Global equities and oil bounce, гold slips from overnight highs

• GLOBAL CAPITAL MARKETS OVERVIEW:

European stock markets rose on Monday after their worst-selling in more than a year. Investors are waiting for clues about whether the Omicron mutant virus will hinder economic recovery and central banks' tightening monetary plans. The pan-European STOXX 600 index closed up 0.7%, the biggest one-day gain in a month, partially regaining the 3.7% drop last Friday due to market concerns about newly discovered mutant strains. Although this mutation has been found in many countries worldwide, a doctor in South Africa said that the symptoms are very mild and can be treated at home so far. He is one of the whistleblowers of the mutant strain of Omicron. Travel and leisure stocks rose, with Wizz Air, Lufthansa, TUI Group, Ryanair, and Carnival Corp rising between 1-5.5%. Due to concerns about new travel restrictions, these stocks experienced double-digit declines last Friday. Financial stocks rose 1.7%, with energy and basic materials stocks leading the way due to higher commodity prices. The London FTSE 100 index rose 0.9%, and investors bet that the Bank of England might be forced to reconsider tightening monetary policy next month. Although the STOXX 600 index has repeatedly set new highs in November, it is still expected to record a monthly decline of 1.7%. The strong performance of the earnings season and the weakening of market concerns about monetary policy tightening were offset by concerns about the discovery of new variations and new restrictions in Europe. The German DAX index closed up 0.16%, and the French CAC-40 index closed up 0.54%. Gold prices fell on Monday, returning to the previous week's general downward trend. As the US dollar strengthened and risk sentiment rebounded, the market is weighing how severe the impact of the Omicron variant virus will be on the economy. spot gold fell 0.4% to $1,784.80 per ounce. Last week's weekly decline was 2.9%, the biggest weekly decline since June. US gold futures closed at 1,782.30 US dollars, down 0.2%. Last week, the discovery of this new variant prompted some countries to strengthen border controls, leading to a sell-off in the global market. Since then, the global market has returned to its apparent calm. Spot silver fell 1.3% to $22.84 per ounce. Platinum rose 1.2% to US$965, while palladium rose 2.7% to US$1,795.69. The Japanese stock market fell sharply on Monday, and the Nikkei index fell to its lowest level in a month and a half due to concerns that the Omicron new crown virus variant may cause damage to the economy. The Nikkei index closed down 1.63% to 28,283.92 points. The last time it hit this low was on October 11, when the index fell 2.5% on Friday. The Topix Stock Index fell 1.84% to 1,948.48 points, the first time it fell below the 200-day moving average since August 2020. Japanese Prime Minister Fumio Kishida said that Japan would ban foreign tourists from entering the country on November 30, seeking to cope with the spread of the new variant of the new coronavirus, Omicron. Then market sentiment deteriorated. The travel-related industries suffered the most, with Oriental Land Corp, the operator of Tokyo Disney Resort, falling 4.8%. Tokai Railway (JR Tokai) fell 4%, East Japan Railway (JR East) fell 3.9%, and Keisei Electric Railway fell 7.6%. Automakers fell as the yen rebounded against the dollar, and the Topix Transportation Equipment Index fell 3.05%, the biggest drop in more than three months. Nissan Motor fell 5.6%, Suzuki Motor fell 3.9%, and Honda Motor fell 3.8%. Industry leader Toyota Motor fell 3%. However, some investors are still cautiously buying on dips, taking comfort from a report. According to the report, a South African doctor who has treated the case said that so far, Omicron's symptoms are mild. Only one in every 14 stocks rose. Trading volume on the Main Board of the Tokyo Stock Exchange soared to 3.394 trillion yen ($30 billion), which is about 20% higher than the long-term average. The Moscow Exchange index closed 9.6% below the all-time high of 4,292.68 points reached on October 14. Friday's drawdown in financial markets was emotional, excessive, and due to low liquidity, as well as other technical factors. On Monday, oil and metal prices recovered their losses. Against the backdrop of the return of risk appetite, stock markets in the US and Europe were growing. Of course, this had a positive effect on the Russian market. Scientists are now trying to assess the consequences of the emergence of the omicron strain and predict whether it will be able to overtake the delta strain that is currently dominant in the world. Many questions remain, but the market is being laid on the fact that for already vaccinated people who can become infected with omicron, vaccination will protect them from the need to go to a hospital bed in a hospital. Five sectoral indices rose, and five declined. Telecoms fell 0.97% and became the outsider of the day (-5.5% in November). The consumer sector grew by 1.74% and became the growth leader (-4.7% in November). The oil and gas sector grew by a comparable 1.73% (-6.5% in November). Of the 43 shares of the Moscow Exchange index, 31 rose in price, and 12 lost in value. The Shanghai Composite Index of China's stock market opened lower on Monday, and its decline narrowed until the close was nearly flat. Analysts believe that the market's worries about the latest variant of the new crown virus have eased, and sentiment has turned. Despite this, the mutated strains have caused concerns about travel obstruction and still dragged down the performance of travel stocks—the Shanghai Composite Index.SSEC closed nearly flat, slightly down 0.04% to 3,562.7 points, while the Shanghai and Shenzhen 300 Index.CSI300 fell 0.2%. The Shenzhen Growth Enterprise Market Index.CNT closed up 1%, and the Shanghai Stock Exchange Science and Technology Innovation Board 50 component index.STAR50 closed up 0.8%. Huang Weikang, Chairman and Chief Executive Officer of Hong Kong Anli Holding Group, said that the Shanghai Composite Index's decline has narrowed because people begin to feel that the mutant virus may have a strong spread. However, the death rate may not be high, and China's border control is still biased towards closed. The impact is limited. The performance of Asian stock markets today is not bad. Omicron's new coronavirus variant spread around the world on Sunday. New cases were detected in the Netherlands, Denmark, and Australia, and more countries have imposed entry restrictions. The travel sector of the Chinese stock market, which is sensitive to the epidemic, plummeted on Monday, and the Omicron new crown variant strain has caused the market to worry that travel will be severely affected again. The China Securities Tourism Theme Index fell 3.4%. The military industry led the gains, with the China Securities and AVIC Military Industry Subject Index closing up 2.3%. Previously, the Eastern Theater of China stated that the organization of continuous military patrols in the direction of the Taiwan Strait is a necessary measure to deal with the situation in the Taiwan Strait.

• REVIEWING ECONOMIC DATA:

Looking at the last economic data:

- US: The US October second-hand housing purchase and sale contract index rose by 7.5% month-on-month, which exceeded market expectations and reversed the decline in September; the index fell 1.4% year-on-year.

- RU: Gazprom predicts a record price of export deliveries to non-CIS countries in the last quarter of this year - an average of $ 550 per 1,000 cubic meters, and expects that, in general, for 2022, it will not be lower than in 2021. The gas giant published financial results for the 3rd quarter of 2021 under IFRS. Revenue, including net income from trading operations, grew by 20% QoQ and 79% YoY to RUB 2.5 trillion. The average gas sales price to non-CIS countries is $ 311 / thous. Cub. m. This is 40% more than in the previous quarter. EBITDA + 15% QoQ and 2.4 times YoY to RUB 809 bln. Net profit increased by 11.6% QoQ to RUB 582 bn. On the whole, we view the report as positive, as net income and base for dividends exceeded forecasts. The company expects Q4 to contribute more to its annual dividend than the previous three quarters due to the increase in the price of Gazprom's portfolio of contracts. In long-term contracts, oil indexation is partially retained with a lag. Therefore, in 4Q., oil indexation will be based mainly on oil prices in Q2. 2021 - about $ 69 / bbl for Brent.

- RU: Norilsk Nickel believes that the new MET calculation in 2022 will not lead to an increase in costs compared to 2021, provided that the current metal prices remain unchanged. As a reminder, this year, metallurgists pay an increased MET, taking into account the applied coefficient of 3.5. Also, from August to the end of the year, and export duty is used, due to which Norilsk Nickel, according to its calculations, did not earn $ 500 million.

- RU: The management of the Samolet Group of Companies voiced very optimistic forecasts while communicating with investors. The company plans to double its bottom line over the next three years. The GMV figure is expected to reach RUB 2 trillion by 2025. In 2022, sales will exceed 1.5 million sq. m, and EBITDA will exceed 65 billion rubles, revenue - 250 billion rubles. However, already in 2023, according to forecasts, sales will exceed 2.4 million square meters. m, EBITDA will exceed 100 billion rubles, revenue - more than 400 billion rubles. Further, in 2024, sales will exceed 3.5 million sq. m, EBITDA - will exceed 150 billion rubles, revenue will be more than 600 billion rubles.

- GB: There are two new cases of the Omicron variant of the new crown virus in England and 6 cases in Scotland. Together with the cases in the past weekend, there have been 11 cases of the Omicron variant of the new crown virus in the UK. In the past day, there were more than 42,000 new confirmed cases in the UK. The Joint Committee on Vaccination and Immunization in the United Kingdom stated that all adults would be vaccinated with a booster of the new crown vaccine. The interval between the second dose and the booster will be shortened from the original six months to 3 months, hoping to speed up the vaccination schedule. The committee also stated that after the first dose of vaccine for 12 to 15-year-olds, the second dose could be given 12 weeks later. The committee believes that the booster vaccination can help increase antibody levels in response to the Omicron variant of the new coronavirus. The committee also stated that Modena and Pfizer's vaccines are the first-choice vaccines for boosters.

- EU: The variant new coronavirus Omicron continues to spread, with cases in Sweden and Spain one after another, and the patients are all from South Africa. The Spanish authorities said that the 51-year-old man who was diagnosed entered the country from South Africa via Amsterdam on Sunday. The officers determined the virus to be the Omicron variant virus after genetic sequencing. The patient is currently in good condition with mild symptoms. The Swedish health department also stated that the first case was discovered during a test on a person who entered South Africa a week ago. According to the authorities, Omicron has appeared in several European countries, so it is expected that Sweden will also find cases and believe that Omicron should be taken very seriously before learning more.

- EU: The Consumer Price Index (CPI, preliminary figures) for November released by the German Federal Statistical Office increased by 5.2% from the same month of the previous year. The rate of increase is the largest since June 1992. became. The European Union (EU) Standard (HICP) CPI rose 6.0% from the same month last year, the highest rate of increase since January 1997, when HICP aggregation began. Growth has accelerated from 4.6% in October, increasing pressure on the European Central Bank (ECB). The ECB's managing director, Schnabel, told ZDF TV yesterday that the ECB is convinced that inflation peaked in November and that rate hikes are premature as inflation is likely to slow gradually next year. The preliminary figures for eurozone inflation in November announced on the 30th are expected to be 4.5%, accelerating from 4.1% in October. Inflation rates have risen sharply in recent years, including base effects, rising energy prices, the temporary value-added tax rate (VAT) of the previous year due to the pandemic of the new coronavirus, and a shortage of raw materials during the economic recovery process. Factors are mixed.

- CN: China South City's interim profit as of the end of September was 557 million yuan, an increase of 0.5% year-on-year; after deducting the fair value gains of investment properties and specific tax effects, and goodwill impairment, the core profit was 649 million yuan, down 11.6%. No interim dividend will be paid. In the first half of the year, the group's total revenue fell by 11.2% to 6.166 billion yuan, mainly due to the lack of property sales and delivery. The gross profit margin was 36.6%, down 1.4% year-on-year. Contract sales were 7.02 billion yuan, down 11%. As of the end of September, the group’s gearing ratio was 63.9%, a decrease of 3.7 percentage points from the end of March; the weighted average financing cost was 8.51%, an increase of 0.12 percentage points from the end of March. The total interest-bearing bank and other borrowings exceeded 22.176 billion Hong Kong dollars, increasing from the end of March. Over 17%, of which HK$6.086 billion must be repaid within one year or on-demand.

- CN: China Gas had an interim profit of 4.1 billion yuan as of the end of September, a year-on-year decrease of 19.3%. Interim dividend of 10 HK cents per share. The Group's revenue for the first half of the year increased by 43.4% year-on-year to 38.9 billion yuan, of which pipeline gas sales rose by about 59% to 19.8 billion yuan, and liquefied petroleum gas sales rose nearly 1.3 times to 11.3 billion yuan. Total sales of natural gas rose 21.1% year-on-year, and sales of liquefied petroleum gas rose 11.9%. On the other hand, newly connected residential users decreased by 39% year-on-year, new related industrial users increased 64.8%, and further connected commercial users increased 6.6%. The group said that a severe gas explosion accident occurred in the joint venture company in Shiyan City during the period. However, it recognizes that there are still weak links in safe operation and management and will continue to invest resources to increase the application of advanced pipe network testing equipment and improve intelligent control.

• LOOKING AHEAD:

Today, investors will receive:

- USD: FOMC Member Bowman Speaks, HPI m/m, S&P/CS Composite-20 HPI y/y, Chicago PMI, Fed Chair Powell Testifies, CB Consumer Confidence, Treasury Sec Yellen Speaks, FOMC Member Williams Speaks, and FOMC Member Clarida Speaks.

- EUR: French Consumer Spending m/m, French Prelim CPI m/m, French Prelim GDP q/q, German Unemployment Change, CPI Flash Estimate y/y, Core CPI Flash Estimate y/y, Italian Prelim CPI m/m, and Italian 10-y Bond Auction.

- AUD: RBA Deputy Gov Debelle Speaks, Building Approvals m/m, Current Account, Private Sector Credit m/m, RBA Deputy Gov Debelle Speaks, and AIG Manufacturing Index.

- JPY: Unemployment Rate, Prelim Industrial Production m/m, and Housing Start y/y.

- CAD: Gov Council Member Schembri Speaks, and GDP m/m.

- NZD: Final ANZ Business Confidence and Building Consents m/m.

- JPY: Unemployment Rate, Prelim Industrial Production m/m, and Housing Start y/y.

• KEY EQUITY & BOND MARKET DRIVERS:

- In the euro area financial and bond markets, government bond yields, which fell sharply last week, rose slightly as panics on the new variant of the new coronavirus "Omicron" converged. There is a growing movement in the market to determine the impact of new mutants on the global economy. German 10-year bond yields fell sharply on the 26th of last week, but trading at the end of the day rose two basis points (bp) to minus 0. 314%. However, it is still 10bp lower than the high-level set last week. Yields on other high-rated government bonds, such as the Dutch 10-year and French 10-year bonds, also rose by about 2-3bp.

- Aeroflot has published financial results for the 3rd quarter of 2021: net profit of 11.6 billion rubles. Against 21.1 billion rubles. Loss a year earlier. Revenue almost doubled to RUB 167.1 billion. EBITDA grew 2.7 times to RUB 54.1 billion. For nine months, gain + 54.7% to 362.2 billion rubles, EBITDA jumped 3.1 times to 95.6 billion rubles, and the net loss decreased by 79.7% to 16.1 billion rubles.

- The net profit of Acron for nine months amounted to 50.93 billion rubles. Against a loss of 4.16 billion rubles. A year earlier. Revenue amounted to 117.22 billion rubles. Against 86.09 billion rubles. A year earlier. EBITDA amounted to RUB 69.19 billion against 24.12 billion a year earlier. Net debt decreased by 26% to RUB 74.02 billion. Against 99.58 billion rubles. At the end of 2020. The report looks quite positive as the EBITDA margin increased from 28% to 50%. At the same time, the debt burden decreased: the net debt / EBITDA ratio at the end of the reporting period decreased to 0.9 from 2.8 at the end of 2020.

- Profit attributable to Tatneft shareholders in the third quarter increased to 52.06 billion rubles. Against 35.75 billion rubles. A year earlier. Quarterly revenue amounted to RUB 323.84 billion. Against 187.37 billion rubles. A year earlier. The company's div policy assumes a target level of payments of at least 50% of net profit under RAS or IFRS (whichever is greater). Net profit (RAS) for nine months of 2021 amounted to 123.28 billion rubles. Net profit under IFRS for six months 2021 amounted to 92.2 billion rubles. We get 144.3 billion rubles for nine months, which is 17% more than profit under RAS. Perhaps an adjustment will be made when determining the final dividend for 2021.

- Hertz Global Holdings (HTZ) shares grew by 4.6%: the company plans to buy securities from the market for up to $ 2 billion. Hertz withdrew from the reorganization procedure after bankruptcy just a few months ago;

- Walmart (WMT) shares declined 0.93%: CEO Brett Biggs, who has headed it for more than 20 years, plans to leave office in early 2023;

- Shares of Adagio Therapeutics (ADGI) rose 69%: Morgan Stanley upgraded its rating to “above market” from “equal weight.” Bank Analyst Believes Omicron Appearance May Increase Demand For ADG20 Drug;

- Stocks of airlines and companies from the tourism and recreation sector corrected after Friday's collapse;

- eBay (EBAY) shares lost 3%: Baird analyst noted a slowdown in the company's sales growth;

- Greif (GEF) shares fell 3%: Wells Fargo analysts downgraded the recommendation for the shares to “equal weight” from “above market,” citing their high value;

- Krystal Biotech (KRYS) shares up 122% on news of success in trials of Vyjuvek;

- Merck (MRK) shares fell 4% ahead of regulatory review of the company's drug for the treatment of coronavirus infection tomorrow;

- Twitter (TWTR) shares gained 3.5% after CNBC reported that its CEO

- Jack Dorsey may step down.

• STOCK MARKET SECTORS:

- High: Energy, Technology, Consumer Discretionary, Utilities, Real Estate.

- Low: Consumer Staples, Materials, Industrials, Financials.

• TOP CURRENCY & COMMODITIES MARKET DRIVERS:

- CURRENCY: The yen and the Swiss franc were the top gainers in the Big Ten last week amid concerns that a new omicron strain could undermine the global economic recovery. The dollar index renewed its 16-month high but on Friday lost all weekly gains as US Treasury bond yields declined, and the money market was pledged to delay the start of the Fed rate hike due to the virus. For example, if on Wednesday, November 24, the futures market for the federal funds rate with 100% probability implied an increase in the rate in June and with a 66% probability took into account the possibility of such a step in May 2022, then by now the market assessed the probability of a rate hike in June fell to 76%. However, on Monday morning, November 29, the currencies of the commodity block (Canadian, Australian, New Zealand dollars, and the Norwegian krone) were actively strengthening against their American counterpart, winning back the return to the liquidity markets and the positive dynamics of oil and metals prices. Preliminary results from experts in South Africa suggested that omicron contamination was associated with predominantly mild symptoms. This thesis has yet to be tested and proven more thoroughly, but the markets reacted positively to the information. Nevertheless, several countries have introduced restrictions on movement that should objectively negatively affect the pace of recovery in demand for oil and oil products. So, from Tuesday, Japan will close the possibility of entry for foreigners, and its citizens arriving from countries where the omicron was detected will be quarantined. Cases of infection with the new strain have been confirmed or are suspected in South Africa, the Netherlands, the United Kingdom, Italy, Denmark, Germany, Austria, Belgium, the Czech Republic, and Australia, Hong Kong, Canada, and Israel. The Omicron strain is likely to spread worldwide, posing "very high" global risks, the World Health Organization (WHO) said Monday. In our opinion, this week, ahead of the publication of data on the US labor market for November, the dollar will continue to be in demand against high-yielding and commodity currencies but will be under pressure against other defensive currencies such as the franc and the yen. 21 out of 24 Emerging Markets currencies fell against the dollar over the week. The ruble, along with the Turkish lira, Mexican peso, and South African rand, entered the TOP-4 outsiders of the EM segment. The critical factor of pressure on the ruble was preparing Russian troops for a large-scale invasion of Ukraine and a landslide drop in oil prices as part of low-liquid Friday trade amid the decision of several countries to renew restrictions on air travel due to the omicron strain. On Monday morning, the South African rand and the ruble were among the top gainers among the EM currencies amid a recovery in commodity prices. US President Joe Biden told reporters that he could soon talk with Russian President Vladimir Putin and Ukrainian President Volodymyr Zelensky had some positive impact. Biden stressed that he was "concerned" about the situation around Ukraine. However, news about a possible dialogue is positively perceived by the market since, most often, such conversations lead to a decrease in geopolitical tensions.

• CHART OF THE DAY:

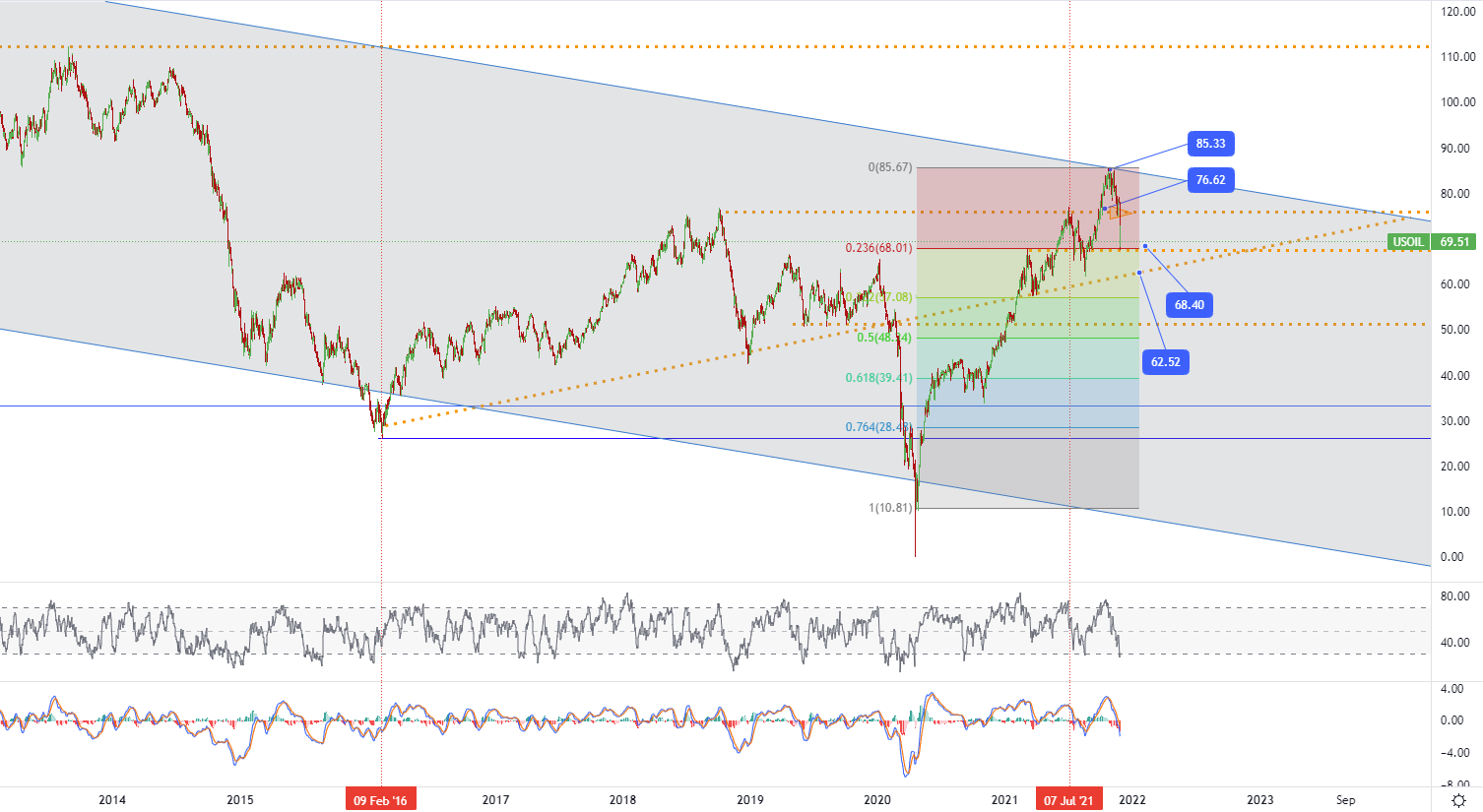

The oil market experienced panic selling under information about a new strain of coronavirus in South Africa. The cost of futures for Brent crude fell 11.5% to $ 72.72 per barrel, and WTI grades - by 9.1% to $ 71.25 per barrel. The sharp price dynamics triggered the triggering of stop orders and intensified the negative dynamics. Closing short positions after a sharp drop today led to a positive price correction. The pressure on prices was exerted by news about the reactions of different states intending to tighten control over the spread of the new strain worldwide. The concern is the resistance of the new theme to existing vaccines, which threatens to disrupt the ongoing vaccination. First of all, countries began to stop flights to the source of occurrence. The UK has suspended flights from South Africa and neighboring African countries, and the EU reported similar precautions. The spread of measures of total control of population movement is not yet planned. Still, the current wave of morbidity in the countries of the Northern Hemisphere is conducive to tightening measures. These decisions will, of course, harm the consumption of oil and petroleum products in December. It is also likely that in Q1 2022 when demand usually decreases under the influence of seasonal factors, the dynamics of the decline will be more pronounced. All of this was superimposed on the recent decision of the United States and other countries to free some of the oil from strategic reserves to lower oil prices. The participants in the OPEC + agreement, which is to decide on a further increase in production on December 2, have already announced that the surplus of oil on the market in 2022 could grow by 1.1 million barrels per day. If a decrease in demand superimposes the increase in supply from strategic reserves due to the imposed restrictions, then the surplus maybe even more significant. As a result, the market expects that OPEC + will not expand the oil supply by another 400 thousand barrels per day. However, the parties to the agreement have not yet expressed a desire to restrain the constant rate of increase in production, urging not to take into account the speculative movements of the market. From a technical point of view, the oil market is correcting downward in a growing trend. If the level of $ 70-65 per barrel holds, then prices may continue to rise. • WTI Crude oil - D1, Resistance around ~ 85.33 & 76.62, Support (target zone) around ~ 68.40 & 62.52

• WTI Crude oil - D1, Resistance around ~ 85.33 & 76.62, Support (target zone) around ~ 68.40 & 62.52

Start trading in four simple steps

1. Register

Open your live trading account

2. Verify

Upload your documents to verify your account

3. Fund

Deposit funds directly into your account

4. Trade

Start trading and choose from 130+ instruments

Demo account

The Blue Suisse Trading Account with virtual funds in a risk-free environment

Demo accountLive account

The Blue Suisse Trading Account in our transparent live model environment

Open an Account- Trading Account types Trading conditions Trading hours Transparency Market Information

- Products Currencies Commodities Indices Stocks

- Tools MetaTrader 4 / 5 Mobile CRM, MAM and DSP

- Education Currency Trading for Beginners How to improve your trading CFD Trading

- Partnerships Asset- and Moneymanager Tied agent White labels FIX API

- Company About us Regulatory Our philosophy Careers FAQs Contact us