a three-month high of 7.1% in the previous month. This is the strongest increase in retail activity since December 2022, driven primarily by higher sales of textiles and apparel in specialty stores (29.37% vs. 1.27% in March) and other retail sales in specialty stores (23.47% vs. 11.88%). Meanwhile, sales of home appliances and merchandise in specialty stores rebounded (11.08% vs. -0.94%), and sales of cultural and entertainment goods rebounded (4.9% vs. -5.43%). At the same time, sales of food, beverages, and tobacco fell (-2% vs. 6.11%), sales of pharmaceuticals, medical supplies, and cosmetics fell (1.17% vs. 5.6%), and sales of motor vehicles and motorcycles dropped sharply. slow (11.26% vs. 28.38%). Retail trade fell 0.17% month-on-month in April, higher than the 11.9% increase in the previous month.

- UK: Preliminary estimates showed the S&P Global/CIPS UK Services PMI falling to 55.1 in May 2023 from 55.9 the previous month, below the consensus 55.5. Budgetary pressures from corporate customers, rising economic uncertainty, and rising borrowing costs are among the reasons holding back growth. However, the travel, leisure, and hospitality industries commented extensively on resilient consumer demand. New business growth in the services sector was strong, with new orders from abroad rising. Meanwhile, staff hiring reflected rising business demand. In terms of prices, the cost burden on service providers increased the most in three months. Looking ahead, business optimism eased in May.

- EU: Preliminary estimates show that in May 2023, the Eurozone HCOB manufacturing PMI fell to 44.6 from 45.8 in April, well below the forecast of 46.2. The factory sector saw its worst contraction in three years, with output, new orders, and backlogs falling even faster, the data showed. Meanwhile, input prices fell the most since February 2016 as employment rose slightly amid lower energy costs and ample supplies. In addition, manufacturers cut input purchases at the fastest pace in three years, leading to a sharp drawdown in inventories. Finally, optimism about the year ahead has declined further. Among the EU's largest economies, the decline in manufacturing was particularly pronounced in Germany (42.9 vs. 44.5).

- EU: Preliminary estimates show that in May 2023, the HCOB Eurozone Services PMI edged down to 55.9 from a 12-month high of 56.2 in April, compared to a consensus forecast of 55.6. Despite the smaller decline, data continued to point to strong growth in the services sector, with new orders rising for a fifth straight month, backlogs rising slightly and employment growth the second-strongest over the past year. At the same time, the average price levied on services remained elevated, mainly due to wage and salary costs. Finally, optimism about the year ahead slipped further.

- EU: In March 2023, the euro area's current account surplus widened sharply to €45 billion, the largest surplus since March 2018, as the goods surplus surged to a record high of €52.1 billion. Also, the primary income surplus rose to 3.6 billion euros from 1.5 billion euros in the same month last year, while the services surplus fell to 4.1 billion euros from 11 billion euros. Finally, the secondary revenue deficit rose to 14.8 billion euros, an increase from a deficit of 11.0 billion euros a year earlier. Taking into account the overall picture in the first quarter, the euro area's current account surplus was 65.3 billion euros, in stark contrast to the 8.4 billion euro deficit reported in the same period in 2022.

- EU: Preliminary estimates showed that the HCOB Flash Eurozone Composite PMI fell to 53.3 in May 2023 from 54.1 in April, below the consensus forecast of 53.7. However, the data marked the fifth straight month of expansion in private sector activity, pointing to strong but uneven economic growth so far in the second quarter. Services continued to perform strongly (55.9 vs 56.2), while manufacturing activity contracted at a faster pace (44.6 vs. 45.8). In May, output growth outpaced new orders to the highest level since early 2009 as demand growth all but stalled. Meanwhile, employment slowed, and average prices for goods and services rose at the slowest pace in 25 months. Finally, optimism about the year ahead fell further from a 12-month high in February, amid heightened concerns over weak customer demand and rising interest rates.

- FR: Preliminary estimates show that in May 2023, the HCOB French manufacturing PMI rose to 46.1 from 45.6 in the previous month, almost in line with market expectations of 46. It was the fourth straight month of contraction in French factory activity, as new orders and output continued to fall sharply. Also, export orders fell for a second straight month, hurt by worsening international demand. As a result, procurement activity also fell, while backlogs fell for the fourth straight month. On the price front, input costs fell for the first time since July 2020 as raw material and energy prices fell, prompting output charges to slow at their slowest pace in two-and-a-half years. Looking ahead, French manufacturers remained optimistic over the next 12 months, but optimism fell to a five-month low.

- GE: Preliminary estimates show that the HCOB Germany Composite PMI edged up to 54.3 in May 2023 from 54.2 in the previous month, easily beating the consensus of 53.5. The latest data showed the economy expanded for the fourth straight month, the fastest pace in more than a year. The services sector, which saw the biggest increase since August 2021, was the sole driver of the expansion while manufacturing production fell back into contraction. Overall inflows of new business and backlogs fell, while employment continued to rise, albeit at a slower pace. On the price front, cost pressures remained concentrated in the services sector, with reports of higher wage costs and adjustments for generally high inflation. Finally, business expectations for activity in the coming year weakened in May.

- GE: According to preliminary estimates, Germany's HCOB flash memory manufacturing PMI fell from 44.5 in April to 42.9 in May 2023, far below the forecast of 45. The data showed that manufacturing saw its biggest drop since May 2020, as output returned to contraction territory after a modest increase in the previous three months, led by falling new orders. Customers have delayed or canceled orders due to high inventory levels and uncertainty about the outlook. In addition, manufacturers' work at hand fell sharply, at the fastest pace since November, as supplies of materials continued to improve. At the same time, factory price inflation was near stagnation as input costs continued to fall sharply, and employment rose at its weakest rate in 27 months. Finally, business sentiment on the outlook turned negative for the first time in five months.

LOOKING AHEAD:

Today, investors should watch out for the following important data:

- AUD: MI Leading Index m/m.

- CAD: Corporate Profits q/q.

- NZD: Retail Sales q/q, Core Retail Sales q/q, Official Cash Rate, RBNZ Monetary Policy Statement, RBNZ Rate Statement, and RBNZ Press Conference.

- USD: Treasury Secretary Yellen Speaks, Crude Oil Inventories, and FOMC Meeting Minutes.

- GBP: CPI y/y, Core CPI y/y, PPI Input m/m, PPI Output m/m, RPI y/y, HPI y/y, BOE Gov Bailey Speaks, CBI Industrial Order Expectations, 10-y Bond Auction, and BOE Gov. Bailey Speaks.

- EUR: German ifo Business Climate, German Buba Monthly Report, and Belgian NBB Business Climate.

KEY EQUITY & BOND MARKET DRIVERS:

Кey factors in the stock and bond market are currently:

- US: U.S. futures lacked direction on Tuesday, with the Dow Jones futures contract down nearly 60 points, while the S&P 500 and Nasdaq traded near flatlines. The debt-ceiling standoff remains in the spotlight, with President Joe Biden and House Speaker Kevin McCarthy expressing optimism after Monday's meeting that talks will continue this week despite a government debt deal that hasn't been reached yet. Treasury Secretary Janet Yellen reiterated her warning that the Treasury may no longer be able to meet all of the government's obligations if Congress does not act to raise or suspend the debt limit by early June, possibly as early as June 1. Meanwhile, Lowe's shares fell nearly 1% in premarket trading after Lowe's lowered its full-year sales forecast. BJ's Wholesale and Dick's Sporting Goods are also due to report quarterly results. On the data front, flash PMIs and new home sales for May are also due.

- US: U.S. 10-year Treasury yields rose to 3.72%, the highest level since mid-March, as investors focused on the debt ceiling impasse and the outlook for monetary policy. President Biden and House Speaker Kevin McCarthy expressed optimism after a meeting on Monday that negotiations will continue this week even though a government debt deal has yet to be reached. Treasury Secretary Janet Yellen reiterated her warning on Monday that the Treasury may no longer be able to meet all of the government's obligations if Congress does not act to raise or suspend the debt limit by early June, possibly as early as June 1. On the monetary policy front, traders will continue to focus on any comments from Fed officials on the Fed's next move. Market participants currently see an 80 percent chance that the Fed will keep rates steady in June.

LEADING MARKET SECTORS:

- Strong sectors: Energy, Utilities.

- Weak sectors: Materials, Consumer Staples, Health Care, Industrials.

TOP CURRENCY & COMMODITIES MARKET DRIVERS:

Кey factors in the currency and commodities market are currently:

- CAD: The Canadian dollar held near 1.35 against the U.S. dollar as investors focused on the latest developments in Canadian and U.S. monetary policy. Concerns have grown that the Bank of Canada may be forced to resume rate hikes after data showed inflationary pressures remained elevated. Consumer prices rose an annualized 4.4% in April, well above expectations for a 4.1% increase, breaking a record 10-month streak of slowing inflation amid sharp increases in mortgage costs and rents. Also in the US, comments from several Fed officials raised expectations that interest rates would remain elevated for longer. The Fed's Bullard said a half-percentage-point increase in interest rates was possible this year, while the Fed's Kashkari said a decision to pause or raise rates in June was a close call.

- USD: The U.S. dollar index edged up to 103.5 on Tuesday, returning to its highest level since mid-March, as comments from several Federal Reserve officials raised expectations for longer-term rate hikes. The Fed's Bullard said a half-percentage-point increase in interest rates was possible this year, while the Fed's Kashkari said a decision to pause or raise rates in June was a close call. Traders are now pricing in an almost 77% chance of a pause in the rate hike cycle next month, while the chance of a 25 basis point hike rose to 23% from 20% last week. On the other hand, expectations for a rate cut this year have declined. Meanwhile, talks on the U.S. debt limit will continue this week after President Joe Biden and House Speaker Kevin McCarthy expressed optimism after a meeting on Monday.

- GBP: Sterling fell below $1.24, its weakest in four weeks, as investors assessed Bank of England policymakers' expectations for upcoming inflation data. Bank of England Governor Bailey acknowledged that inflation has taken a positive turn and expressed confidence in the central bank's ability to bring it back to target levels. In addition, BoE Pill said long-term expectations were not significantly off target. UK annual inflation in May is set to fall below double digits for the first time since last August. Meanwhile, the latest PMI survey showed that UK GDP was likely to grow by 0.4% in the second quarter, avoiding a contraction after expanding by 0.1% in the first quarter. However, Britain's economic growth in May remained centered around the services sector, while production levels at manufacturing firms saw their biggest drop in four months.

- EUR: The euro has fallen below $1.08, near a seven-week low of $1.0758 hit on May 19, as investors process the latest PMI survey and grapple with uncertainty surrounding the U.S. debt deal. Growth in business activity in the euro zone slowed more than expected in May, mainly due to weak expansion in services and a sharp drop in manufacturing output, survey data showed. Notably, German factory output saw its sharpest contraction in three years. Regarding monetary policy, the European Central Bank is expected to continue raising interest rates throughout the year. ECB board member Isabel Schnabel recently stressed the importance of the central bank's commitment to fighting inflation with "determination," while ECB President Christine Lagarde assured that necessary steps would be taken to counter price pressures.

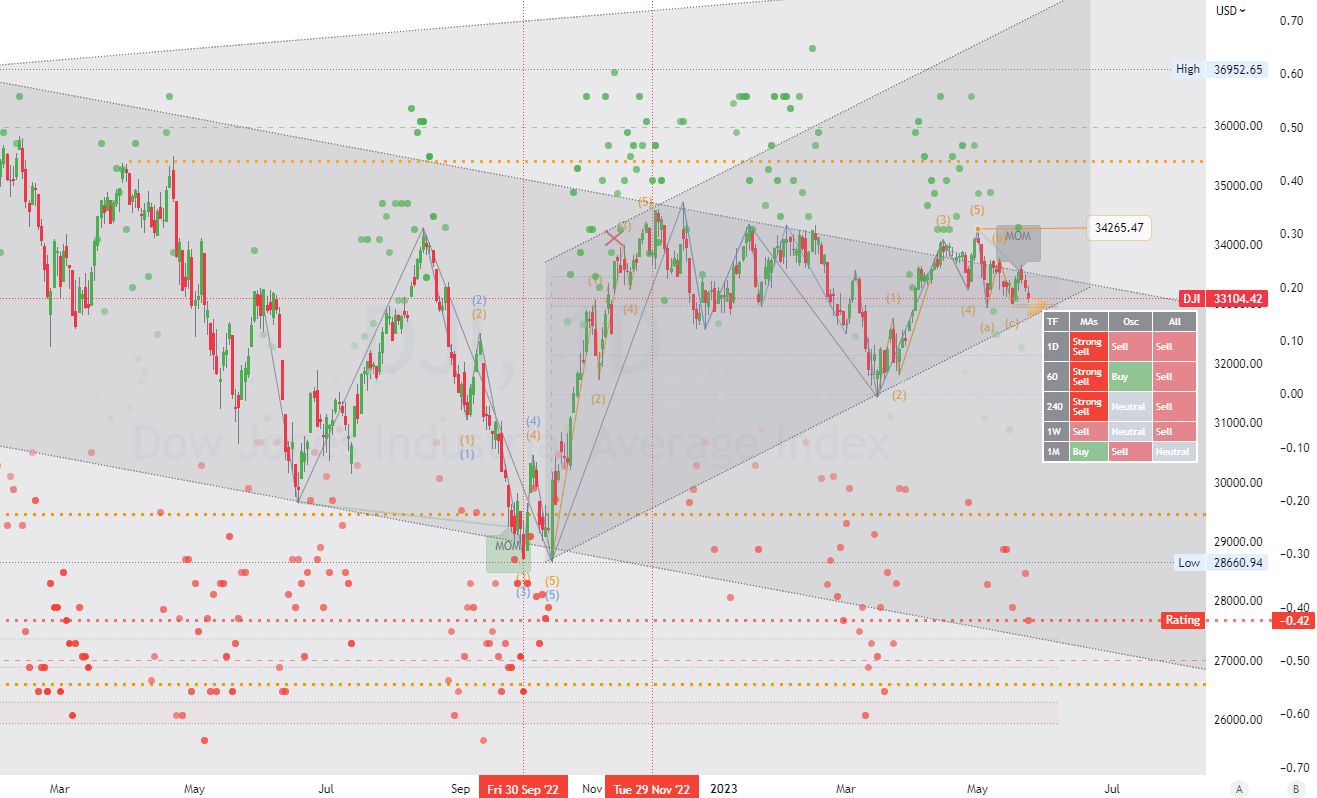

CHART OF THE DAY:

The Dow traded near flat after falling 173 points earlier in the session. Earlier, new PMIs demonstrated that the U.S. private sector, with services as its main driver, expanded faster than anticipated. Meanwhile, the S&P 500 and Nasdaq fell nearly 0.2% as investors remained cautious about making big bets with debt ceiling talks set to resume today. A meeting between President Biden and House Speaker Kevin McCarthy on Monday was productive but failed to reach an agreement. Meanwhile, shares of Lowe's rose nearly 3%, bouncing back from a pre-IPO loss after the company topped profit estimates but lowered its full-year sales forecast. Elsewhere, Chevron shares surged nearly 2% after HSBC upgraded the stock to a hold-buy rating. Zoom, on the other hand, fell 7% despite reporting upbeat EPS and in-line guidance.

Long-term Channels Trading Strategy for: (US Dow index).Time frame (D1). The primary resistance with a potential (consolidation area) is around (34265). The primary support with a potential (target area) is around (32788). Therefore, the next most probable price movement is a (consolidation/down) trend. (*see all other details on the chart).

Start trading in four simple steps

1. Register

Open your live trading account

2. Verify

Upload your documents to verify your account

3. Fund

Deposit funds directly into your account

4. Trade

Start trading and choose from 130+ instruments

Demo account

The Blue Suisse Trading Account with virtual funds in a risk-free environment

Demo accountLive account

The Blue Suisse Trading Account in our transparent live model environment

Open an Account- Trading Account types Trading conditions Trading hours Transparency Market Information

- Products Currencies Commodities Indices Stocks

- Tools MetaTrader 4 / 5 Mobile CRM, MAM and DSP

- Education Currency Trading for Beginners How to improve your trading CFD Trading

- Partnerships Asset- and Moneymanager Tied agent White labels FIX API

- Company About us Regulatory Our philosophy Careers FAQs Contact us