Reacting to more central bank rate hikes from the likes of the Bank of England, Swiss National Bank, and Norges Bank; Falling Treasury yields; Turkish stocks are down nearly 12% so far this year; S&P 500 running into resistance at the 4,000 level

GLOBAL CAPITAL MARKETS OVERVIEW, ANALYSIS & FORECASTS:

Author: Dr. Alexander APOSTOLOV (researcher at Economic Research Institute at BAS)

The BIST 100 index was around 5,000 at the end of March, down nearly 12% since the start of 2023, as investors shrugged off government measures to prop up the stock market after the quake and continued to feel uneasy about the political risk posed by the upcoming parliamentary and presidential elections. After the devastating earthquake of February 6, billions of lire were indirectly placed on the market, including eliminating 15% of the withholding tax on treasury share buyback programs and increasing to 30% of the fund's mandatory quotas state pension. from 10%.Meanwhile, the Turkish central bank kept the interest rate stable at 8.5% for the second time at its March 2023 meeting, as expected after a 50 basis point cut in the previous month.

U.S. stocks ended a volatile session in positive territory on Thursday as investors attempted to recover from Wednesday's sell-off. The Dow rose more than 75 points, while the S&P and Nasdaq gained 0.3% and 1%, respectively. Tech stocks led the gains, namely Microsoft (2%), Nvidia (2.7%), Meta (2.2%), and Apple (0.7%), while Treasury yields fell. The Fed raised the fund's rate by 25 basis points and said it would raise rates by another 25 basis points this year. Despite the central bank's cautious tone to prevent further turmoil in the financial sector, Chairman Jerome Powell questioned the dovish outlook in money markets. He said a rate cut should be different than expected this year. Today, Treasury Secretary Janet Yellen said the federal emergency actions used to support Silicon Valley Bank and Signature Bank customers could be used again to stabilize the U.S. banking system if necessary.

The S&P/TSX Composite index closed down 0.3% on Thursday near 19,450, tracking losses among Wall Street peers, with heavyweight energy, banks, and miners weighing on the index. Investors continued to digest the Fed's policy decision and the threat to banking stability. Energy producers led losses, falling nearly 1.7 percent, followed by banks, which fell 0.6 percent as investors assessed risks in the U.S. banking sector.

The Baltic Exchange's leading shipping index, which measures the cost of shipping goods worldwide, broke its two-day losing streak on Thursday, climbing about 1.9% to 1,484 points, its biggest daily gain since March 14th. The Capesize index, which tracks iron ore and coal cargoes of 150,000 tons, also halted its two-day decline, climbing 5.9% to 1,856 points. “Next week looks a little slow looking at the cargo list. However, that could change quickly, and the list of vessels heading to Brazil is not very significant, so sentiment can change overnight.”, Meanwhile, the Panamax index, which tracks cargoes of coal or grain from about 60,000 tons to 70,000 tons, fell for the sixth consecutive day, down about 1.4% to its lowest level since March 7 at 1,584 points;

European shares were weaker in Thursday afternoon trading as investors digested interest rate hikes from central banks, including the Federal Reserve, Bank of England, Swiss National Bank, and Norges Bank. The Stoxx Bank Index fell more than 2% after Citigroup downgraded its rating on European banks to "neutral" from "overweight," saying possible continued monetary tightening fueled concerns about global banking turmoil. Meanwhile, Treasury Secretary Janet Yellen told Congress she was not considering or discussing anything related to blanket insurance or deposit guarantees. The CAC 40 edged up to 7,139 on Thursday, extending a rally that started on Monday. Investors priced in a continued monetary tightening in Europe, and the Federal Reserve softened its rhetoric on the next rate hike. Meanwhile, Citigroup downgraded its rating on European banks, warning that a rapid rise in interest rates could further weigh on economic activity and bank performance. Among individual stocks, Sanofi was the best performer (+5.5%) after the pharmaceutical group's asthma and eczema drug Dupixent hit all its targets in a trial to treat "smoker's lung," giving the French stock a big boost. Growth prospects for drugmakers. On the other hand, rate-sensitive real estate firm Unibail Rodamco Westfield was down the most (-3.4%), followed by Teleperformance (-2.6%) after it announced it would maintain its full content moderation service, including the most aggressive part. Societe Generale and BNP Paribas also fell more than 2% each. The FTSE MIB closed just below the flatline at 26,480 on Thursday, extending a slight retreat from the previous session, as losses from banks offset gains from utilities and technology companies. At the same time, investors digested gains from major central banks—a series of rate hikes. As loosely expected, the Fed raised its fund's rate by 25 basis points after yesterday's close but struck a dovish tone in its report to address recent instability in the banking sector. Meanwhile, the BoE and Norges Bank raised interest rates by 25 basis points, while the Swiss National Bank increased its main borrowing costs by 50 basis points. Banco BPM shares fell 3 percent, leading the sector lower. Shares of Inwit, on the other hand, surged more than 5% on reports that Ardian and JPMorgan Chase & Co could take over the wireless network operator privately. The IBEX 35 fell further to 8960 on Thursday, trailing its European counterparts amid renewed pressure from financials. Yesterday the Fed raised rates by the expected 25 basis points but ruled out the possibility of interest rate cuts this year. Adding to the concerns, Treasury Secretary Janet Yellen signaled no move to expand bank deposit insurance, and Citigroup downgraded the European banking sector's rating to "neutral" from "overweight." Lenders trailed the index, with CaixaBank (-2.36%) and BBVA (-2.05%) suffering the biggest losses. In other news, the Fidelity International fund reduced its stake in Bankinter's capital to 2.830% from the previous 3.025%, and Banco Santander raised its prime rate from 7.75% to 8.0%.

The ruble-based MOEX Russia index closed just below flatline at 2,388 on Tuesday, extending a slight retreat from the previous session, as modest losses in banks and energy stocks offset gains in miners and metallurgists. Tatneft led the decline in the oil and gas sector, down 1.6 percent, as investors continued to digest the company's dividend announcement earlier this week. On the other hand, Gazprom edged higher after Russian Deputy Prime Minister Novak said negotiations on a contract to build the Power of Siberia 2 pipeline to China were in the final stages. The pipeline will significantly increase gas exports to China, which is crucial for Gazprom's rebound in the current situation of low TTF prices and the destruction of Nord Stream 1. Mechel, meanwhile, has underperformed other steelmakers, with shares down nearly 2% after reporting poor results for 2022.

The Hong Kong stock market rose 458.21 points, or 2.34%, to close at 20,049.64 points on Thursday, rising for the third consecutive day, as investors digested the recent decision of the Federal Reserve. The Fed announced a 25-basis-point rate hike on Wednesday, saying it may pause rate hikes and reaffirming its commitment to curbing inflation. Meanwhile, traders shrugged off a statement from Treasury Secretary Janet Yellen, who said the U.S. government ruled out broadly expanding insurance to protect savers and would only act on a case-by-case basis. Technology stocks led the gains, followed by consumer and financial stocks. Real estate stocks edged higher, even as China Evergrande's debt restructuring proposal appeared unattractive due to long repayment periods and a lack of sweeteners. Shares rose 7% after Tencent reported upbeat quarterly revenue. The other top gainers were Orient Overseas International (16.7%), Lenovo Group (10.8%), and Xiaomi Corporation (7.1%).

Japan Nikkei 225 fell 0.17% to close at 27,420. In comparison, the Topix fell 0.29% to close at 1,957, paring gains from the previous session to track Wall Street's decline as the Fed raised interest rates another 25 basis points. At the same time, Federal Reserve Chairman Jerome Powell said officials would not cut rates this year and are prepared to raise rates higher than expected if needed. Treasury Secretary Janet Yellen also told lawmakers that the U.S. government is not considering "blanket insurance" for bank deposits, weighing on financial stocks. Meanwhile, investors digested data showing Japanese manufacturers remained pessimistic for a third straight month in March amid concerns that slowing global growth could hurt the country's export-heavy industries. Financials, healthcare, and technology stocks led losses, with Mitsubishi UFJ (-1.4%), Takeda Pharmaceutical (-2.6%), and Keyence (-1.6%) falling.

China Shanghai Composite Index edged up 0.05% to close at 3,267 points, while the Shenzhen Composite rose 0.55% to close at 11,559 points, rising for a third consecutive session. Still, market caution capped gains as the Federal Reserve Resisted bets on rate cuts this year. Treasury Secretary Janet Yellen told lawmakers the U.S. government is not considering "blanket insurance" for bank deposits. The Fed raised interest rates by 25 basis points, while Fed Chairman Jerome Powell said officials would not cut rates this year and were prepared to raise rates higher than expected if needed. Technology stocks led the gains, extending their recent outperformance, with Inspur Electronics (6.5%), HKUST Xunfei (8.8%), Foxconn Industrial (6%), United Nations Letter (8.5%)

New Zealand shares rose 8 points, or less than 0.1%, to 11,594.94. U.S. stock futures rose sharply after Wall Street slumped on Wednesday after Federal Reserve Chairman Jerome Powell said the central bank remained focused on reducing inflation. Meanwhile, Treasury Secretary Yellen said the Biden administration was not considering expanding deposit insurance amid the current banking crisis, adding that decisions would only be made in specific circumstances. Locally, a senior central bank governor said today that New Zealand's cash rate, which has risen by 450 basis points over the past 1-1/2 years, is still "penetrating" through the economy and will weigh on consumer spending. Embark Education rose 5.6 percent, while Eroad Ltd. and Mainforture Ltd. gained 4 percent and 2.5 percent, respectively. By comparison, Warehouse Group fell 11.7 percent, Bremworth 10 percent, Aofrio Ltd 9.6 percent, and Air New Zealand 0.7 percent.

Australia S&P/ASX 200 fell 0.8% to around 6,960 on Thursday, snapping two days of gains and taking cues from Wall Street's negative lead as the Fed hiked rates by another 25 basis points. At the same time, Fed Chairman Jay Rohm Powell said officials would not cut rates this year and are prepared to raise rates more than expected if needed. Treasury Secretary Janet Yellen also told lawmakers that the U.S. government is not considering "blanket insurance" for bank deposits, weighing on financial stocks. Tech and clean energy-related stocks led losses, with Computershare (-2.3%), Xero (-2.1%), Block Inc (-5.6%), Pilbara Minerals (-5.4%), and Lynas Rare Earths (-4%) down. Financials also fell, including Macquarie Group (-1.7%), Bank of Canada (-0.6%), ANZ (-0.9%), Westpac (-0.4%), and National Australia Bank (-0.9%). %.).

Brazil's Ibovespa index closed Thursday 2.4% down around the 97,700 level, its lowest in more than eight months, as investors weighed the latest policy decision from Brazil's central bank and Federal Reserve. Brazil's Copom kept the Selic rate unchanged at 13.75%, as expected, but signaled it "will not hesitate" to resume the monetary tightening cycle depending on the macroeconomic scenario. In recent weeks, President Luiz Inácio Lula da Silva has criticized central bank head, Roberto Campos Neto, saying high-interest rates will certainly hurt the economy. Meanwhile, the Federal Reserve raised the federal funds rate by 25 basis points and indicated only one more rate hike this year.

REVIEWING THE LAST ECONOMIC DATA:

Reviewing the latest economic news, the most critical data is:

- EU: In the last three months of 2022, the number of insolvency declarations by EU companies rose by 26.8% quarter-on-quarter, reaching the highest level since data collection began in 2015. The number of bankruptcy filings increased in all four quarters of 2022. The activities with the largest increase in the number of bankruptcies in the fourth quarter of 2022 compared to the previous quarter were transport and warehousing (+72.2%), accommodation and food services (+39.4%), and education, health, and social activities (+29.5%). The largest decreases were in Belgium (-17.6%), Romania (-17.3%), and Lithuania (-10.8%), while the largest increases in new business registrations were in Ireland (+112.6%), Spain (+7.4%), and France ( +2.8%).

- EU: Preliminary estimates show that in March 2023, the Eurozone consumer confidence index edged down by 0.1 percentage points to -19.2, below market expectations of -18.3, but still close to its highest level in more than a year. While there are signs that inflationary pressures may be easing in many European countries, higher interest rates and the recent turmoil in the banking sector may start to affect consumer behavior. Across the EU, consumer sentiment was also little changed at -20.7. Still, confidence remains below pre-pandemic levels and its long-run average.

- US: The Kansas City Fed’s manufacturing production index rose to 3 in March 2023 from -9 in the previous month. It was the highest reading since last July. Activity at food manufacturing plants increased, while activity at nondurable goods plants declined in March, particularly printing, plastics, and chemical manufacturing. Indexes for production, shipments, and finished goods inventories rose slightly, while indexes for new orders, supplier lead times, and materials inventories declined. The monthly price index was mixed, with material prices rising but finished product prices falling slightly.

- US: Sales of new single-family homes in the U.S. rose 1.1% month-over-month to a seasonally adjusted annualized rate of 640,000 in February 2023, the highest level since last August, but below the forecast of 650,000. This follows a downward revision of 633K in January. Sales in the West rose 8.1% to 133,000; in the South, they rose 3% to 415,000, offsetting declines in the Midwest (-1.4% to 71,000) and the Northeast (-40% to 21,000). The median new home sale price was $438,200, and the average sale price was $498,700, compared with $427,400 and $522,200, respectively, a year ago. There are 436,000 homes left for sale, the lowest level since April 2022, or 8.2 months' supply at the current sales pace.

- US: U.S. building permits for February 2023 were revised up to a seasonally adjusted annual rate of 1.55 million in February 2023 from an initial estimate of 1.524 million. It remained the highest reading in five months, with both single households (8.9% to 786,000 from an initial rate of 777,000) and multisector mandates (23.8% to 764,000 from 747,000) revised higher. In addition, licenses increased in all four regions: the South (11.1 percent to 863,000 compared to the original 845,000), the West (28.3 percent to 376,000 compared to 3.81 million), the Midwest (10.1 percent to 196,000 compared to the initial 195,000).

- US: The Chicago Fed National Activity Index fell to -0.19 in February 2023 from +0.23 in January. All four categories of indicators used to construct the index made negative contributions, with three of them deteriorating from January. Indicators related to production contributed -0.08, down from +0.15 in January; indicators related to employment contributed -0.02, down from +0.10; and personal consumption and housing categories fell to -0.08 from +0.10. On the other hand, the contribution of sales, orders, and inventories rose to -0.02 from -0.12 in the previous month. The three-month moving average rose to -0.11 in February from -0.27 in January. The CFNAI Diffusion Index, a three-month moving average, rose from -0.07 in January to +0.02 in February.

- US: In the fourth quarter of 2022, the U.S. current account deficit narrowed to $206.8 billion, the lowest level since mid-21 years, below market forecasts for a gap of $211.2 billion. This primarily reflects a reduction in the secondary income deficit and a widening surplus in the services sector. However, considering the full year 2022, the current account deficit widens by $97.4 billion to $943.8 billion. That equates to 3.7% of the gross domestic product in current dollars, the highest level since 2008 and up from 3.6% in 2021. Again, the widening primarily reflected widening deficits in goods and secondary income, partly offset by a widening surplus in primary income.

- UK: At its March 2023 meeting, the Bank of England raised its key bank rate by 25 basis points to 4.25%, as expected, and pushed borrowing costs to fresh 2008 highs, aiming to bring inflation back to its 2% target. Inflation in the UK unexpectedly edged up to 10.4% from 10.1% last month. However, inflation will likely fall sharply for the rest of the year, falling to a lower-than-expected level in February. Still, policymakers have warned that further tightening is needed if evidence of more persistent pressures exists. With regard to the recent banking crisis, the central bank noted that the UK banking system maintains sound capital and strong liquidity positions and remains resilient. Policymakers will also continue to monitor closely any impact on credit conditions facing households and businesses, and thus the macroeconomic and inflation outlook.

- TW: In February 2023, Taiwan's broad M2 money supply increased by 6.8% year-on-year to NT$5,848.6 billion, slightly higher than the previous month's 6.67%. This increase was mainly due to net foreign capital inflows and higher annual growth rates of loans and investments. Considering the first two months of 2023, the cumulative annual growth rate is 6.73%.

- TW: Taiwan's retail sales rose 4.6% year-on-year in February 2023, following a 4.2% increase in the previous month. The retail activity of motor vehicles and motorcycles resumed (26.9% in January, vs. -11%), non-store retail trade (5%, vs. -5.4%), electronic shopping (6.2%, vs. -3.5%), Food, beverages and tobacco (2.1%, vs. -6%), and fuel and related products (1.5%, vs. -1.1%), while other retail sales rose further (14.6%, vs. 11.5%). Meanwhile, general merchandise sales slowed (3.3 percent versus 16.3 percent), as well as pharmaceutical and medical supplies and cosmetics (3.9 percent versus 7.7 percent). In addition, textiles, clothing (-8.3% vs. 23.4%), and cultural and recreational goods (-6.2% vs. 8.3%).

- TW: Taiwan's industrial output fell 8.68% year-on-year in February 2023, the sixth consecutive month of decline, although it eased sharply from a near 14-year high and was revised upwards from a 20.95% drop last month as manufacturing (- 9.15% vs. -21.82% in January) and output fell in both electricity and gas supply (-27.7% vs. -7.09%). Additionally, output increased in mining and quarrying (24.46% vs. 15.8%) and water supply (1.62% vs. -0.64%). As a result, on a seasonally adjusted basis, industrial activity fell further to 4.53% in February after falling 3.84% the previous month.

- HK: In February 2023, Hong Kong's annual inflation rate rose to 1.7% from 2.4% in the previous month. It was the slowest increase in consumer prices since May 2022, as increases in food (2.4 percent versus 5 percent in January), clothing and footwear (5.5 percent versus 5.8 percent), and miscellaneous goods (0.7 percent versus 1 percent) Prices rose more slowly, while services rose faster (0.9% vs. 0.2%). At the same time, the underlying inflation rate was also 1.7%, 0.7 percentage points lower than in January. On a monthly basis, consumer prices did not increase after rising 0.6% in the previous month.

- JP: The Reuters Tankan sentiment index for Japanese manufacturers came in at -3 in March 2023, an improvement from February's -5 reading but a third in a row on concerns that slowing global growth could hurt the country's export-heavy industries. The month remains negative. The negative reading in the monthly survey topped the Bank of Japan's quarterly Tankan report, which showed more companies said business conditions were poor than good. The recent banking crisis has raised risks for external demand, already facing global tightening and a slowdown in China, Japan's largest trading partner. In contrast, a weaker yen has pushed up the cost of imports amid commodity-driven inflation. Materials industries such as steel and textiles and electric motor companies have been hit the hardest. The Reuters Tankan index will rebound to +10 in the next three months.

LOOKING AHEAD:

Today, investors should watch out for the following important data:

- GBP: GfK Consumer Confidence, Retail Sales m/m, Flash Manufacturing PMI, Flash Services PMI, and MPC Member Mann Speaks.

- USD: Core Durable Goods Orders m/m, Durable Goods Orders m/m, Flash Manufacturing PMI, and Flash Services PMI.

- EUR: French Flash Manufacturing PMI, French Flash Services PMI, German Flash Manufacturing PMI, German Flash Services PMI, Flash Manufacturing PMI, Flash Services PMI, German Buba President Nagel Speaks, Euro Summit, and Belgian NBB Business Climate.

- AUD: Flash Manufacturing PMI and Flash Services PMI.

- JPY: National Core CPI y/y, and Flash Manufacturing PMI.

- CAD: Core Retail Sales m/m, and Retail Sales m/m.

KEY EQUITY & BOND MARKET DRIVERS:

Кey factors in the stock and bond market are currently:

- US: The average rate on a 30-year fixed mortgage fell to 6.42% as of March 23, 2023, from 6.60% the week before, according to a survey of lenders by mortgage giant Freddie Mac. It was the biggest weekly drop since mid-January. The average rate on a 15-year fixed-rate mortgage was 5.68%, down from 5.90% last week. “Mortgage rates have continued to slide over the past two weeks as concerns in financial markets have come to the fore,” said Sam Khater, chief economist at Freddie Mac. "However, the news is more positive on the homebuyer side as homebuying demand improves and home prices stabilize. If mortgage rates continue to slide in the coming weeks, they should continue to rebound in the first few weeks of the spring home-buying season."

- UK: U.K. 10-year gilt yields fell to 3.43%, tracking lower in regional peers, as investors digested the latest monetary policy decision. As expected, the Bank of England raised the bank rate by 25 basis points to 4.25% and said further hikes might be necessary if there is evidence of more persistent pressure. In February, UK inflation unexpectedly rose for the first time in four months. Before the CPI report, investors increasingly believed the central bank would soon pause in rate hikes. Meanwhile, the Fed's tone was seen as more dovish on a Wednesday, with the central bank raising interest rates by another 25 basis points, which meant only one more hike this year.

- US: U.S. stock futures were higher on Thursday, with the Dow Jones futures contract up nearly 50 points, the S&P 500 up 0.5%, and the Nasdaq 100 up more than 1%, recovering from a 1.6% plunge in the previous session. Traders continued to assess the latest monetary policy decision from the Federal Reserve after the central bank raised the Fed funds rate by an expected 25 basis points and said it would raise rates only once this year. Meanwhile, the Fed chair opposed any cuts in 2023 and said the central bank would prolong tightening if needed. Meanwhile, as Treasury Secretary Janet Yellen told Congress she was not considering or discussing a blanket insurance or deposit guarantee, bank stocks were in focus.

- EU: European government bond yields fell on Thursday, with the benchmark 10-year yield down about seven basis points at 2.26% after hitting a one-week high in the previous session, as investors digested the latest monetary policy decision and tried to assess further The impact of rate hikes on the economy and the global financial system, following the recent turmoil in the banking sector. As expected, the Fed raised the Fed funds rate by 25 basis points but said it would raise rates only once this year. Meanwhile, central banks in Switzerland and Norway raised rates again. The Bank of England is also expected to continue tightening monetary policy. Last week, the ECB announced a 50 basis point hike in borrowing costs. As a result, key 10-year bond yields in France, Italy, and Spain fell nearly seven basis points to 2.78%, 4.12%, and 3.3%, respectively.

- TW: On March 23, 2023, Taiwan's central bank raised its key rediscount rate by 12.5 basis points to 1.875%, surprising most market participants who had expected no change in borrowing costs, reflecting concerns about inflation. worry. With interest rates now at their highest level since 2015, policymakers said they would continue to focus on the cumulative effects of monetary tightening, the spillover effects of monetary policy in major economies, the likely impact of the recent US and European banking crises, and how these factors might affect Domestic economic and financial implications. Meanwhile, the central bank cut its GDP growth forecast for this year to 2.21 percent from 2.53 percent in December. It also raised its annual inflation forecast to 2.09 percent from 1.88 percent.

- UK: The Bank of England is expected to raise its key bank rate by 25 basis points to 4.25% at its March 2023 meeting, pushing borrowing costs to fresh 2008 highs to counter the still-double-digit inflation that unexpectedly accelerated last month. High inflation while ensuring financial stability. Britain's annual inflation rate increased to 10.4% last month from 10.1%, the first increase in four months. Before the announcement of CPI yesterday, investors were quite optimistic about raising interest rates by 25 basis points or stopping interest rate hikes. The March hike would mark the 11th in a row, with investors expecting summer rates to peak at 4.5%, implying at least one or two more quarter-point increases in borrowing costs. The Bank of England voted 7-2 to raise interest rates by 50 basis points to 4% at its February meeting, pushing borrowing costs to their highest level since late 2008.

- SA: South Africa's 10-year government bond yield fell further to a three-month low of 9.950%, following lower Treasury yields as investors weighed the Federal Reserve's policy outlook. Fed Chairman Jerome Powell reaffirmed his commitment to cut inflation to the official 2% target but suggested a pause in interest rate hikes due to the recent turmoil in financial markets. Domestically, the South African Reserve Bank is expected to raise its key policy rate for the last time this cycle by 25 basis points on March 30, continuing its battle against sticky inflation while supporting the battered economy.

LEADING MARKET SECTORS:

- Strong sectors: Communication Services, Information Technology.

- Weak sectors: Energy, Utilities, Financials, Real Estate, Consumer Staples.

TOP CURRENCY & COMMODITIES MARKET DRIVERS:

Кey factors in the currency and commodities market are currently:

- GBP: Sterling held above the $1.23 level in late March, near its strongest since June 2022. Earlier, the Bank of England raised its key bank rate by 25 basis points to 4.25%, which was largely expected and left the door open for further rate hikes if inflation persists. The move lifted borrowing costs to their highest level since 2008, as the central bank stressed that it was after price stability rather than short-term volatility at the Bank of England. The decision came as the latest data showed that UK inflation rose to 10.4% in February, beating expectations for 9.9% and accelerating unexpectedly from 10.1% the previous month. Meanwhile, the pound was also supported by pressure on the dollar amid the dovish tone of the Fed's latest meeting. However, the dollar also weakened amid ongoing uncertainty over the health of U.S. banks after Treasury Secretary Janet Yellen said the government would not protect all deposits in the banking system without reservation.

- CNY: The offshore yuan rose above 6.83 against the dollar, its highest level in five weeks. The Federal Reserve announced a widely expected 25 basis point rate hike and signaled that its tightening policy might end. Still, traders remained cautious as Fed Chair Jerome Powell said officials would not cut rates this year and were prepared to raise rates higher than expected if needed. At the same time, U.S. Treasury Secretary Janet Yeh Lun's latest comments have reignited fears of a banking crisis. In addition, the yuan has been pressured recently by the prospect of rising liquidity after the People's Bank of China announced its first surprise cut to the reserve requirement ratio for banks this year to help the economy recover. The central bank also kept key lending rates steady in its March rate fixes, keeping the prime rate for one-year loans at 3.65 percent and the five-year lending rate at 4.3 percent.

- USD: The U.S. dollar index fell to 102 on Thursday, remaining under pressure near seven-week lows, as the Fed announced a widely expected 25 basis point rate hike but backed away from talk of a need for "continued rate hikes" and signaled it would increase only One more rate. Still, Fed Chairman Jerome Powell said officials would not cut rates this year and were prepared to raise rates higher than expected if needed. Meanwhile, Treasury Secretary Janet Yellen told lawmakers the U.S. government is not considering "blanket insurance" for bank deposits, reigniting fears of a banking crisis. Investors now look ahead to Thursday's U.S. weekly jobless claims and new home sales data. In addition, the Bank of England was expected to tighten policy further on Thursday after UK inflation data topped expectations.

- GLD: Gold prices rallied to as high as $2,000 an ounce on Thursday, the most in a year, as investors continued to digest the March Federal Reserve meeting and the risks to the global banking system. As loosely expected, the US central bank raised its funding rate by 25 basis points but adopted a dovish tone in its policy report and summary of economic projections. The FOMC forecast a quarter-point increase remaining in its hike campaign, in line with its December estimate, as heightened turbulence in the US financial system narrowed the Fed's scope to respond to higher inflation forecasts and lower unemployment. Gold is sensitive to the rating outlook as lower interest rates reduce the opportunity cost of holding unprofitable bullion.

- IRN: Prices for iron ore cargoes with an iron ore content of 63.5% for delivery to Tianjin fell below USD 124 per ton, the lowest in more than a month, driven by weaker demand from steel producers and increased speculative price controls. Reports indicate that China's top producer will reduce its domestic steel production by 2.5% in 2023, marking the third consecutive annual decline. Immediate bidding activity is also expected to remain subdued as pollution regulations forced major steelmaking centers Tangshan and Handan to reduce capacity. Meanwhile, China's National Development and Reform Commission has issued further warnings against speculative increases in iron ore prices, saying it will crack down on false information by producers and hoarding by traders. Meanwhile, efforts to shore up infrastructure and construction have limited the decline.

- SLV: Silver futures hit $23 an ounce in late March, holding close to levels last seen in early February, but underperforming gold's rally as investors priced a flight to metals precious versus expectations of weak demand for silver as an industrial component. Despite the Federal Reserve's dovish tone at its March meeting, Chairman Jerome Powell said the central bank does not expect any rate cuts this year, dashing any hopes of lower borrowing costs. Higher interest rates drive demand for silver as an input for goods with high electrical conduction needs, as reflected in falling solar panel stock prices. However, a flight to precious metals continued after US Treasury Secretary Yellen denied that she considered the government protecting all deposits in the US banking system.

- TRY: The Turkish lira was stable at a record low of 19 per USD in late March after the Turkish central bank kept its key interest rate unchanged at 8.5%, as expected. The move followed a 50 basis point cut in interest rates in February as the TCMB returned to cutting interest rates to ease financial conditions further and stimulate supply chains in response to Turkey's devastating earthquake. The central bank has cut its key rate by 10.5 percentage points since September 2021, triggering a crisis for the lira, skyrocketing inflation, and a vastly out-of-balance current account. Inflation in Turkey soared to 86% in October before falling back to 55% in February as the lira plunged 56% since the start of the bank's cut cycle and exacerbated rising energy costs Turkey must import.

- CHF: The Swiss franc strengthened to 0.91 per USD, approaching last week's robust levels, after the Swiss National Bank went ahead with a 50 basis point hike in borrowing costs as expected, citing a renewed increase in pressure inflationary and discounting the recent turmoil in the banking sector and the takeover of Credit Suisse. The central bank noted that the measures announced by the federal government, FINMA, and the SNB had ended the crisis. Furthermore, it reiterated that it provides substantial liquidity relief in Swiss francs and foreign currencies, secured by guarantees and subject to interest. As a result, inflation in Switzerland unexpectedly rose to 3.4% in February, beating market expectations by 3.1% and SNB forecasts by 3%.

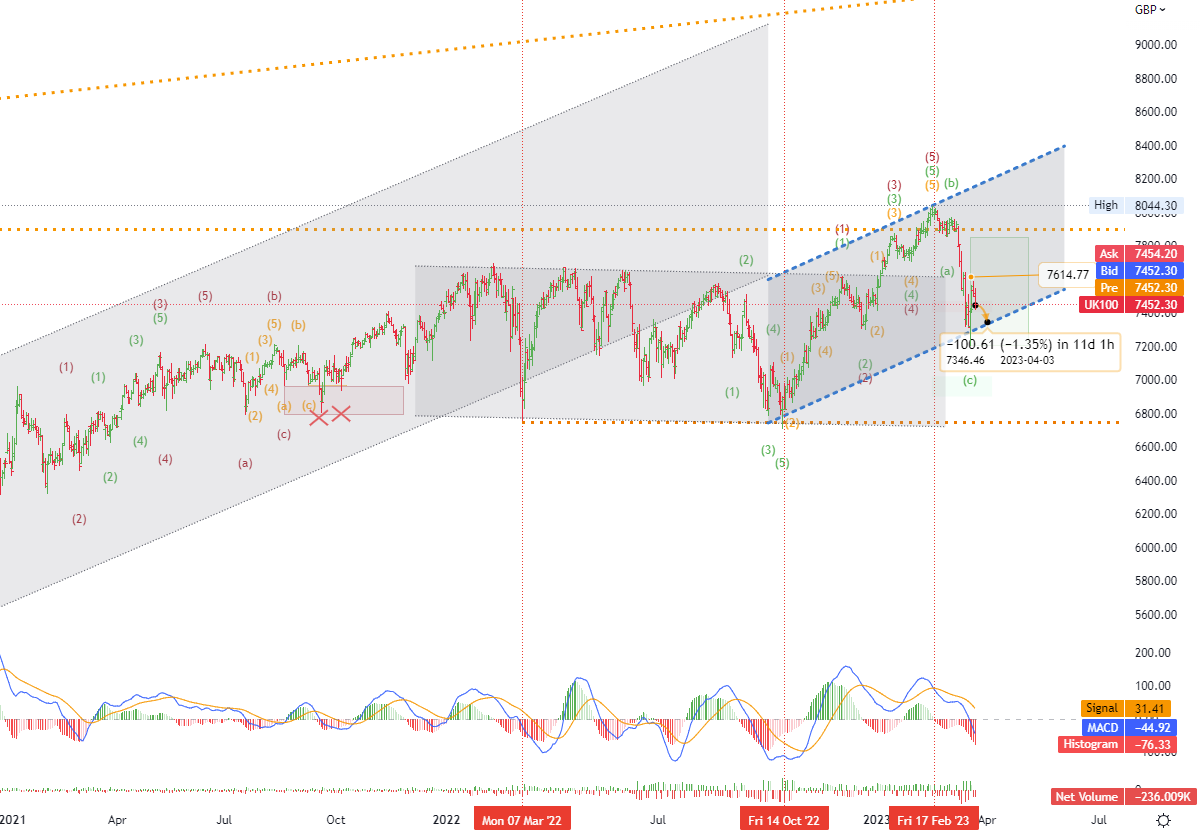

CHART OF THE DAY:

The UK FTSE 100 fell 0.85% to close at 7,500 on Thursday, underperforming its European peers after the Bank of England raised its key bank rate by 25 basis points as expected and highlighted its willingness to keep growing borrowing costs if necessary. The decision was passed by a 7-2 majority, against market expectations of 6-3, with John Cunliffe unexpectedly voting for a rate hike. The move is in line with rate hikes this month by the European Central Bank and the Swiss National Bank, which have opted to prioritize tackling a surge in inflation despite recent volatility. Lenders were among the biggest losers on the session, with HSBC down nearly 3 percent and Barclays down 2 percent.

Long-term Channels Trading Strategy: - UK FTSE 100 index -; Chart with time-frame (D1); The primary Resistance with a potential (consolidation area) is around ~ ( 7614 ), and the primary Support with a potential (target area) is around ~ ( 7346 ). Therefore, the next most probable price movement is a (down / sideways) trend. *see details on the chart.

Start trading in four simple steps

1. Register

Open your live trading account

2. Verify

Upload your documents to verify your account

3. Fund

Deposit funds directly into your account

4. Trade

Start trading and choose from 130+ instruments

Demo account

The Blue Suisse Trading Account with virtual funds in a risk-free environment

Demo accountLive account

The Blue Suisse Trading Account in our transparent live model environment

Open an Account- Trading Account types Trading conditions Trading hours Transparency Market Information

- Products Currencies Commodities Indices Stocks

- Tools MetaTrader 4 / 5 Mobile CRM, MAM and DSP

- Education Currency Trading for Beginners How to improve your trading CFD Trading

- Partnerships Asset- and Moneymanager Tied agent White labels FIX API

- Company About us Regulatory Our philosophy Careers FAQs Contact us