Economic slowdown worries are still in play, manifesting in falling oil and copper prices; European gas prices edge down

GLOBAL CAPITAL MARKETS OVERVIEW:

The blue-chip Dow and S&P 500 lost some momentum at the open on Friday but ended the session up about 0.6% each, as much of the optimism over positive earnings was offset by lingering fears of a Fed-fueled recession. However, the tech-heavy Nasdaq underperformed, closing near flat as higher U.S. Treasury yields weighed on high-growth and other tech stocks. Hawkish comments from several Fed policymakers dashed hopes for a pause in the central bank's tightening cycle. Of these, St. Louis Fed President James Bullard was the most vocal, warning that tightening conditions would have little impact on inflation. Chip toolmaker Applied Materials rose nearly 2 percent on the company front after forecasting first-quarter revenue that topped analysts estimates. The Dow was largely flat for the week, while the S&P 500 lost 0.7 percent and the Nasdaq lost 1.2 percent. Canada's S&P/TSX Composite closed at 19,980 on Friday, up 0.5%, snapping a two-session losing streak, as gains in technology companies and banks offset sharp losses in energy producers. At the same time, investors Digested a batch of macroeconomic data. Canadian industrial producer prices rose 2.4% month-on-month in October, beating expectations for a 0.4% increase and reinforcing recent hawkish comments from central bank governor Steve Macklem. Lenders led gains in Toronto, with TD Bank, BMO, and RBC up more than 0.5 percent. On the other hand, heavy energy producers were down nearly 3% on average as crude oil prices fell sharply late in the last two sessions. The TSX closed down 0.7% last week. The domestic DAX 40 rose more than 1 percent to close around 14,430, up 1 percent for the week, its seventh straight week of gains, driven by increases in utilities and energy stocks. Investors tracked several economic data and earnings results for clues about the eurozone economy and the path of interest rates from the European Central Bank. President Christine Lagarde said the central bank will continue to raise interest rates and may even need to limit growth to keep inflation in check. At the same time, the European Central Bank announced that banks would repay the ECB's multi-year loan of 296 billion euros next week, which is lower than the market expectation of 500 billion euros, which is the first voluntary repayment window of the ECB TLTRO. The regional STOXX 600 index was up about 1% at around 430, boosted by utilities, real estate gains, and financials. The European benchmark rose 0.1% for the week, it's fifth straight weekly gain. The Italy FTSE MIB index closed at 24,620 on Friday, up 1%, erasing losses from the previous two sessions, and was up 0.8% for the week as investors continued to assess the outlook for monetary tightening by major central banks. Traders also digested reports that Giorgia Meloni's cabinet would set 30 billion euros in extra spending in the new government's first budget law, expected to provide input into further measures to shield businesses and households from soaring energy prices. The report strongly favored utility providers trading in Milan, with Enel up 3 percent and Italgas and Terna up 2 percent each. The heavyweight financial sector also closed in the green, with Generali up 1.5 percent to lead the gains. The France CAC 40 index rose about 1 percent to close at 6,644.46 on Friday after falling for two consecutive sessions, in line with regional peers. Investors continued to monitor economic data while also trying to assess the outlook for interest rates in the months ahead. Meanwhile, the European Central Bank announced the largest withdrawal of cash in history from the eurozone banking system as part of efforts to curb inflation. Among the top gainers, Teleperformance rose 3.7 percent after it said it would exit an "extremely spectacular" part of its social media content moderation business. Schneider Electric (+2.8%) was not far behind after Erste Group raised its recommendation from "hold" to "buy." In contrast, real estate group Unibail Rodamco led losses of 1.2% after Goldman Sachs downgraded its stock, switching from "neutral" to "sell," with a 12-month price target lowered from 44 euros to 39 euros. The CAC 40 closed the week up about 0.8%. London shares snapped a three-day losing streak on Friday, with the benchmark FTSE 100 up about 0.5% at around 7,400, adding almost 1% for the week, driven by gains in property, consumer discretionary, and utilities. The latest data showed that retail sales tripled in October, although still on a downward trend. Investors also continued to digest the fall announcement on Thursday. Treasurer Jeremy Hunt proposes around £30bn in spending cuts and £25bn in tax increases, including freezing the income tax threshold for six years and reducing the top income tax rate to £125,000. Meanwhile, the UK economy is expected to shrink by 1.4% this year and not return to pre-pandemic levels until the end of 2024. The MOEX Russia index fell 0.4 percent to close at 2,204 on Friday, pressured by commodity-backed stocks, down 0.5 percent for the week. The sub-index for oil and gas producers fell 2.2 percent for the week, sharply underperforming the broader benchmark, as investors continued to assess the worrisome outlook for Russia's energy sector ahead of the EU oil embargo starting in December. In addition to halting seaborne oil exports to EU countries, companies will also be banned from using Western tankers and insurance services for shipments to Asia. Before the embargo, Russia took in $118 million in revenue from seaborne oil exports in the week ended Nov. 11, the lowest since the start of the year, data compiled by Bloomberg showed. Meanwhile, the European Union announced it would cap gas prices by the end of the month, further putting pressure on state-owned energy giants. Tatneft and Novatek were both down 1 percent during the session. Hong Kong shares fell 59.71 points, or 0.33 percent, to close at 17,985.95 on Friday, after strong gains in early trade, supported by news that China's video game regulator issued distribution licenses to 70 online games. Market sentiment turned pessimistic in the afternoon, with U.S. stock futures falling after Wall Street pulled back on Thursday on fears of aggressive tightening by the Federal Reserve. Meanwhile, the recent worsening COVID-19 outbreak in China has added downward pressure on near-term economic growth, Goldman Sachs said in a report. China Overseas Land led the decline (-4%), followed by CITIC (-3%), Wuxi Biologics (-2.3%), and Tencent (-1.1%). In contrast, Alibaba Group rose 2.1% after unveiling a new buyback program and reporting earnings that topped expectations. Still, the Hang Seng rose 3.8 percent for the week, it's third weekly gain, buoyed by policy adjustments over the outbreak and measures to stabilize the property market. The Baltic Dry index, which measures the cost of shipping goods globally, fell about 3.2% to 1,189 points on Friday, falling for the seventh straight day to its lowest level since Sept. 8. The Capesize index, which tracks cargoes of about 150,000 tonnes of iron ore and coal, fell for a sixth straight session, down about 5.6% to 1,122 points; the Panamax index, which tracks cargoes of about 60,000 to 70,000 tonnes of coal and grains, fell for a second straight day, down 3.4 % to a ten-week low of 1,594. Meanwhile, the Supramax index fell for the 20th consecutive session to 1,170 points. The Baltic Dry index fell 12.3 percent in the third week of November, its fifth weekly decline in six weeks. Brazil's Ibovespa index traded higher above 111,470 on Friday after falling for a second straight day to its lowest level since September on concerns over the incoming government's plan to cap spending. Meanwhile, on Thursday, Vice President-elect Geraldo Alckmin said that Brazil's incoming government would be fiscally responsible, promising a budget surplus and reduction in public debt to quell market unrest over a proposed welfare plan. Congressional leadership, reportedly People Artur Lira and Rodrigo Pacheco, debated the possibility of a proposed amendment to the Transitional Constitutional Amendment (PEC) yesterday. Traders also expressed interest in This is welcome. Almost all sectors were up, led by real estate companies (+4.9%). Elsewhere, investors continued to assess the outlook for the Federal Reserve's monetary policy after hawkish comments from several officials. Ibovespa was on track for a 0.7% loss for the week. Hong Kong shares fell 59.71 points, or 0.33 percent, to close at 17,985.95 on Friday, following strong gains in early trade on news that China's video game regulator issued publishing licenses to 70 online games. Market sentiment turned pessimistic in the afternoon, with U.S. stock futures falling after Wall Street corrected on Thursday on fears the Federal Reserve would tighten policy sharply. Meanwhile, Goldman Sachs said in a note that China's recent worsening COVID situation had added downward pressure on near-term growth. China Overseas led the decline (-4%), followed by CITIC (-3%), WuXi Biologics (-2.3%), and Tencent (-1.1%). In contrast, Alibaba Group Holding rose 2.1 percent after unveiling a new buyback program and reporting earnings that topped expectations. Even so, the Hang Seng Index rose 3.8% for the week. New Zealand shares rose 86.09 points, or 0.76%, to close at a near four-week high of 11,380.61 on Friday after trading lower in early trade, up 0.6% for the week, the fourth straight weekly gain. Traders turned their attention to next week's central bank meeting, with the market divided on whether a 50 or 75 basis point rate hike is imminent. Since October 2021, the Reserve Bank of New Zealand has maintained its hawkish stance to cool inflation at a high level for more than 30 years. Meanwhile, Prime Minister Jacinda Ardern is scheduled to meet President Xi Jinping on the sidelines of Bangkok's Asia-Pacific Economic Cooperation (APEC) summit. This will be their first face-to-face meeting since 2019. Utilities, health technology, and non-energy minerals largely led to gains. Mercury NZ led the way, up 4.1 percent. On Friday, the Nikkei 225 fell 0.11% to close at 27,900. In comparison, the broader Topix rose 0.04% to 1,967 amid cautious sentiment after Fed officials said they were prepared to tighten policy further to curb inflation. dominate market sentiment. Japanese stocks were also volatile after Bank of Japan Governor Haruhiko Kuroda emphasized the need to maintain an ultra-loose monetary policy to support the economy after data showed the country's annual core consumer prices surged to a 40-year high in October. Index heavyweights such as SoftBank Group (-3.9%), Tokyo Electron (-1%), Mitsubishi UFJ (-0.6%), NYK Line (-2.4%), and Recruit Holdings (-3.2%) posted notable losses. Meanwhile, barely higher companies included Nintendo (0.7%), Sumitomo Mitsui (0.5%), and Sony Group (0.2%). The Shanghai Composite and Shenzhen Composite Index struggled on Friday1amid growing fears of a resurgence of the coronavirus in China, dashing hopes for a reopening and further dimming the economic outlook. Investors also heeded warnings from the People's Bank of China that inflation could accelerate in anticipation of a pick-up in demand, leaving little room for further monetary easing. The benchmark index remained on track to end the week marginally higher, recently buoyed by policy shifts involving China's property sector and approach to Covid, as well as positive updates from President Xi Jinping's interactions with other world leaders. Growth in healthcare, technology, and new energy stocks mostly rose, with strong gains in Shijiazhuang Yilin (3.4%), China Great Wall Technology (8%), and Modern New Energy (2.1%). at the same time. The Australian S&P/ASX 200 rose 0.23% to 7,152 on Friday. Still, it ended the week little changed throughout the period amid concerns over further tightening by the Federal Reserve, China's Covid-related uncertainty, and plunging commodity prices. Get washed up. Domestically, the Reserve Bank of Australia continued to signal a data-driven monetary policy after slowing the rate hikes, despite solid economic data supporting further tightening. Financial firms led gains on Friday, with the "big four" banks up between 0.2 percent and 1.8 percent. Meanwhile, technology, energy, and lithium stocks lagged behind the broader market. In corporate news, OZ Minerals surged 4% after backing BHP Billiton Group Inc's A$9.6 billion bid increase as the latter plans to boost its copper and nickel portfolio.

REVIEWING ECONOMIC DATA:

Looking at the last economic data:

- US: U.S. Existing Home Sales declined 5.9% in October 2022 to a seasonally adjusted annual rate of 4.43 million units, the lowest level since December 2011, barring a brief dip early in the pandemic, when the consensus forecast was 438 million sets. It was the ninth month of sales declines as home prices continued to rise and 30-year fixed mortgage rates hit a 20-year high, forcing many buyers out of the market. "As mortgage rates climbed, more potential homebuyers were excluded from mortgage eligibility in October," said Yun, chief economist at NAR. Big.". Meanwhile, the total housing inventory fell 0.8% to 1.22 million units. The median existing-home price for all housing types was $379,100, up 6.6 percent from October 2021. Properties typically stay on the market for 21 days in October, compared to 19 days in September.

- US: In November 2022, the Kansas City Fed's manufacturing production index came in at -10, the second-lowest number since May 2020, down only from -22 the previous month. The slowdown in factory growth in the period was due to lower activity in primary metals, plastic and rubber products, chemicals, furniture, and metal manufacturing. Most month-on-month indices fell, with the delivery time index now at its lowest level on record. Meanwhile, the index grew at its slowest pace since March 2021, hit by a drop in new orders and a backlog of orders. On the other hand, the future composite index fell to 0 from -1 in the previous month, as expectations for production rebounded (6 vs. -1 in October).

- CA: Foreign investors reduced their exposure to Canadian securities by a net C$22.3 billion in September 2022, the largest amount since December 2018 and a change from net acquisitions of C$26.2 billion in the previous month. Nonresidents sold a net of C$11.1 billion in debt securities through federal government money market instruments (C$9.2 billion) and federal government bonds (C$5.8 billion). Meanwhile, foreign investors sold a net C$8.9 billion in Canadian equities, tracking a 4.6 percent drop in the benchmark S&P/TSX Composite index over the same period. On the other hand, Canadian residents made net purchases of foreign securities of C$9.6 billion, with net assets of bonds ($12.9 billion) offsetting equity sales ($1.4 billion).

- CA: In October 2022, the Canadian raw material price index rose by 1.1% month-on-month to 145.6 index points, rebounding from a downwardly revised 3.1% decline in September, mainly due to higher prices of crude oil energy products (2%). Conventional crude oil prices rose 5.1% on expectations of lower crude production. At the same time, rapeseed prices also increased (+7.7%), but the costs of logs, pulp, natural rubber, and other forestry products fell (-9.5%). As a result, raw material prices rose 9% year-on-year.

- SW: In October 2022, Sweden's unemployment rate dropped from 7.6% in the same month last year to 7.1%, the number of unemployed people decreased by 22,000 to 396,000, and the number of employed people increased by 110,000 to 5.19 million. The labor force participation rate rose 1.0 percentage points to 74.1%, and the employment rate rose 1.1 percentage points to 68.8%. On a seasonally adjusted basis, the unemployment rate was 7.3% in October.

- BG: Bulgaria's current account deficit widened to EUR 457.9 million in September 2022 from EUR 31.5 million a year earlier. The goods deficit increased to 632.4 million euros from 191.6 million euros in September 2021; the primary income gap has risen from 322.8 million euros to 362.1 million euros; the secondary income surplus narrowed from 142.5 to 106.7 million euros. At the same time, the services surplus increased from EUR 340.3 million to EUR 429.9 million.

- SW: Swiss industrial production rose by 5.2% year-on-year in the third quarter of 2022, slightly higher than the downwardly revised 5% growth in the previous three months, due to a smaller contraction in mining and quarrying (-2.1% vs. -12%) and Electricity supply (-6.6% vs. -9.8%). Meanwhile, manufacturing output growth held steady at 6.3%. As a result, industrial production rose 0.5% in the third quarter on a seasonally adjusted quarterly basis, after a downwardly revised 0.1% decline in the previous quarter.

- NR: Norway's economy expanded by 1.5% quarter-on-quarter in the third quarter of 2022, the fastest pace in four quarters, following an upwardly revised 1.3% growth in the second quarter. Oil activity and marine transport rose 7.6%, well above the 1.5% rise in the second quarter. Elsewhere, gross fixed capital formation rose 0.4%, double the 0.2% increase in the second quarter, and investment in extractive-related services rose 15.5%. As a result, exports grew faster (5.7% vs. 2.8%), while imports slowed (2.9% vs. 5.7%). Meanwhile, mainland GDP, which excludes the largely oil-based offshore sector, rose 0.8% in the second quarter, beating market expectations for a 0.4% increase, driven by services and wholesale trade in particular. 1.2% .

- JP: Japan's core consumer price index (excluding fresh food but including fuel costs) rose 3.6% YoY in October 2022, the fastest pace since February 1982, driven by high global commodity prices and weaker yen import costs. The October data followed a 3% increase in September and was higher than analysts' expectations for a 3.5% increase. Core inflation also topped the central bank's 2 percent target for the seventh straight month, posing a challenge to the Bank of Japan, which is under increasing pressure to adjust its ultra-low interest rate policy. However, Bank of Japan Governor Haruhiko Kuroda recently said the central bank would stick to monetary easing to support the economy, citing the desire for sustainable inflation alongside wage growth.

- JP: Japan's annual inflation rate climbed to 3.7% in October 2022 from 3.0% a month earlier, the highest level since January 1991, due to high prices for imported raw materials and persistent yen weakness. Upward pressure came from all components: food (6.2% vs. 4.2% in September); housing (1.1% vs. 0.6%); fuel, light, and water bills (14.6% vs. 14.9%), mostly electricity (10.9% vs. %) and natural gas (20.0% vs. 19.4%); transportation and communications (2.0% vs. 0.6%); medical care (0.2% vs. -0.5%), furniture and household appliances (6.9% vs. 6.6%); culture and entertainment (0.9 % % vs. 2.2%), and miscellaneous (0.8% vs. 1.2%). As a result, core consumer prices rose 3.6% year-on-year, the most since February 1982, beating expectations for a 3.5% increase and topping the Bank of Japan's 2% target for the seventh straight month. On a monthly basis, consumer prices rose by 0.

- PR: Annual producer price inflation in Portugal fell to 16.2% in October 2022 from an upwardly revised 19.7% in the previous month, marking the fourth consecutive year of decline in inflation and the lowest level in a year. Prices fell in energy (21.7% vs. 34.9% in September), intermediate goods (16.7% vs. 18.8%), and capital goods (4.4% vs. 4.7%). On the other hand, consumer goods prices rose faster (15.7% vs. 15.3%). As a result, producer prices fell 0.4% on a monthly basis, compared with a revised 0.1% decline in September.

- ML: Malta's annual inflation rate hit a record high of 7.4% in October 2022, unchanged from the previous month. Upward pressure continued to come mainly from prices of food and non-alcoholic beverages (14.3% and 11.9%, respectively, in September) and housing and utilities (10.2% and 9.6%). Meanwhile, prices slowed for transportation (4.1% vs. 7.7%); entertainment and culture (6.6% vs. 7.7%); restaurants and hotels (6.4% vs. 6.4%), and miscellaneous goods and services (4.6% vs. 4.8%). As a result, on a monthly basis, the CPI fell by 0.6%, the same as the previous month's.

- CY: Cyprus's annual coordinated inflation rate fell for the third consecutive month in October 2022, falling to 8.6% from 9% in the previous month. The main reasons for the price slowdown were housing and utilities (22.2% vs. 28.7%), transportation (11.9% vs. 11.1%), and restaurants and hotels (9.1% vs. 10.7%). On the other hand, the price growth of clothing and footwear decreased (-0.2% vs. 0%), while the cost of food and non-alcoholic beverages increased faster (12.6% vs. 9.1%). As a result, on a monthly basis, HICP rose 0.5% after falling 1% in the previous month.

- EU: Consumer price inflation in the euro area was revised down slightly to 10.6% in October 2022 from an initial estimate of 10.7%. Still, the rate remains at an all-time high and well above the ECB's 2.0 percent target amid soaring energy prices and a weak euro. The data put pressure on European Central Bank policymakers to keep raising interest rates despite signs of an economic downturn. The main upward pressure came from energy (41.5% vs. 40.7% in September), followed by food, alcohol, and tobacco (11.1% vs. 11.8%), services (4.3%, same as September) and non-energy industrial goods (6.1%) percentage vs. 5.5%). As a result, annual core inflation, which excludes volatile energy, food, alcohol, and tobacco prices, climbed to 5.0% in October, the highest on record.

LOOKING AHEAD:

A week ahead:

- In the US, investors will be closely watching the release of the FOMC minutes, the University of Michigan's consumer sentiment index, durable goods orders, and new home sales. Additionally, November PMI flash data from major advanced economies, including the US, Japan, Germany, France, and Australia, will be in focus. In the end, the central banks of China, New Zealand, Sweden, South Korea, Turkey, Malaysia, and South Africa will determine the direction of monetary policy.

Today, investors will receive the following:

- EUR: German PPI m/m and German Buba President Nagel Speaks.

- NZD: Credit Card Spending y/y and Trade Balance.

- GBP: MPC Member Cunliffe Speaks.

- AUD: CB Leading Index m/m.

KEY EQUITY & BOND MARKET DRIVERS:

- GE: German 10-year government bond yields held above 2% after the ECB announced that eurozone banks would repay 296 billion euros of multi-year ECB loans next week, below market expectations of 500 billion euros, which is the ECB TLTRO First voluntary repayment window since terms changed in October. Meanwhile, ECB President Christine Lagarde said the central bank would keep raising rates as eurozone inflation hit a record high of 10.6% in October, well above its 2% target. However, the recession is seen as unlikely to ease Price pressure is enough for the ECB to hit the brakes. Investors are now divided on pricing in December rate hikes of 50 and 75 basis points and expect to reduce bond holdings starting in the first half of 2023. Last week, German yields were on track to post a second straight weekly loss for the first time since July as major central banks, including the Federal Reserve, look to take a more dovish approach.

- IN: India's 10-year government bond yield was above 7.3%, up slightly from a near two-month low of 7.26% hit on Nov. 15, tracking a rise in global bond yields as major central banks signaled that interest rates would continue to rise. Domestically, money markets expect the RBI to raise its key rate by 50 basis points at its December meeting, adding to the 180 basis points hike it has since tightening began in May, in a bid to rein in stubborn inflation. In addition, the latest data showed retail prices rose 6.8% for the year in October, marking the tenth month that inflation has exceeded the central bank's 6% ceiling target. Still, the rebound in yields was capped by reports that major government spending should be below the budgeted amount for the current fiscal for the first time since 2019/20, underscoring the government's aim to rein in the fiscal deficit and reduce credit risk on India's debt .

- CA: The yield on Canada's 10-year government bond climbed above 3.1%, rebounding from a more than one-month low of about 3% earlier last week, as the prospect of further rate hikes dented investor appetite for government debt. Federal Reserve policymakers stepped up their hawkish tone, saying inflation remained too high while warning that it was too early to consider a pause. Domestically, the Bank of Canada surprised markets last month by raising its benchmark interest rate by a lower-than-expected 50 basis points as it assessed the growth outlook. Nonetheless, the central bank is expected to maintain its tightening cycle until a final level of around 4.25%.

- US: Government bond yields worldwide increased after major central banks flagged a longer path to monetary tightening and warned it was too soon to consider a pause. Fed policymakers have little choice but to ramp up hawkish rhetoric, with inflation only starting to ease after reaching its highest level in decades and signs of a resilient U.S. economy, a tight job market, and rising U.S. consumers. Accelerate. In Europe, European Central Bank President Christine Lagarde warned that the central bank will continue to raise interest rates and may even need to limit growth to keep inflation in check. The U.S. 10-year Treasury yield, the benchmark for global borrowing costs, rebounded sharply to 3.8% from a more than one-month low of 3.7% earlier in the week. Europe's benchmark German 10-year bond yield jumped above 2%.

- UK: UK 10-year government bond yields rose to 3.3% from a two-month low of 3.09% hit on Thursday after Chancellor of the Exchequer Jeremy Hunt announced tax hikes and spending cuts to fix the country. Public finances and restore their economic credibility. Tax changes are widely expected, with key measures including reducing the 45% top income tax threshold to £125,000 and freezing the exemptions and thresholds for income tax, national insurance, and inheritance tax for another two years. In addition, the Budget aims to cut the dividend allowance to £1,000 next year and then £500 in April 2024. The UK is in recession, according to the Office for Budget Responsibility, which expects GDP to contract by 1.4% next year before returning to growth in 2024, but perhaps at a lower peak than the US.

STOCK MARKET SECTORS:

- High: Utilities, Real Estate, Financials, Health Care.

- Low: Energy, Communication Services.

TOP CURRENCY & COMMODITIES MARKET DRIVERS:

- OIL: West Texas Intermediate crude futures fell 4% to around $78 a barrel on Friday, the lowest since Sept. 28, and were on track to end the week down more than 10% as the weak demand outlook outweighed supply concerns. A renewed coronavirus outbreak in China has dashed hopes of reopening and clouded the outlook for demand in the world's largest crude importer. In addition, concerns remain that aggressive monetary tightening by major central banks could tip the global economy into recession, hurting energy demand. Recently, St. Louis Federal Reserve Bank President James Bullard said the federal funds rate could reach a range of 5% to 7%, higher than what the market is currently pricing, as the authorities fight inflation. Still, investors remain wary of a highly uncertain supply outlook heading into winter, with the European Union set to ban Russian crude flows from December. Brent crude futures rose above $90 a barrel on Friday but remained sharply lower for the week as a weak demand outlook outweighed supply concerns. The international oil benchmark has fallen about 6% this week, under pressure from concerns that aggressive monetary policy tightening by major central banks could tip the global economy into recession, hurting energy demand. Notably, St. Louis Fed President James Bullard said the federal funds rate could reach a range of 5% to 7%, higher than the market is currently pricing in, as the authorities crack down on inflation. A resurgence of the coronavirus in China has also dashed hopes of reopening and clouded the outlook for demand in the world's largest crude importer. Still, traders remain wary of a highly uncertain supply outlook heading into winter

- NIC: The nickel market has been volatile again, with the benchmark LME price plunging nearly 20 percent to $25,000 a tonne in the past two sessions after hitting a six-month high of around $30,000 earlier this week. The wild price swings have revived fears of a liquidity crisis for one of the most important industrial commodities. The LME responded by raising initial margins by 28% to $6,100 a tonne from Friday's close and stepping up market surveillance activities. Prices briefly topped the $100,000 mark in early March as China's Tsingshan Holdings bought heavily to hedge its bearish bets on the metal. In addition to the chaotic price action, investors continued to focus on developing China's zero-Covid policy. The reopening of the world's largest consumer of the metal should boost demand while providing some respite for prices. On the supply side, the nickel deficit in 2021 will turn into a surplus in 2022 due to solid production in Indonesia.

- GAS: U.S. natural gas futures fell below $6.20 per million British thermal units on Friday after four sessions of gains but were still up more than 5% for the week as heating demand rises due to cooler weather. On the other hand, the Freeport LNG export plant in Texas may not be able to return to service this month as repair work and efforts to gain regulatory approval to make more gas available for domestic use are still underway. Meanwhile, EIA data showed US utilities added 64 billion cubic feet (bcf) of natural gas to storage in the week ended Nov. 11, in line with expectations. This compares to an increase of 23 bcf in the same week last year and a five-year (2017-2021) average decrease of 5 bcf. Inventories at this time of year are near the five-year average of 3.651 tcf.

- GBP: Sterling rallied to $1.19 on Friday, recovering from a 0.5% loss on Thursday to close at its highest level in three months as investors welcomed the new data and the new budget. Data on Friday showed retail sales rose 0.6% in October, well above expectations for a 0.3% rise. Meanwhile, Chancellor of the Exchequer Jeremy Hunt outlined a £55bn plan of tax hikes and spending cuts in his autumn budget statement aimed at repairing the country's public finances and restoring its economic credibility. Still, the chancellor said Britain was already in recession, with the OBR forecasting the economy would shrink by 1.4% in 2023, compared with a 1.8% growth forecast in the previous outlook published in March. On the monetary policy front, UK money market futures point to the Bank of England raising interest rates to a peak of 4%.

- JPY: Japan's annual core consumer prices soared to a 40-year high of 3.6% in October as high global commodity prices and a weak yen pushed up import costs, with the yen gaining more than 140 per dollar, data showed. The currency strengthened even after Bank of Japan Governor Haruhiko Kuroda emphasized the need to maintain an ultra-loose monetary policy to support the economy after overheating inflation data. Kuroda has also previously said the central bank wants to achieve sustainable inflation alongside wage growth. In addition, the latest data showed that the country's trade deficit widened more than expected in October as soaring import costs outpaced export growth, while its economy contracted unexpectedly in the third quarter.

- GLD: Gold steadied around $1,760 an ounce on Friday but was set to end the week lower as hawkish news from the U.S. Federal Reserve hinted at more rate hikes than the market had expected, pushing down expectations for the central bank's shift to policy. Most notably, St. Louis Fed President James Bullard said the policy rate was not sufficiently restrictive and suggested that it could reach a range of 5% to 7%, above Current pricing in the market. San Francisco Fed President Mary Daly also stressed that a pause in rate hikes was "impossible." At the same time, Kansas City Fed President Esther George said policymakers must be "careful not to stop prematurely" from raising rates. At the same time, gold is widely considered a hedge against inflation and economic uncertainty.

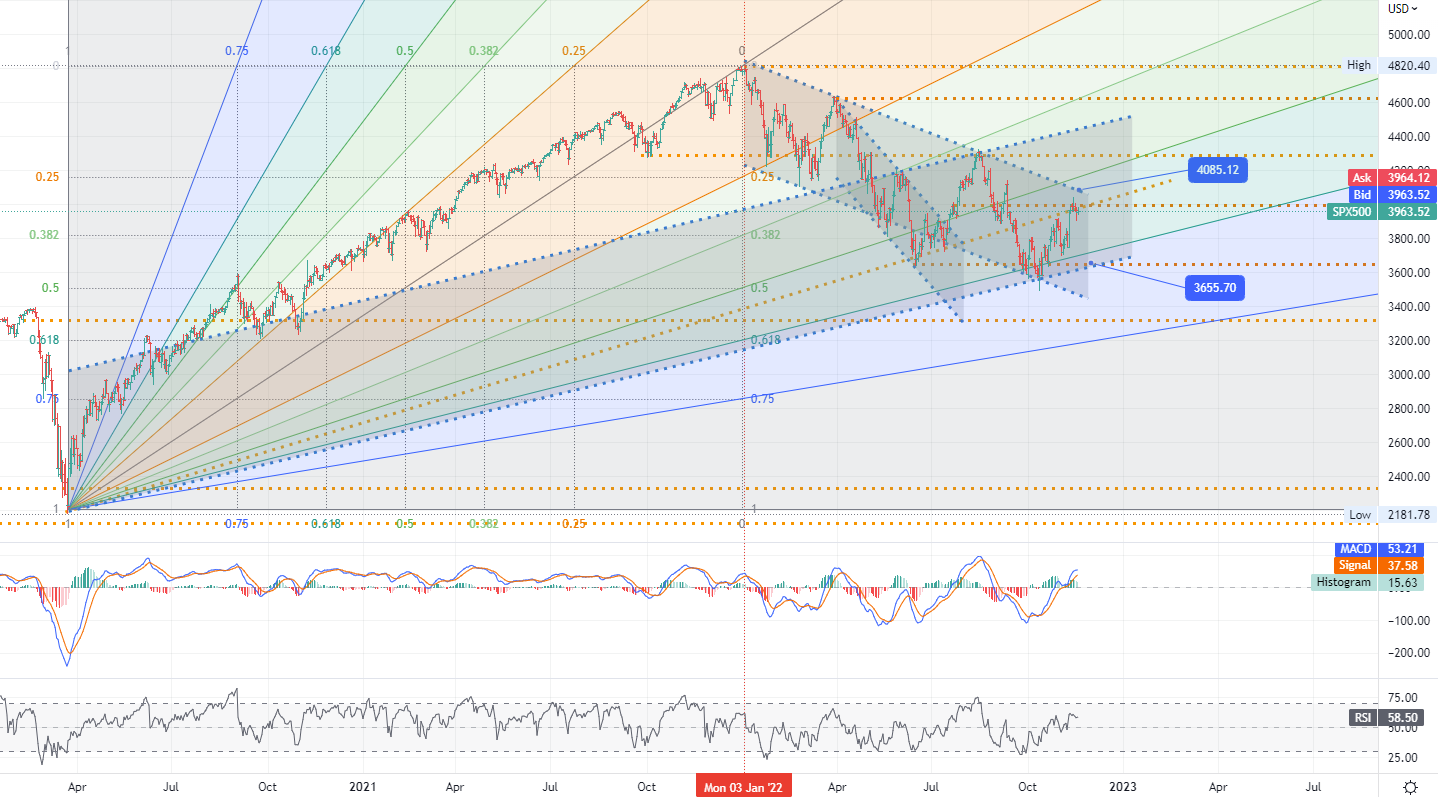

CHART OF THE DAY:

The blue-chip Dow and S&P 500 lost some momentum at the open on Friday but ended the session up about 0.6% each, as much of the optimism over positive earnings was offset by lingering fears of a Fed-fueled recession. However, the tech-heavy Nasdaq underperformed, closing near flat as higher U.S. Treasury yields weighed on high-growth and other tech stocks. Hawkish comments from several Fed policymakers dashed hopes for a pause in the central bank's tightening cycle. Of these, St. Louis Fed President James Bullard was the most vocal, warning that tightening conditions would have little impact on inflation. Chip toolmaker Applied Materials rose nearly 2 percent on the company front after forecasting first-quarter revenue that topped analysts estimates. The Dow was largely flat for the week, while the S&P 500 lost 0.7 percent and the Nasdaq lost 1.2 percent.

- US S&P 500 index - D1, Resistance (short target zone) around ~ 4085, Support around ~ 3655

Start trading in four simple steps

1. Register

Open your live trading account

2. Verify

Upload your documents to verify your account

3. Fund

Deposit funds directly into your account

4. Trade

Start trading and choose from 130+ instruments

Demo account

The Blue Suisse Trading Account with virtual funds in a risk-free environment

Demo accountLive account

The Blue Suisse Trading Account in our transparent live model environment

Open an Account- Trading Account types Trading conditions Trading hours Transparency Market Information

- Products Currencies Commodities Indices Stocks

- Tools MetaTrader 4 / 5 Mobile CRM, MAM and DSP

- Education Currency Trading for Beginners How to improve your trading CFD Trading

- Partnerships Asset- and Moneymanager Tied agent White labels FIX API

- Company About us Regulatory Our philosophy Careers FAQs Contact us