Fed keeps rates near zero as expected - asset purchases will end in early March

• GLOBAL CAPITAL MARKETS OVERVIEW:

European shares posted their biggest gain in seven weeks on Wednesday, with Frankfurt's DAX 30 up 2.2 percent at 15,459, while other significant stocks rose 1.4 percent to 2.5 percent, led by travel and mining stocks. Investors await the outcome of the Federal Reserve's monetary policy meeting scheduled for today, with U.S. officials expected to signal a rate hike as early as March, followed by three more 25-percentage-point hikes by the end of the year amid soaring inflation and steady economic recovery. On the corporate front, Italian fashion group TOD 2021 sales undermined market expectations, while debt recovery firm DoValy said it aimed to keep its total loans steady between 2024 and 160 billion euros. The COVID-19 company and Pfizer announced that they had begun clinical trials to test a new vaccine that targets the COVID-19 OmiCon variant. Meanwhile, hygiene products group Essity posted a bigger-than-expected drop in quarterly profit. On Wednesday, the FTSE MIB index rose 2.3% to close at 26,619, after a slight rebound of 0.2% in the previous session, supported by the industrial and technology sectors, as investors traded in anticipation of the Fed's policy statement confirming a rate hike after the close of March. On the corporate front, industrials rose 2.7%, boosted by steel pipe makers and automakers, while technology shares gained 3.2%. UniCredit (3.6%) and STMicroelectronics (3.1%) closed in the green as traders braced for results ahead of Friday's results. Meanwhile, Tod's rose 15.8% after announcing that European retailers and online sales had returned to pre-pandemic levels. Meanwhile, Italian lawmakers discussed a possible compromise and candidates for the fourth round of elections tomorrow. A simple majority is enough to guarantee victory in the fourth round of elections. On Wednesday, the FTSE 100 rose 1.3 percent to close at 7,470, in line with its European peers, and rose for a second straight session, led by heavyweight mining, energy, and banking stocks. Investors are cautiously awaiting the highly anticipated Federal Reserve monetary policy meeting, where policymakers are expected to signal more aggressive tightening. Meanwhile, traders continued to focus on the evolution of tensions between Russia and Ukraine, with President Biden saying he would consider sanctioning President Vladimir Putin on a rare occasion. In contrast, the British foreign secretary said that option would not be ruled out. Meanwhile, pressure on the UK prime minister eased slightly as Conservative MPs said the party would await the outcome of a police inquiry into illegal parties in the prime minister's official residence. On the earnings front, Wizz Air reported an operating loss of 211.6 million euros in the third quarter and warned that the fourth quarter could be worse before improving in spring 2022. Canada's main stock index, the S&P/TSX, extended gains on Wednesday, cementing a rally from the previous session, as traders digested the Bank of Canada's monetary policy decision and the focus shifted to the Federal Reserve later in the session time of the meeting. Meanwhile, higher oil prices supported the heavyweight energy sector. The Bank of Canada's decision to keep both rates and forward guidance unchanged means that rates will rise in mid-2022. Policymakers noted that inflation is expected to fall to its 2 percent target in the second half of the year, while gasoline prices, a critical upside risk, have declined recently. In a corporate update, NBC analysts raised their target for Canadian National Railway to C$172 per share from C$170 previously. U.S. stocks rallied on Wednesday, with the Dow up more than 200 points before inching up slightly, with the S&P 500 up about 1% and the Nasdaq soaring nearly 2%. Microsoft was one of the biggest gainers, with earnings, revenue, and sales forecasts all beating forecasts, rising 4%. AT&T and Abbott also posted gains, but shares failed to rise after the company reported a much larger-than-expected loss of $7.69 per share in the fourth quarter, with Boeing shares falling more than 3%. Tesla and Intel will report quarterly results after the market closes. Meanwhile, investors looked forward to the Fed's decision later in the day for a clearer picture of how much and how fast rates will rise. On Wednesday, the ruble-based MOEX-Russian index rose 2.6% to hover around 3,340, extending some of yesterday's rally, supported by energy and commodity-backed stocks. Rising oil and gas prices lifted energy shares by 2.2%, while gains in metals pushed mining shares up 2.9%. However, the benchmark was still down about 3% in the week after Monday's slump, as investors had to treat Russian assets with extreme caution amid geopolitical uncertainty over Ukraine's military campaign and the prospect of Western sanctions. The blue-chip index edged lower, with Gazprom leading losses (-0.8%) as possible sanctions threatening Germany's Nord Stream 2 pipeline approval. In comparison, Russia's Federal Reserve Bank (Sberbank) fell 0.9% on expectations. The Fed and CBRE (CBR) will tighten policy. Meanwhile, Samolet fell 3% after reporting fourth-quarter corporate results. On Wednesday, the Shanghai Composite rose 0.66 percent to close at 3,456, while Shenzhen rose 0.7 percent to close at 13,780, as investors snapped up hard-hit Chinese stocks after a heavy sell-off in the previous session. On Tuesday, markets saw an accelerated sell-off in mainland stocks as investors felt the recent policy rate cut would not be enough to boost China's economy. The People's Bank of China has slashed a slew of key short- and medium-term interest rates to boost economic growth. Still, analysts expect more easing, including lowering the reserve requirement ratio, to impact material. High-growth new energy and electronic technology companies led the rally, including Contemporary Amber (3.87%), BYD Corporation (3.82%), Longi Green Energy (3.84%), Jiangsu Zhongtian (10%) and Tianjin Zhonghua ( 4.15%), and other companies.Nikkei 225 lost 0.44% to close at 27,011, an 11-month low, while the broader Topix index lost 0.25% to close at 1,892, as investors braced for a tightening by the Federal Reserve Stocks tracked overnight losses on Wall Street. The Fed ends its two-day meeting on Wednesday, and while the central bank is not expected to change policy, investors will be looking for hints on the timing and extent of rate hikes and quantitative tightening. Investor sentiment was also subdued as Japan continued to battle a record number of Covid-19 cases after Japan expanded a state of quasi-emergency to 34 of the country's 47 prefectures on Tuesday. Chipmakers and precision manufacturing companies led the declines, among which Tokyo Electronics (down 0.81%), Ned (down 3.18%), Kean (down 1.8%), Fanuk (down 3.29%), Murata (down 2.03%), and Hitachi (down 0.91%) and other companies fell significantly.

• REVIEWING ECONOMIC DATA:

Looking at the last economic data:

- RU: Russian producer prices rose 28.5% year-on-year in December, a slowdown from the previous month's 29.2% increase. Producer price inflation eased from a five-month high as cost growth slowed in mining (59.2% vs. 62.3%) and manufacturing (23.5% vs. 23.7%). Meanwhile, utility prices rose faster (5.8% vs. 2.9%). Monthly, the producer price index rose 0.8%, up from a 0.4% gain a month earlier.

- US: New home sales in the U.S. rose 11.9% from a month ago to a seasonally adjusted annual rate of 811,000 through December 2021, and November's year-over-year increase easily topped the consensus estimate of 760,000. Home sales reached their highest level since last March, with the most significant increases in the Midwest (56.4% to 86,000), South (14.9% to 456,000), and West (0.4% to 242,000). On the other hand, new home sales in the Northeast fell 15.6 percent to 27,000. Last month, the median sale price of a new home was $377,700, 3.4% higher than the median home price a year ago, while the average sale price was $457,300, up 11.8% year over year. The supply of new homes for sale fell by 9.1 percent, equivalent to a six-month supply between November and December.

- US: A preliminary estimate showed U.S. wholesale inventories rose 2.1% month-on-month to $2021 in December, up from 1.7% in November and above consensus forecasts of 1.3%. It was the 17th consecutive month of growth, with inventories of both durable goods (2.4% vs. 2.5% in November) and nondurable goods (1.6% vs. 0.6%) rising. Wholesale stocks rose 18.3% year-on-year in December.

- US: The U.S. goods trade deficit was revised to a record high of $2021 in December from $98 billion in the previous month, forecasts showed. Imports rose 2% to $258.26 billion, reflecting a continued recovery in domestic demand due to rising wages and economic growth. In addition, automobiles (8.4%) and consumer goods (7.6%) rose. Meanwhile, export growth slowed by 1.4% to $157.3 billion, driven by higher sales of capital goods (1.9%) and consumer goods (6.5%). As a result, in 2021, the U.S. announced a merchandise shortfall of $1.86 trillion, the most significant annual sales gap in history.

- UK: British public expectations for inflation over the next 12 months rose to an all-time high of 4.8% in January 2022 from 4.0% the previous month, a survey by YouGov and Citi showed. In addition, long-term inflation expectations for five to ten years later held steady at 3.8%, the highest level in eight years. Citi economists said: "Today's data, especially the level of long-term expectations, suggest that high-risk inflation expectations may deviate from the upside as inflation accelerates in the coming months. However, for now, we believe that overall expectations remain stable.". The Bank of England is expected to raise rates by another 25 basis points next month, the second since the outbreak of the pandemic, as inflation has been running above double the central bank's target.

- UK: Mortgage applications in the U.S. fell 7.1% in the week ended Jan. 21, the most significant drop in two months, as the refinance index fell, according to the Mortgage Bankers Association. 12.6%, and the home purchase index fell 1.8%. The average 30-year fixed mortgage rate rose to 3.72% from 3.64%, the highest since March 2020, and U.S. Treasury yields continued to climb to a two-year high. MBA economist Joel Kan said: “After almost two years of low-interest rates, not many borrowers have an incentive to refinance. Among those still in the market looking for refinancing, high-interest rates have proven to be a nuisance to them. is much less attractive."

- EU: The number of unemployed registered in mainland France fell by 12,800 from the previous month to reach December 2021, the lowest level since September 2012, as the labor market recovers from the pandemic. Across age groups, the unemployment rate for people aged 25 to 49 fell by 10,600 to 1.794 million, and for those aged 50 and over, it fell by 65,000 to 876,000. On the other hand, the unemployed among the young population rose by 43,000 to 405,000. Compared with the same period last year, the number of registered unemployed fell by 512,300.

- EU: In January 2022, the French consumer confidence index edged down 1 point to 99, slightly above market expectations of 98, but below the long-term average of 100, indicating pessimism among consumers. The proportion of households who believe now is an appropriate time to make a large purchase fell (-17 to -14 in December), while the proportion of households who think prices will increase over the next 12 months rose slightly (7 to -8).

- SW: n December, Sweden's trade account turned from a surplus of SEK 1.2 billion in the same period last year to SEK 5.5 billion in 2021. Exports rose 23% to SEK 147.3 billion year-on-year, while imports rose 29% to SEK 152.8 billion. There is one more working day in December 2021 than in December 2020. Merchandise trade with countries outside the EU led to a surplus of SEK 16.9 billion, while EU trade led to a deficit of SEK 22.4 billion.

- JP: Japan's economic indicators, including factory output, employment, and retail sales, reached 92.8 in November 2021, compared to 93.6 the previous month and 89.8 last month. It was the highest level since July and rose for a second straight month as coronavirus-related disruptions eased as infection rates fell and vaccinations accelerated.

• LOOKING AHEAD:

Today, investors will receive:

- USD: Goods Trade Balance, Prelim Wholesale Inventories m/m, New Home Sales, Crude Oil Inventories, FOMC Statement, Federal Funds Rate, and FOMC Press Conference.

- EUR: German 10-y Bond Auction.

- JPY: BOJ Summary of Opinions, and SPPI y/y.

- AUD: MI Leading Index m/m, and Import Prices q/q.

- CHF: Trade Balance.

- EUR: German GfK Consumer Climate, and Spanish Unemployment Rate.

• KEY EQUITY & BOND MARKET DRIVERS:

- The Bank of Canada kept its overnight rate target at 0.25% at its first meeting in 2022, in line with expectations, but said it had withdrawn its exceptional forward guidance to keep policy rates at the effective lower bound as broader economic weakness has now been priced in. The first-rate hike since 2018 paved the way. The central bank will also keep its holdings of Canadian government bonds on its balance sheet essentially unchanged, at least until it starts raising policy rates. Regarding prices, inflation was close to 5% in the first half of 2022 and will fall reasonably quickly to around 3% by the end of the year. The bank expects the Canadian economy to grow by 4 percent in 2022 and about 3.5 percent in 2023.

- Yields on China's 10-year government bond rebounded from a 20-month low to above 2.71%, as traders digested signs of slowing government spending amid heightened volatility ahead of the upcoming Lunar New Year holiday. In early 2021, national government spending rose 0.3% from a year earlier, the slowest pace in nearly 20 years, while revenue increased 10.7%, reflecting limited financial support for the faltering economy. However, China's vice finance minister said the revenue beat expectations, which would allow the government to step up spending in 2022 and strengthen support for lower authorities. Yields hit 2.66% on Jan. 25, the lowest level since May 2020, after the People's Bank of China decided to cut key interest rates for the second time in a row while signaling more support for a slowing economy.

- U.S. futures rallied on Wednesday, with the Dow and S&P 500 both up about 1% and the Nasdaq up nearly 2%, as investors looked to the Federal Reserve to make a decision later in the day to provide further clarity on the central bank's tightening policy. In addition, AT&T's earnings season continues to hit its stride. Abbott and Boeing will also report before the market opens, while Tesla and Intel will say after closing. Meanwhile, Microsoft shares rose 3% in premarket trading after beating forecasts for earnings, revenue, and sales.

- The Federal Reserve is expected to maintain a hawkish tone at its first meeting in 2022, confirming that interest rates will start to rise in March. Investors will also be watching for more details on the policy normalization process that began last November. The asset-purchase program will end in March, and the bank's $8.9 trillion balance sheet will shrink. In addition, the Federal Reserve announced at its December meeting that it would end pandemic-era bond purchases in March, paving the way for three rate hikes by the end of 2022. However, many investors are beginning to believe that the Fed will tighten monetary policy more aggressively than expected and raise interest rates four times.

- The yield on the benchmark 10-year U.S. Treasury note edged up to 1.78% on Tuesday, away from a two-week low at the start of the week, as market volatility and stock market decline? The sell-off continues as investors await the decision of the Federal Open Market Committee tomorrow. The Fed is set to raise the federal funds rate in March and lower its balance sheet later this year. However, the scale of the hike remains uncertain, and investors fear the central bank will tighten monetary policy more aggressively than expected.

• STOCK MARKET SECTORS:

- High: Information Technology, Consumer Discretionary, Communication Services.

- Low: Consumer Staples, Utilities.

• TOP CURRENCY & COMMODITIES MARKET DRIVERS:

- OIL: U.S. crude inventories unexpectedly rose by 2.377 million barrels in the week ended Jan. 21, the most significant increase since late October, compared with a consensus forecast of 728,000 barrels, data from the EIA Oil Conditions report showed. . Meanwhile, gasoline inventories rose by 1.297 million barrels, missing market expectations for a rise of 2.548 million barrels.

- CAD: The Canadian dollar edged lower to a 2-week low of $1.26/USD, boosted by a stronger dollar. The Federal Reserve is expected to tighten monetary policy at a faster-than-expected pace. At the same time, the Bank of Canada keeps rates steady at its first meeting of 2022, disappointing some investors. However, the central bank said rates would be raised soon, possibly at its next meeting on March 2.

- CNY: The offshore yuan lingered at a 3-1/2-year high of 6.33 against the dollar on Wednesday, buoyed by a more prudent adjustment from the central bank and solid corporate demand ahead of the Lunar New Year holiday. On Wednesday, the People's Bank of China set the primary parity rate at 6.3246 yuan per dollar, 0.27% higher than the previous setting of 6.3418 yuan and the highest level since April 2018. The move signals to the market that Chinese authorities appear to be more lenient on the yuan's strength. Meanwhile, the yuan has continued to appreciate despite a series of policy easing measures by Beijing, with the People's Bank of China slashing several critical short- and medium-term interest rates to boost economic growth. Analysts expect the People's Bank of China to roll out easing measures in the first half of this year and further cut interest rates and lower the reserve requirement ratio in the first quarter.

- AUD: The Aussie was hovering below $0.718 on Wednesday, struggling to build momentum despite higher-than-expected inflation data the day before. Investors weighed the prospect of Australia's early acceleration after Australia's core inflation accelerated to 2.6% in the fourth quarter of 2021, more than a forecast of 2.3% and a registration in the Reserve Bank's halfway target range of 2.3% quick. The latest inflation figures pose a challenge to the RBA. It has repeatedly insisted that domestic interest rates will not likely rise until 2023 or until inflation continues to push above its 2-3 percent target range. Meanwhile, risk-sensitive currencies remained under pressure amid rising geopolitical tensions and expectations for more aggressive Fed tightening.

- NZD: The New Zealand dollar hovered at a 14-month low above $0.67 on Wednesday, as risk currencies remained under pressure from geopolitical risks and rising expectations for more aggressive Fed tightening. The U.S. central bank ends its two-day meeting on Wednesday. While no rate change is expected, a growing number of Fed officials said they were ready to accelerate the pace of policy normalization. Meanwhile, the Reserve Bank of New Zealand hiked interest rates twice last year to 0.75%, and amid persistent inflation and record-low unemployment, the policy on February 23 is widely expected. At the meeting, interest rates will rise to 1.0%. Investors are also awaiting Thursday's fourth-quarter inflation data from New Zealand, which is likely to accelerate at the fastest pace since 1990 to 5.7%.

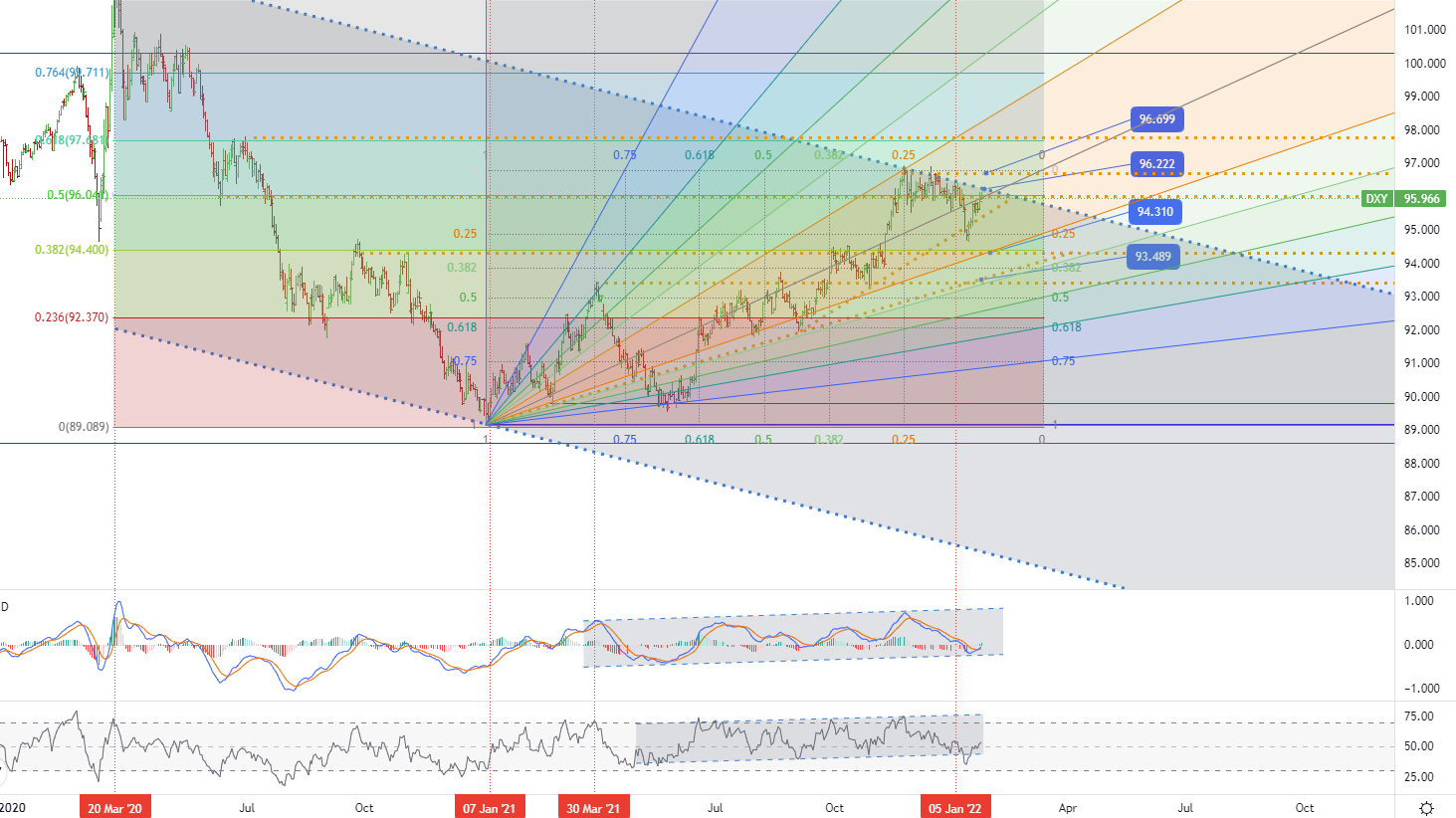

• CHART OF THE DAY:

The U.S. dollar index rose to a three-week high of 96.2 on Wednesday as traders awaited the Federal Reserve's monetary policy decision later in the day for more clues on the magnitude and pace of rate hikes. The odds are rising that the Fed will need to tighten monetary policy faster than expected, while other central banks around the world appear more reluctant to raise borrowing costs. Meanwhile, rising geopolitical tensions have also boosted the safe-haven dollar, with U.S. President Joe Biden threatening to sanction Vladimir Putin if he orders an invasion of Ukraine. • U.S. dollar index (DXY) - D1, Resistance (target zone) around ~ 96.222 & 96.669, Support (consolidation) around ~ 94.310 & 93.489.

• U.S. dollar index (DXY) - D1, Resistance (target zone) around ~ 96.222 & 96.669, Support (consolidation) around ~ 94.310 & 93.489.

Start trading in four simple steps

1. Register

Open your live trading account

2. Verify

Upload your documents to verify your account

3. Fund

Deposit funds directly into your account

4. Trade

Start trading and choose from 130+ instruments

Demo account

The Blue Suisse Trading Account with virtual funds in a risk-free environment

Demo accountLive account

The Blue Suisse Trading Account in our transparent live model environment

Open an Account- Trading Account types Trading conditions Trading hours Transparency Market Information

- Products Currencies Commodities Indices Stocks

- Tools MetaTrader 4 / 5 Mobile CRM, MAM and DSP

- Education Currency Trading for Beginners How to improve your trading CFD Trading

- Partnerships Asset- and Moneymanager Tied agent White labels FIX API

- Company About us Regulatory Our philosophy Careers FAQs Contact us