Stocks close mixed, but near session highs - crude futures settle unchanged

• GLOBAL CAPITAL MARKETS OVERVIEW:

European stocks closed higher on Wednesday, ending the previous four-day losing streak. Telecom Italia led the gains, but concerns about the worsening epidemic in Europe and the prospect of implementing epidemic lockdown measures limited the increase. The pan-European STOXX 600 index climbed 0.1% and set its worst one-day performance in nearly two months on Tuesday, as the European mainland countered the epidemic and the market was worried about rising interest rates. Telecom Italia soared 15.6%, boosting telecom stocks to rise 1.2%. Earlier, there were reports that KKR was considering increasing the offer price after the largest investor, Vivendi, said the initial offer was too low. European stock markets are likely to fall weekly this week, as restrictions have been introduced again, and interest rate hikes and inflation concerns have triggered people's concerns about weak economic growth prospects. Travel stocks fell more than 1.0%, the seventh consecutive day of decline. Nick Nelson, Head of European Equity Strategy at UBS, said: “People are waiting to see what impact the restrictions will have on economic growth in the fourth quarter and next year. If the situation worsens, we see governments respond more aggressively. People will be worried about the overall economic growth in Europe." An earlier survey revealed that German business confidence deteriorated for the fifth consecutive month in November. Bottlenecks in manufacturing supply and a surge in new crown cases cast a shadow over Germany's growth prospects. The German DAX index fell 0.4%. The easing of concerns about Chinese demand pushed up copper prices, boosting miner stocks to rise 0.2%, and energy stocks rose 0.7% after crude oil prices rose slightly. The French CAC-40 index fell slightly by 0.03%, while the British FTSE index closed up by 0.27%. At the beginning of the trading session on Wednesday, November 24, the US stock market declined moderately and finished almost flat - continuing the trend of Monday-Tuesday. US Treasury yields resumed their growth along the entire curve, and yields on 2-, 5- and 10-year Treasuries renewed recent highs. Additional pressure on the market is exerted by the worsening financial statements of American companies. The prominent outsiders were technology companies (-0.71%), manufacturers of consumer goods (-0.70%), and manufacturers of materials (-0.59%). 31% of S&P 500 components rose in price, and 68% fell in price. At the beginning of the trading session on Wednesday, November 24, the US stock market declined moderately, continuing the trend of Monday-Tuesday. US Treasury yields resumed their growth along the entire curve, and yields on 2-, 5- and 10-year Treasuries renewed recent highs. Additional pressure on the market is exerted by the worsening financial statements of American companies. The S&P 500 components showed fragile dynamics: only 1 of the 11 main sectors of the index - energy (+ 1.11%) - was growing. The prominent outsiders were technology companies (-0.71%), manufacturers of consumer goods (-0.70%), and manufacturers of materials (-0.59%) 31% of S&P 500 components rose in price, and 68% fell in price. Tomorrow, the US stock market will be closed due to the Thanksgiving Day celebrations in the country, and today at 22:00 Moscow time, the minutes of the last Fed meeting (November 3) will be published, at which the regulator decided to start cutting the asset purchase program. The recent rhetoric of the FRS representatives indicates that at the next meeting on December 14-15, the regulator may consider the issue of increasing the rate of curtailment of the QE program. Investors will look in the text of the November 3 meeting minutes for indications of the criteria for such an adjustment. US GDP growth in the third quarter was revised from 2.0% q / q to 2.1% q / q. However, the consensus forecast of economists assumed the figure at the level of 2.2% q / q. Personal consumption grew only 1.7% QoQ in this period, but recent good data, including retail sales for October, suggests that economic growth is likely to pick up in the fourth quarter. However, logistical problems, supply chain disruptions, and declining consumer confidence could correct such prospects. The number of initial applications for unemployment benefits in the United States fell in the week to November 20 to 199,000, which, according to Bloomberg, is the lowest value since 1969. The consensus forecast for this figure was 260,000, but the sharp decline may be due to seasonal adjustments. If this is indeed the case, then next week, this figure may increase significantly. Durable goods orders fell 0.5% in October against expectations for a 0.2% rise, driven by a drop in commercial aircraft orders. At the same time, demands for industrial equipment, excluding the defense sector, increased by 0.6% in October against the consensus forecast of + 0.5%, and the September figures were revised from + 0.8% to + 1.1%. The upward trend in industrial equipment spending dates back to last May and has seen a decline in only one month since then. The ruble index attempted to return above 4000 points in the morning with the support of oil prices (Brent), which at that moment we're testing the strength of the level of $ 83 / bbl. However, oil prices did not manage to overcome this resistance, well, and the Moscow Exchange index - to gain a foothold above 4000 p. The weakening ruble against the dollar adds points to the basket of inflationary fears, which the Bank of Russia intends to fight rather actively. The money market does not already imply a 150 bp increase in the critical rate. Such expectations indicate a decrease in the attractiveness of investments in stocks over more conservative strategies. Therefore, the rise in expectations of a more aggressive monetary policy tightening cycle hurts the Russian stock market. The external background also did not stimulate growth. Liquidity on external markets remains low. Markets in the US will be closed on Thursday for Thanksgiving. The continuing geopolitical tensions should be added, and we get a cocktail of factors that prevented Russian stocks from demonstrating positive dynamics on Wednesday. 6 sectoral indices rose, and four declined. The IT sector fell 1.54% and became the outsider of the day (-4.85% in November). The Sectoral Index of Chemistry and Petrochemistry rose by 2.44% and became the growth leader (+ 5% in November). Of the 43 shares of the Moscow Exchange index, 14 rose in price, and 29 lost in value. Accordingly, for each index paper that increased in price, at least two fell in price. Japan's Nikkei Index closed down on Wednesday, and growth stocks were hit. Investors worried that the Federal Reserve Board (Fed/) might speed up policy tightening to deal with inflation risks. US President Biden nominated Fed Chairman Powell for re-election on Monday and appointed Fed Governor Brainard as vice-chairman. This makes investors expect the Fed to be more aggressive. In addition, U.S. technology stocks fell in the past two trading days, weakening investors' risk appetite in the Japanese stock market. The Japanese market was closed for a holiday on Tuesday. The Nikkei index closed down 1.58% to 29,302.66 points; the top stock index fell 1.16% to 2,019.12 points. Internet company Z Holdings fell 4.6%, and Softbank Group fell 3.3%. Semiconductor-related stocks were also hit hard, with Lasertec down 3.3% and Advantest down 4.1%. On the other hand, some value stocks rose, a weaker yen boosted automakers, and rising U.S. bond yields boosted banks. Mitsubishi Motors rose 5.1%; Nissan Motor rose 4.4%. Toyota Motor rose 0.9%. Among financial stocks, Sumitomo Mitsui Financial Group (SMFG) rose 2.1%, while Mitsubishi UFJ Financial Group rose 0.8%.Hong Kong stocks ended their 5-day decline, but their gains were limited. The Hang Seng Index repeatedly rose, up 200 points in the afternoon, hitting 24851 points, closing at 24685 points, up 33 points, or 0.14%, and the principal board turnover was about 137.4 billion yuan. The technology index fell 0.5%, and heavyweight technology stocks developed individually. Meituan, which announced its quarterly results on Friday, rose 3%, making it the best performing blue-chip stock. After Xiaomi's performance, it plummeted by nearly 7%, while Alibaba and Tencent fell by almost 1% and almost 2%, respectively. Kuaishou continued to build well and rose by more than 5%. Alibaba Health fell 7%, making it the worst-performing blue-chip stock. In addition, the heavyweight HSBC and AIA rose more than 1% and nearly 3%, respectively.

• REVIEWING ECONOMIC DATA:

Looking at the last economic data:

- US: Wall Street Bank is preparing for rising inflation. They conduct internal health checks to monitor whether customers in risky industries can repay loans, develop hedging strategies, and recommend caution when trading. The U.S. Consumer Price Index (CPI) released this month recorded the most significant year-on-year increase in 31 years, driven by soaring gasoline and other commodities prices. However, central bank officials believe that soaring prices are only a temporary phenomenon caused by the interruption of the supply chain, and bank executives are not buying it too much and are beginning to strengthen risk management. Rising inflation is generally seen as beneficial to banks, increasing their net interest income and profitability. But top bankers warned that if inflation rises too fast, it may have adverse effects. A senior banker of a European bank with many operations in the United States said that continued high inflation would bring credit and market risks to the bank. The bank is assessing this risk in an internal stress test. Another banker said that the risk team is also monitoring credit exposure in industries most affected by inflation. This includes companies in consumer discretionary, industrial, and manufacturing industries.

- US: US soybean futures fell for the second consecutive day on Wednesday, under pressure Profits were settled, and the fund took out positions before Thanksgiving. CME Group said the market would be closed on Thursday due to the holiday, and Friday’s trading hours will be shortened. CBOT-January soybean futures closed down 6-1/2 cents, with a settlement price of 12.66-1 per bushel 2 USD. CBOT-January soybean oil futures rose 0.62 cents to 60.70 cents per pound. January Soybean Meal Futures closed down 5.20 US dollars, at 350.90 US dollars per short ton. Corn futures ended lower. Traders said they were affected by the stronger U.S. dollar and gains before the Thanksgiving holiday Profit closing and exiting positions. The settlement price of the December corn contract fell by 3/4 cent to $5.79-3/4 per bushel. The March contract fell 2-3/4 cents to $5.85-1/2 per bushel.

- US: New home sales in the United States rose 0.4% month-on-month in October, and the growth rate was significantly slower than that in September. The annual rate was 745,000, which was lower than the expected 800,000. As of the end of October, there were 389,000 houses for sale, slightly higher than the 378,000 at the end of September. In addition, the growth rate of new home sales in September was revised downward to 7.1%, the previous value increased by 14%. As a result, the annual rate is 742,000 rooms, lower than the initial value of 800,000 rooms.

- US: The number of new jobless claims in the United States dropped to less than 200,000 people last week, with 199,000, a 52-year low, a sharp drop of 71,000 weekly, which was much more than market expectations. The number of new jobless claims is lower than the average level of about 220,000 before the epidemic, and the data has fallen since October. The four-week average of the new applicants last week failed to approximately 252,000, a decrease of 21,000 from a week-to-week period. As of November 11, the number of people who continued to apply for unemployment benefits this week was 2.049 million, which was a decrease of 60,000 on a weekly basis, but the number of continuous claims still exceeded expectations.

- US: The final value of the University of Michigan Consumer Confidence Index in November was 67.4, higher than market expectations of 66.9 and higher than the initial value of 66.8, but lower than the final value of 71.7 in October. The final value of the current conditions index and the expected index in November, lower than the last value in October, was reported at 73.6 and 63.5, respectively.

- US: The growth rate of personal income and expenditure in the United States in October exceeded market expectations. Personal income rose 0.5% month-on-month last month, higher than the expected 0.2% increase and better than the 1% drop in September. Personal spending rose 1.1% month-on-month, higher than the 1% expected and higher than the 0.6% in September. During the period, the personal consumption expenditure (PCE) price index rose 0.6% month-on-month, and the core PCE price index also rose 0.4%, in line with expectations. The personal PCE price index rose 5% on a year-on-year comparison, and the core index rose 4.1%, in line with expectations.

- CN: Kaisa Group, a Chinese real estate developer who has recently suffered a deep debt crisis, announced on Wednesday evening that several member companies of the group and their associated companies issued wealth management products with a principal amount of approximately RMB 1.493 billion in October. And when it expires in November, it has implemented repayment measures for wealth management products with a principal amount of around 1.097 billion yuan. The shares of the applied company will resume trading at 9 am on November 25. It was published in the Hong Kong Stock Exchange's announcement here and stated that these measures include the redemption of 10% of the principal amount and interest from the 20th day of the month when the appropriate principal amount is due and the saving of 10% of the principal amount every three months from the maturity date. And interest and the outstanding principal amount will be paid deferred interest to the holder at an interest rate of 4.35%. The issuer is negotiating repayment measures with the holder for the remaining principal amount of approximately 397 million yuan. The announcement also stated that the company is considering measures (including issuing an exchange offer) on outstanding US dollar bills with a principal amount of US$400 million due on December 7. Kaisa Group released its wealth management product redemption plan on Monday evening, stating that it will redeem the principal and interest in installments according to the time sequence of Jinheng Wealth’s product maturity; for the principal due to investors, 10% of the maturity month will be redeemed. , And 10% will be paid every three months after that.

- CN: The Mainland China Banking and Insurance Regulatory Commission stated that the current economic and financial environment faced by the banking industry is complex and severe, and some long-term accumulated contradictions and problems have been concentratedly exposed. According to the authorities, some banks have failed to implement significant decisions and deployments, falsely reported data on inclusive financial indicators, illegally flowed funds into the real estate sector, illegally added hidden debts to local governments, and implemented fee reduction and profit-sharing measures inadequately. In addition, the China Banking and Insurance Regulatory Commission said that some banks have failed to enforce national macro policies, have repeatedly investigated and repeatedly committed problems in the field of credit management, and have modified their regulatory arbitrage methods. In particular, the recent occurrence of risk events such as the deposit certificate pledged note business and personal information security had damaged the overall reputation of the banking industry and exposed problems such as insufficient assessment of potential business risks. The China Banking and Insurance Regulatory Commission also mentioned that efforts should be made to explore financial services that promote technological innovation, to increase support for advanced manufacturing and independent controllable industrial chains and supply chains, to innovate green financial products and services around the realization of the dual-carbon goal, and to improve Multi-financial resources are allocated to critical areas and weak links of rural revitalization.

- NZ: As expected by the market, the Bank of New Zealand raised interest rates by 25 basis points to 0.75%, in line with market expectations, raising interest rates for the second consecutive month. The central bank said it continues to reduce stimulus measures. The minutes of the main bank meeting show that the committee expects that the official overnight lending rate will need to be gradually increased, which will be 0.94% in March next year and 2.14% in December.

• LOOKING AHEAD:

Today, investors will receive:

- EUR: German Final GDP q/q, German GfK Consumer Climate, ECB Monetary Policy Meeting Accounts, ECB President Lagarde Speaks, and Belgian NBB Business Climate.

- USD: Bank Holiday.

- GBP: MPC Member Haskel Speaks and BOE Gov Bailey Speaks.

- JPY: SPPI y/y.

- AUD: Private Capital Expenditure q/q.

• KEY EQUITY & BOND MARKET DRIVERS:

- Raspadskaya may pay interim dividends for the III quarter in the amount of 28 rubles per share. The closing date of the register for receiving dividends is January 18, 2022. The company's dividend for the first half of 2021 amounted to 23 rubles per share and was paid under the new dividend policy, which implies sending at least 100% of FCF to shareholders with low leverage. At the same time, as Raspadskaya previously reported, concentrate sales prices increased in Q3 in ruble terms by 51% versus the previous quarter. This factor was the main reason for the sharp increase in the company's cash flow in July-September and generous dividend payments.

- TCS Group earned a record profit for the third quarter and nine months of 2021. The Group confirmed its forecasts for the leading indicators for 2021: net profit is expected to be at least 60 billion rubles, net loan portfolio growth is over 50%. TCS Group receipts looked worse than the market. Investors' disappointment may be because the company does not plan to pay dividends in the first quarter of 2022, as capital requirements were increased when the Bank of Russia ranked TCS Group as a systemically important credit institution. Tinkoff Bank plans to launch full-fledged mortgage lending in the first half of 2022, but for now, it will start with refinancing mortgages from other banks, said the bank's financial director Ilya Pisemsky during a conf call. However, at the end of last year, CEO Oliver Hughes said,

- LUKOIL published on Wednesday, November 24, the condensed interim consolidated financial statements (IFRS) for the III quarter and nine months of 2021. Overall, we view the report as positive. Record free cash flow (free cash flow increased by 44% YoY to RUB 228 bln - the maximum in 5 years in rubles, but in dollars, it was higher in Q3 2019) increases the base for dividend payments at the end of 2021. do not expect that the contribution of the IV quarter. The dividend will be as high as the contribution of the III quarter. Due to the likely significant increase in CAPEX. However, the yield on dividend payments for the second half of the year may well exceed 7%.

- The Federal Reserve Board (FRB) announced on the 24th that the Federal Open Market Committee (FOMC) agenda on November 2-3 would reduce the pace of bond-buying programs if high inflation continues. However, it turns out that several policymakers were willing to accelerate and raise rates more quickly.

- European Central Bank (ECB) Board member Makruh Irish Central Bank Governor, said yesterday that the ECB's rate hike is not justified but should be dealt with without delay if circumstances change. So stated. "As far as the current evidence is concerned, the factors that are causing inflation are temporary, so the rate hike is not justified," the Parliamentary Commission said. "But my view is that if the evidence changes, we should respond without delay. If the evidence changes, my view may change," he said. He mentioned the structural effects and structural changes in economic management methods.

- The European Central Bank (ECB) Managing Director Schnabel said on the 24th that there is no risk of the euro area falling into stagflation, a combination of high inflation and stagnant economic growth. "I don't think it's a stagflation situation, and I don't think I'm approaching a stagflation situation," he said. "Inflation is relatively high, but there is no economic stagnation. On the contrary, most economies are growing very strongly, well above potential growth," he said.

- Southern European bond yields have risen to the highest level in weeks in the euro area financial and bond markets. European Central Bank (ECB) in response to a rate hike by Reserve Bank (Central Bank) There are vital observations that major central banks, including the central bank, will take similar steps to curb inflation. Wait. Central Bank of New Zealand announced on the 24th that the official cash rate of the policy interest rate Increased rate (OCR) by 25 basis points (bp), 0.7. It was set to 5%. While deregulation of the new coronavirus supports economic activities, Inflationary pressures have led to a monetary deduction following the previous October meeting. Italy's 10-year bond yield rose 4bp to 1.08%. At one point, there was a scene where the high level of 1.1% was reached for the first time in three weeks. The 10-year German-Italy bond yield gap is 129bp, the highest since the 2nd of this month. Greek 10-year bond yields had been at their highest level since June last year. Cyprus's 10-year bond yield is about one year. It rose to 0.66%, the first level. German 10-year bond yield remains almost unchanged at minus 0.222%. Analysts said November's Eurozone Comprehensive Purchasing Managers Index (PM)

- The shares of the retailer Nordstrom fell 27%: the company's quarterly report indicates an increase in labor and fulfillment costs, as well as the fact that sales are stubbornly staying below pre-crisis levels.

- Shares of another retailer, Gap, lost 23%: the company's quarterly earnings report was worse than expected. In addition, the retailer lowered its annual earnings and revenue guidance, citing supply chain disruptions and entry inflation. Following this, JPMorgan downgraded securities, and Wells Fargo downgraded their target.

- Autodesk shares were down 16% after the company released a mixed quarterly report, prompting many analysts to cut their targets for the stock.

• STOCK MARKET SECTORS:

- High: Energy, Real Estate.

- Low: Consumer Staples, Utilities, Materials.

• TOP CURRENCY & COMMODITIES MARKET DRIVERS:

- COMMODITIES: Crude oil inventories rose 1.0 million barrels to 434 million barrels as of November 19, a report from the Energy Information Administration (EIA) showed. A decline of 0.5 million barrels was preliminary expected, and the American Petroleum Institute (API) reported an increase in stocks for the week by 2.3 million barrels. Gasoline inventories fell 0.6 million barrels from the previous week to 211.4 million barrels. Distillate stocks fell 2.0 million barrels to 121.7 million barrels. The drop in petroleum product inventories confirms the demand that has recovered from the pandemic with lagging refining and a shortage of raw materials. Stocks in strategic reserves fell 1.6 million barrels to 604.5 million barrels. From the beginning of this year to November 19, 33.6 million barrels of oil were sold from strategic reserves, while 32 million barrels were sold until November 12, i.e., before the announcement by US President Biden of the release of oil from reserves. As we wrote earlier, within the framework of the approved program for 2021, another 18 million barrels can be produced from strategic reserves. Inventories at Cushing's storage facilities rose to 27.4 million barrels in response to the sale of oil from reserves. The spread between Brent and WTI crude as of November 23 widened to $ 3.81 per barrel due to increased pressure on the market from the supply side. Nevertheless, the dynamics of oil reserves show that the availability of crude oil in the US domestic market is decreasing. The stocks curve in November reached the lower boundary of the average long-term corridor. As of November 19, domestic oil production in the United States increased by 100 thousand barrels per day, amounting to 11.5 million barrels per day. US oil imports as of November 19 rose to 6.436 million barrels (+ 4.0% by November 12, 2021). US oil exports fell to 2.605 million barrels (-28.2% by November 12, 2021). After publication data on reserves, the price of a future for Brent crude rose to $ 82.48 per barrel and a future for WTI crude - to $ 78.53 per barrel.

- CURRENCY: The dollar index on Wednesday once again renewed its 16-month high. The US currency strengthened against all G10 currencies in the evening, and only the Canadian dollar remained stable against its southern neighbor. The demand for the dollar was driven by a short technical factor - Thanksgiving and a longer technical factor - the end of the calendar year. Usually, the demand for the dollar grows at the end of the year, but to hedge the risks, market participants buy a monthly contract in the second half of November. So in December itself, we may not even see such technical demand. But now it is showing up. San Francisco Fed chief Mary Daly said he sees the case for accelerating the pace of the Fed's stimulus cut and is open to doing so if inflation remains high and employment growth remains strong. She predicts that the Fed will want to raise rates for the first time at the end of next year but won't be surprised if the regulator raises the rate twice in 2022. The federal funds rate futures market has already considered the possibility of a rate hike in June 2022 with 100% probability. The likelihood of such a move jumped to 64% in May. Such expectations continue to support the dollar, which may strengthen against the euro to 1.1000 in the medium term. The overwhelming majority of emerging market currencies weakened against the dollar on Wednesday, but the weakest was the Mexican peso (-0.93%) and the Russian ruble (-0.9%). At the same time, short OFZs remained under pressure, while cautious purchases of bonds that had fallen in price due to geopolitical risks began in the middle and far parts of the curve. EUR / USD - 1,119 (-0.50%), GBP / USD - 1.3325 (-0.37%), USD / JPY - 115.46 (+ 0.30%), Dollar Index - 96.888 (+ 0.41%), USD / RUB - 75.002 (+ 0.99%), EUR / RUB - 83.9053 (+ 0.45%).,

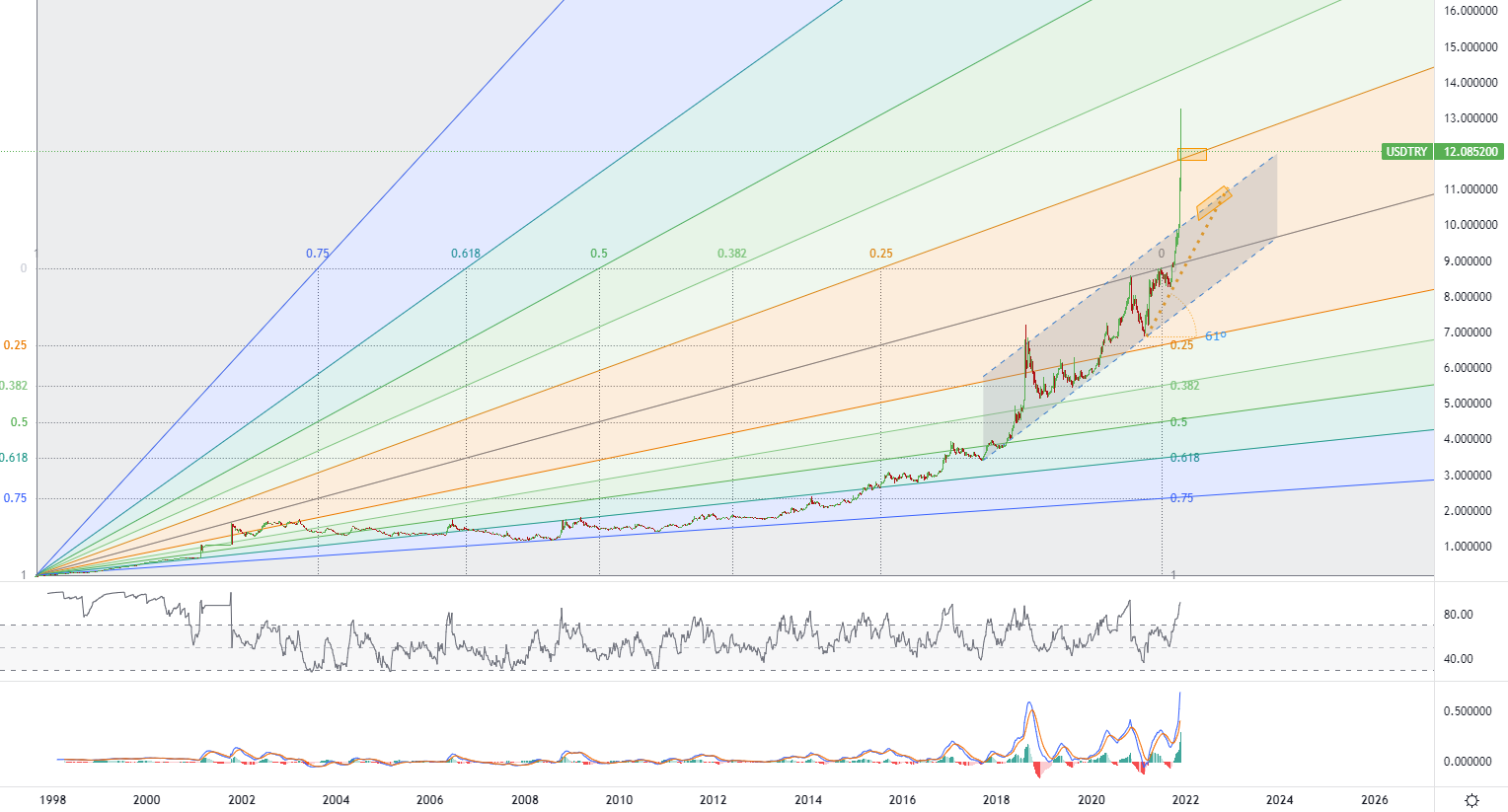

• CHART OF THE DAY:

The Turkish lira plummeted by more than 15% on Tuesday after President Erdogan defended the recent sharp interest rate cut and vowed to win his "independence economic war" despite widespread criticism and demands from his Reverse policy. The TRYTOM=D3 exchange rate of the lira against the US dollar fell to 11.45 at one time, setting a record low continuously since 11 trading days, and then reduced some of the declines, closing 10.2% lower at 12.7015. The lira has fallen 42% this year, including a drop of more than 22% since the beginning of last week. Erdogan put pressure on the central bank to shift to a positive easing cycle, which he said was to promote exports, investment, and employment-even. If the inflation rate soars to nearly 20%, the depreciation of the lira accelerates and severely erodes the incomes of the Turks. Many analysts called the rate cuts reckless, while opposition politicians called for immediate elections. After Erdogan and Central Bank President Sahap Kavcioglu met, the central bank issued a statement saying that the sharp depreciation of the lira was “unrealistic and completely out of the fundamentals” of the economy. The central bank did not imply that it would intervene to prevent the lira from collapsing, saying it would only do so under certain conditions of "excessive volatility." Semih Tumen, former vice president of the Turkish Central Bank, called for an immediate restoration of the policy of protecting the lira's value. He was fired in Erdogan’s latest round of rapid leadership adjustments last month. The lira fell on Tuesday the most since the peak of the currency crisis in 2018. The problem in 2018 led to a sharp recession in the Turkish economy, with economic growth below average for three consecutive years and double-digit inflation. The Central Bank of Turkey has cut interest rates by a total of 400 basis points since September. When almost all other central banks are beginning or preparing to tighten their policies in response to rising inflation, real yields have fallen into a negative value. Turkey is scheduled to hold elections no later than the mid-term of 2023. At this time, Erdogan's Justice and Development Party (AK Party) has fallen in support, reflecting the sharp rise in the cost of living. As volatility indicators soar to new highs since March, investors seem to be fleeing. Erdogan removed the hawkish central bank president from his position in March and planted an official who shared the same ideas and criticized high-interest rates. As the Turks bought hard assets, the lira against the euro EURTRY = Tuesday fell to a record low of 14.4225. The 10-year benchmark bond yield rose to more than 21% for the first time since 2018. Tradeweb data shows that sovereign dollar bonds have plummeted, with prices of many longer-term bonds falling by more than $0.02 as the lira plunged, Turkey’s main stock index.XU100 suddenly became cheaper due to its valuation. It rose 1.7%, setting a new high, but banking stocks fell. • Turkish lira USDTRY - W, Resistance around ~ 12.21 & 14.31 Support (target zone) around ~ 11.00

• Turkish lira USDTRY - W, Resistance around ~ 12.21 & 14.31 Support (target zone) around ~ 11.00

Start trading in four simple steps

1. Register

Open your live trading account

2. Verify

Upload your documents to verify your account

3. Fund

Deposit funds directly into your account

4. Trade

Start trading and choose from 130+ instruments

Demo account

The Blue Suisse Trading Account with virtual funds in a risk-free environment

Demo accountLive account

The Blue Suisse Trading Account in our transparent live model environment

Open an Account- Trading Account types Trading conditions Trading hours Transparency Market Information

- Products Currencies Commodities Indices Stocks

- Tools MetaTrader 4 / 5 Mobile CRM, MAM and DSP

- Education Currency Trading for Beginners How to improve your trading CFD Trading

- Partnerships Asset- and Moneymanager Tied agent White labels FIX API

- Company About us Regulatory Our philosophy Careers FAQs Contact us