The UK announced a fiscal stimulus plan, financed through issuing more debt at a time of rising interest rates

GLOBAL CAPITAL MARKETS OVERVIEW:

The Dow fell below the key 30,000 mark to close at 29,592, a near two-year high, while the S&P 500 and Nasdaq fell 1.7% and 1.8%, respectively, as the Fed-induced sell-off intensified. The outlook for economic growth has deteriorated, with high inflation hitting Main Street and dampening consumer spending, clouding sentiment. With the central bank projecting rates as high as 4.6% in 2023 and Jerome Powell saying a soft landing or even a mild recession is unlikely, investors are bracing for a prolonged recession. Energy stocks were the biggest losers on the day, down 6.33% as crude prices tumbled. On the corporate front, Costco Wholesale shares fell 4% after the big-box retailer reported lower profit margins in the fourth quarter. Costco's disappointing results added to the gloomy outlook for several companies, including FedEx and Ford. The Dow is down 4% for the week, while the S&P and Nasdaq are down 4.7% and 5.1%, respectively. Canada S&P/TSX Composite fell 2.8% on Friday to end the week at 18,480, or 4.6%, for the third straight session to its lowest level since July, amid a recession sparked by the prospect of aggressive tightening by major central banks Fears led to a sell-off in global equities. Concerns about low demand pushed crude prices to January lows, pushing the Toronto-heavy energy sector down 6.5 percent. A broad sell-off in gold and other gold investments also lowered mining stocks, with the materials sub-index down 4.5%. Consumer discretionary stocks also fell sharply as investors digested July retail sales data, which showed Canada's retail turnover posted its biggest monthly decline since April 2021. Aircraft maker Bombardier was the biggest loser on the day, down 14.3%, as lower crude oil prices and travel demand weighed on the planemaker. Russia's MOEX index fell 4.6% to 2,090 on Friday, after plunging 14% for the week, as Russia's war in Ukraine escalated further and the West faced new threats. President Vladimir Putin ordered the country's first military mobilization since World War II. He stressed that Russia is ready to use its nuclear arsenal after drawing up plans to formally annex four Ukrainian territories through a referendum that has already begun. In addition to sparking widespread protests inside Russia, several EU members states have urged tougher sanctions on Moscow. Many see annexation as a serious escalation, so the Kremlin has reason to believe that Ukraine's latest counterattack is an aggression on Russian territory with Western weapons. Russia's announcement that it will tax exports to boost its budget deficit by 3 trillion rubles has also weighed on Russian financial markets, prompting energy companies to be among the bellwethers of the decline. Mining stocks also fell, down 10% in the session. European shares fell sharply on Friday, with Germany's DAX down 2 percent to a two-year low, as growth concerns weighed on sentiment again after weak PMI data. Business activity in the eurozone shrank for the third month, and Germany's economy deteriorated at a pace not seen since the global financial crisis. Last week, the DAX fell 3.5% as central banks unleashed a wave of interest rate hikes to fight inflation. The Federal Reserve raised interest rates by 75 basis points for the third time to fight inflation, while the Bank of England and the Swiss National Bank also raised rates. The European Central Bank is also expected to raise interest rates further, with policymaker Isabel Schnabel saying on Thursday that inflationary pressures in the eurozone may be more persistent than expected. Meanwhile, the benchmark Stoxx 600 index fell more than 4% for the week and just over 2% on Friday to close at a roughly nine-month low. On Friday, the CAC 40 index fell about 2.3% to close at 5,783, its highest level since March 2021, extending losses for a second session as investors grew increasingly concerned about the ongoing tightening of monetary policy. It will push the global economy into recession, so stay away from riskier assets. The flash purchasing managers' index paints a bleak picture of the eurozone. On the domestic front, the French private sector unexpectedly rebounded in September, with modest growth in the services sector offsetting another slump in manufacturing activity. Nearly all sectors posted losses, with Renault (-7.1%), Thales (-5.5%), Carrefour (-4.9%) and TotalEnergues (-4.9) falling the most. In addition, heavyweight financials and luxury goods were dragged down. For the week, the index fell nearly 5%. FTSE MIB index fell 3.4% to close at 21,065, after plunging 4.7% for the week as a global monetary tightening trend added to recession fears ahead of the weekend's election. Italians are set to elect a right-wing coalition led by Giorgia Meloni of the brothers of Italy, raising concerns among investors that a sudden policy change could prevent recovery of more than 200 billion euros from the European Union funds. Meanwhile, according to PMI data, economic activity in the eurozone contracted for the third straight month. Energy producers and distributors led losses in Milan, tracking a decline in energy prices as macroeconomic data tightened demand. Tenaris fell more than 8 percent, and Eni fell nearly 5 percent. Continuing signs of a sharp economic contraction also weighed on the euro, falling further to a 20-year low. London stocks continued to fall on Friday, dragged down by energy and real estate stocks, with the FTSE 100 blue-chip index falling 2% to around 7,000, closing at its lowest level since March. Investors worry that the government's tax cuts and energy subsidies will put Britain on a more dangerous fiscal trajectory, with some analysts questioning the ability to fund such a massive plan. The market moves coincided with a sell-off in sterling and domestic bonds, with the former hitting a fresh 37-year low and the 10-year gilt soaring above 3.8% for the first time since 2010. On the economic front, the latest UK Purchasing Managers' Index (PMI) data showed that UK private sector output fell further in September. The FTSE 100 fell 3% for the week, its second straight weekly loss. The Hang Seng dropped 59 points, or 0.32%, to 18,089 in early trade on Friday, its third day of losses and its lowest level since December 2011, as Wall Street retreated on concerns that the Fed's increasingly hawkish stance could sink the economy into a tailspin. decline. China said the U.S. Inflation Reduction Act, which scrapped federal tax credits for electric vehicles outside North America, allegedly violated WTO rules, also pointing to a second straight week for the week amid fresh tensions between Beijing and Washington. It fell nearly 3.6% for the week. Locally, Hong Kong's annual inflation rate held steady at a seven-month high of 1.9%, slightly below the consensus estimate of 2%. Basic Materials, Consumer, Industrial, and Utilities are the worst among them. The tech sector, sensitive to rate hikes, was also lower, tracking losses from its Wall Street peers. JD Corporation. Com and Meituan each fell 2 percent, Alibaba Holdings fell 1.6 percent, and Baidu slid 1.1 percent. New Zealand ANZ 50 Index fell 40 points, or 0.34%, to a near four-week low of 11,479 in early trade on Friday, after a slight gain in the previous session and a 0.9% drop last week. Wall Street fell for the third day in a row, and the market continued to worry that the Fed (Federal Reserve) will take a long-term hawkish stance against high inflation. At the same time, the central bank's new economic forecasts highlighted the increased risk of a U.S. hard landing and more rate hike this year. In local data, New Zealand's trade balance widened in August due to high energy costs and a weaker currency. Technology stocks led losses, falling more than 1%, in line with their U.S. peers, as rising Treasury yields weighed on valuations of companies in the sector. Among individual stocks, Savor Limited fell 4.8%, Plexure Group fell 3.9%, while Third Age Health Services and Pay Sauce lost 3.4% and 3.3%, respectively.

REVIEWING ECONOMIC DATA:

Looking at the last economic data:

- CA: In July 2022, the Government of Canada had a budget surplus of C$3.9 billion, compared with a deficit of C$10.9 billion in the corresponding month of the previous year. Revenue increased by C$5.9 billion, or 20.%, reflecting a general improvement in revenue streams. Meanwhile, program spending, excluding net actuarial losses, decreased by $1.8 billion, or 4.8 percent, largely reflecting lower transfers to individuals and businesses, partly driven by higher transfers to other levels of government offset.

- CA: Preliminary estimates suggest that Canadian retail sales may increase by 0.4% month-on-month in August 2022. Considering July, retail sales fell 2.5% from a month earlier, up from a preliminary estimate of a 2% drop, compared with a 1% drop in June. It was the first decline in retail turnover since December 2021 and the largest decline since April 2021, as sales contracted in 9 of 11 sub-sectors. Lower fuel prices and fears of a slowing economy led to a 14.2% drop in gas station sales, preventing the industry's six-month streak of rapid growth. Sales also fell at clothing and accessories stores (-3.3%) and electronics and appliance stores (-2.8%). As a result, retail trade grew at an annual rate of 8% in July, down from an upwardly revised 11.1% in the previous month.

- CA: Preliminary estimates show that total Canadian manufacturing sales fell 1.8% month-on-month in August 2022 after falling 0.9% in July. This was the fourth consecutive month of sales declines, with the largest declines in the chemicals, primary metals, petroleum, and coal products industries.

- US: Preliminary estimates show the S&P Global U.S. Composite Purchasing Managers' Index rose to 49.3 in September 2022 from 44.6 the previous month, indicating a softer decline in private-sector business activity. Services output contracted slower, while manufacturers' production continued to decline slightly. While export orders continued to fall, new orders rebounded, while employment rose. On the price front, input cost inflation fell to its lowest level since early 2021 but remained generally elevated on higher interest rates, materials and wages. Business confidence rose to a four-month high, just shy of the series trend, as new orders and new customer acquisitions are expected to increase further.

- US: In September 2022, the Kansas City Federal Reserve Bank's manufacturing production index recovered to 2 from -9 the previous month. Nonetheless, factory growth remained subdued due to lower activity in durable goods factories (mainly electrical, furniture, non-metallic minerals, primary metals, fabricated metal products, and transportation equipment manufacturing). "Regional factory activity was generally subdued in September. However, businesses continued to add workers," said Chad Wilkerson, vice president, and economist at the Federal Reserve Bank of Kansas City. Moderately optimistic about growth in the coming months.".

- US: The S&P Global U.S. Services Purchasing Managers' Index rose to 49.2 in September 2022 from 43.7 in the previous month, easily beating market expectations of 45.0 but marking the third straight month of contraction for the sector. Business activity fell weakest in three months as new orders, and customer demand rose. Still, new export orders fell for the fourth month, and the backlog returned to growth. On the price front, cost inflation was the lowest since January 2021 in some reports of lower material costs but remained high overall. Finally, business confidence was the strongest since May, as expectations for customer demand improved.

- US: Preliminary estimates show the S&P Global Lightning U.S. Manufacturing Purchasing Managers Index edged to 51.8 in September 2022 from 51.5 in August, beating consensus forecasts of 51.1. Although this was the second-lowest level since July 2020, the data still pointed to relatively benign health in the manufacturing sector. New orders rose for the first time in four months, production fell slightly, demand was rather subdued, and supply chain constraints took a toll on output and capacity. In addition, the backlog of work has increased again, with employment rising at the fastest pace since March. On the price side, input costs have grown slowly, but firms have increased output charges faster. Finally, manufacturers have overall confidence in output growth in the coming year, even as sentiment is dented by ongoing concerns about economic uncertainty and the impact of inflation on consumer spending.

- AU: In September 2022, the S&P Global Flash Australia Services PMI edged up to 50.4 from the final reading of 50.2 in August, marking the eighth consecutive month of expansion in the services sector, but the growth rate remained below the Series average. Panelists said the increase in output reflected overall demand conditions, with the rise in activity broadly similar to the increase in new business. The data also showed that new orders in the services sector continued to improve, but the overall pace of growth was only modest. In addition, services companies added their labor force for the 15th straight month in September. Inflationary pressures have also remained at record highs but have eased from the survey peak earlier this year. Notably, the level of optimism in Australia's services sector continued to deteriorate in September, falling to its third-lowest level on record.

- Au: In September 2022, the S&P Global Rapid Manufacturing Purchasing Managers' Index edged to 53.9 from a final reading of 53.8 in August, indicating improved operating conditions in the commodity-producing sector. Output growth accelerated in September as demand conditions strengthened within the industry. New orders rose steadily as manufacturers benefited from customer wins and higher sales. Likewise, overseas demand accelerated. To meet current demand, manufacturing companies have expanded their workforces at historically high rates. Regarding prices, inflationary pressures in the manufacturing sector have eased considerably. Notably, input and output inflation fell to 19- and 11-month lows, respectively.

- UK: The UK GfK Consumer Confidence Index fell to a record low of -49 in September 2022 from -44 in August, as households continue to grapple with the cost-of-living crisis and wider economic uncertainty. The September figure also unexpectedly rose to -42 following the government's £150bn package to freeze household energy bills. Joe Staton, director of customer strategy at GfK, said: "Consumers are under pressure from the UK's growing cost of living crisis, driven by rapidly rising food prices, domestic fuel bills, and mortgage payments. The data comes a day after the Bank of England raised its policy rate by 50 basis points to 2.25% in response to high inflation, making it more expensive for businesses and households to borrow. The Bank of England expects UK inflation to peak at 11% in October from the current 9.9%.

- SK: South Korean producer prices rose 8.4% year-on-year in August 2022, down from 9.2% the previous month. Prices of electricity, natural gas, and waste rose (24.6%, compared with 21.7% in July), prices of services rose (3.6%, compared with 3.5% in July), and prices of industrial products fell (10.5%, compared with 12.7% in July). Notably, coal and petroleum products fell to 52.8% from 66.1% in July. Agricultural, livestock and marine prices rose across the board (total prices: 6.2% vs. 4.2%, individual prices: 7.4% vs. 5.7%, 5.8% vs. 4.7%, 4.2% vs. -0.4%).

LOOKING AHEAD:

Today, investors will receive the following:

- EUR: German Buba President Nagel Speaks, German Ifo Business Climate, ECB President Lagarde Speaks, Belgian NBB Business Climate, and German Buba President Nagel Speaks.

- USD: FOMC Member Collins Speaks and FOMC Member Mester Speaks.

- JPY: BOJ Gov Kuroda Speaks.

- GBP: MPC Member Tenreyro Speaks.

- JPY: SPPI y/y.

KEY EQUITY & BOND MARKET DRIVERS:

- UK: Yields on Britain's 10-year gilt soared to 3.7% on Friday, from 3.5% the previous day, to the highest level since 2010, after the announcement of the government's growth plan raised concerns among investors about the sustainability of public finances. The measures will include abolishing the top income tax rate of 45p, replacing it with a 40p rate, and cutting stamp duty on home sales. The UK Debt Management Office said it had raised its debt issuance program for the current financial year by £72.4bn, reflecting the funding needed for all the measures announced by the new finance minister. Meanwhile, borrowing costs for other short-term UK government bonds are at a 14-year high: 5-year yields topped 4%, while 3-year and 7-year yields were both near 4%.

- IN: India’s 10-year government bond yield rose to 7.4 percent in September, its highest level since July, as borrowing costs for major central banks rose, making government bonds less attractive to investors. In addition, the Fed raised its fund's rate by 75 basis points for the third time in a row and said rates would remain capped for an extended period to reduce inflation. Domestically, analysts expect the RBI to raise its key interest rate by 35-50 basis points at its September meeting, on top of 140 basis points so far this year, in response to price growth and a slump in the rupee. However, the benchmark is down about 20 basis points from a high of 7.62% in June, driven by strong overseas demand. Investors hope India will soon be added to the JPMorgan Emerging Markets Bond Index after Russia was ousted earlier this year.

STOCK MARKET SECTORS:

- High: n/a

- Low: Energy, Materials, Consumer Discretionary, Communication Services.

TOP CURRENCY & COMMODITIES MARKET DRIVERS:

- AUD: The Australian dollar fell more than $0.66 to its lowest level since May 2020, weighed down by the U.S. Federal Reserve's (Fed's) aggressive plan to curb inflation, which weighed on the global growth outlook and commodities and other risky assets. come under pressure. The Australian dollar weakened after Reserve Bank of Australia deputy governor Michele Bullock reiterated that the central bank was looking for opportunities to slow the pace of interest rate hikes at some point, noting that domestic wage growth was not as strong as in some other developed countries. After raising the cash rate by 225 basis points to a seven-year high of 2.35%, markets remain divided on whether the RBA will raise rates by 50 or 25 basis points next month.

- CAD: The Canadian dollar fell below 1.34 per dollar, its lowest level since August 2020, after the Federal Reserve raised its rate forecast by 75 basis points and foreshadowed sharp hikes ahead. At home, weaker-than-expected inflation slightly eased expectations for how aggressively the Bank of Canada will extend its path to rate hikes. Consumer prices in Canada rose 7% on a yearly basis in August, below expectations for a 7.3% increase and well below the 39-year peak of 8.1% two months ago. In addition, disappointing employment data for August, with Canadians' unemployment rate rising to 5.4 percent from a projected 5 percent, added incentive to slow rate hikes.

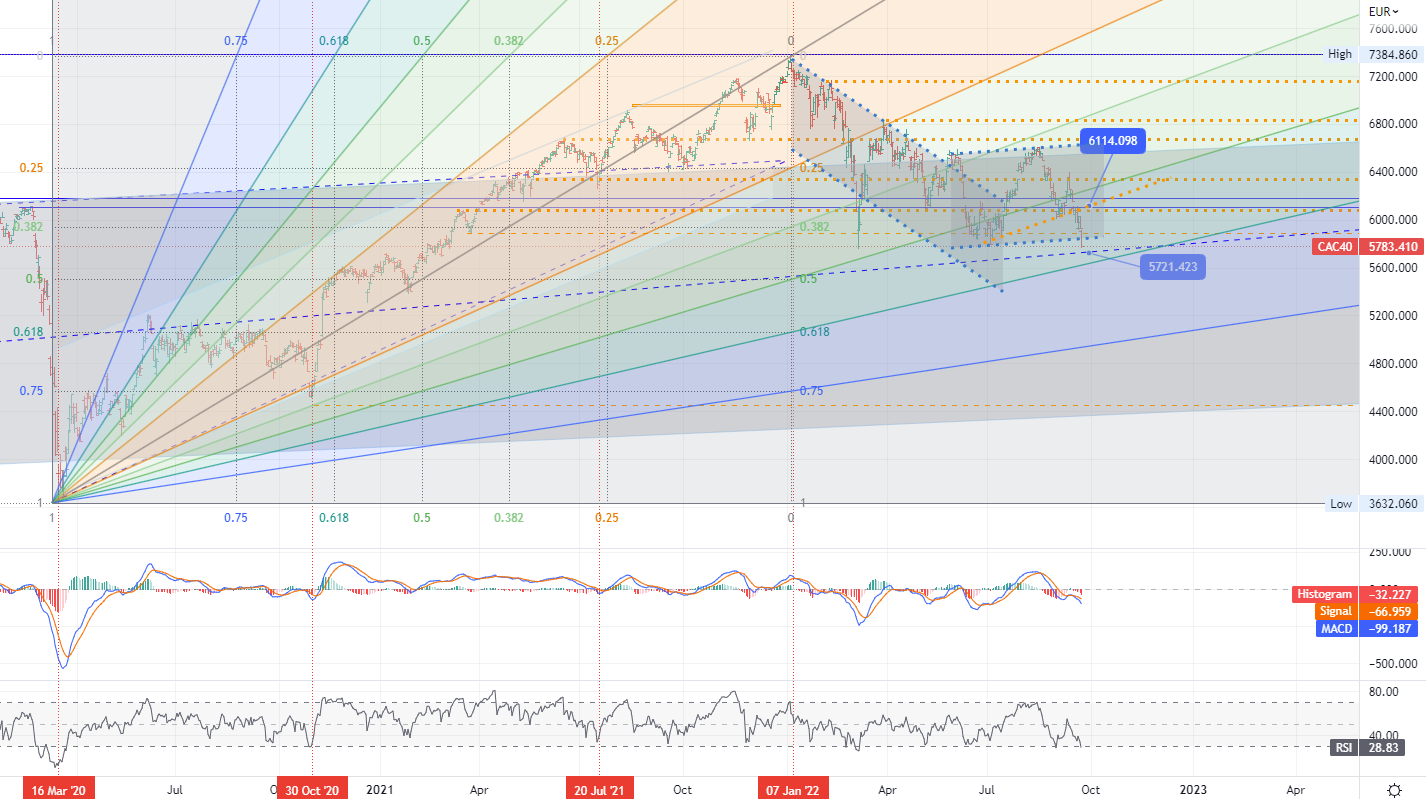

CHART OF THE DAY:

On Friday, the CAC 40 index fell about 2.3% to close at 5,783, its highest level since March 2021, extending losses for a second session as investors grew increasingly concerned about the ongoing tightening of monetary policy. It will push the global economy into recession, so stay away from riskier assets. The flash purchasing managers' index paints a bleak picture of the eurozone. On the domestic front, the French private sector unexpectedly rebounded in September, with modest growth in the services sector offsetting another slump in manufacturing activity. Nearly all sectors posted losses, with Renault (-7.1%), Thales (-5.5%), Carrefour (-4.9%) and TotalEnergues (-4.9) falling the most. In addition, heavyweight financials and luxury goods were dragged down. For the week, the index fell nearly 5%.

- France CAC 40 index - D1, Resistance around ~ 6114, Support (target zone) around ~ 5721.

Start trading in four simple steps

1. Register

Open your live trading account

2. Verify

Upload your documents to verify your account

3. Fund

Deposit funds directly into your account

4. Trade

Start trading and choose from 130+ instruments

Demo account

The Blue Suisse Trading Account with virtual funds in a risk-free environment

Demo accountLive account

The Blue Suisse Trading Account in our transparent live model environment

Open an Account- Trading Account types Trading conditions Trading hours Transparency Market Information

- Products Currencies Commodities Indices Stocks

- Tools MetaTrader 4 / 5 Mobile CRM, MAM and DSP

- Education Currency Trading for Beginners How to improve your trading CFD Trading

- Partnerships Asset- and Moneymanager Tied agent White labels FIX API

- Company About us Regulatory Our philosophy Careers FAQs Contact us